US Banking Regulators Unveil Framework for Payment Stablecoins

A critical hurdle has been overcome in US stablecoin regulation: Draft rules of implementation under the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) have been released by the two main banking regulators. The FDIC and OCC have opened for public comment Notices of Proposed Rulemaking (NPRMs) outlining the application, licensing, and supervision processes for banks to issue payment stablecoins.

What Happened?

1. FDIC Draft

The Federal Deposit Insurance Corporation (FDIC) Board of Directors approved a draft rule implementing the application provisions of the GENIUS Act.

The rule allows insured deposit institutions to issue payment stablecoins through an affiliate.

State banks and savings associations under FDIC supervision must apply to the FDIC to have their affiliates approved as “authorized payment stablecoin issuers” in order to conduct this activity.

The draft regulates that applications will be evaluated according to legal factors under Section 5 of the law, finalized within specific timeframes, and an appeals mechanism will be established for rejected applications. The review period is 60 days following its publication in the Federal Register.

2. OCC Draft

The Office of the Currency Conduct Authority (OCC) has proposed a comprehensive regulatory framework for national banks, federal savings associations, and federal branches.

The draft, announced in OCC Bulletin 2026-3, covers “authorized payment stablecoin issuers” (PPSI – approved affiliates of banks), federally qualified issuers, state-qualified issuers, and foreign payment stablecoin issuers (FPSI) under OCC jurisdiction.

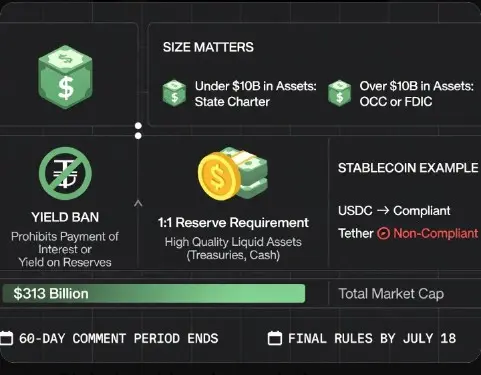

The rule aims to establish a licensing, supervision, and enforcement framework. The OCC is soliciting public comment on over 200 questions concerning permitted activities, reserve assets, the licensing process, and capital. The comment period is again 60 days.

Scope of the Drafts

Who is affected: National banks and their subsidiaries, federal savings associations, federal branches, and state banks under FDIC supervision. Also, foreign and state-qualified issuers within the OCC's jurisdiction.

What is regulated: Application and approval process, evaluation criteria, timelines, right to appeal. On the OCC side: Licensing, supervision, reserve asset structure, and capital requirements.

What is excluded: Anti-money laundering (AML) and sanctions compliance obligations are not covered in these drafts; separate regulations are expected for these topics.

What's Next?

Both drafts will enter a 60-day public comment period after being published in the Federal Register. Regulators will evaluate the comments received and shape the final rules. Once the process is complete, a clear legal procedure will be established in the US for the first time for the issuance of payment stablecoins through bank subsidiaries.

This step puts the GENIUS Act's claim to "drive innovation" into action: it opens a predictable application path for banks while regulators link reserve quality, consumer protection, and financial stability to the supervisory framework.

#GENIUSImplementationRulesDraftReleased

A critical hurdle has been overcome in US stablecoin regulation: Draft rules of implementation under the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) have been released by the two main banking regulators. The FDIC and OCC have opened for public comment Notices of Proposed Rulemaking (NPRMs) outlining the application, licensing, and supervision processes for banks to issue payment stablecoins.

What Happened?

1. FDIC Draft

The Federal Deposit Insurance Corporation (FDIC) Board of Directors approved a draft rule implementing the application provisions of the GENIUS Act.

The rule allows insured deposit institutions to issue payment stablecoins through an affiliate.

State banks and savings associations under FDIC supervision must apply to the FDIC to have their affiliates approved as “authorized payment stablecoin issuers” in order to conduct this activity.

The draft regulates that applications will be evaluated according to legal factors under Section 5 of the law, finalized within specific timeframes, and an appeals mechanism will be established for rejected applications. The review period is 60 days following its publication in the Federal Register.

2. OCC Draft

The Office of the Currency Conduct Authority (OCC) has proposed a comprehensive regulatory framework for national banks, federal savings associations, and federal branches.

The draft, announced in OCC Bulletin 2026-3, covers “authorized payment stablecoin issuers” (PPSI – approved affiliates of banks), federally qualified issuers, state-qualified issuers, and foreign payment stablecoin issuers (FPSI) under OCC jurisdiction.

The rule aims to establish a licensing, supervision, and enforcement framework. The OCC is soliciting public comment on over 200 questions concerning permitted activities, reserve assets, the licensing process, and capital. The comment period is again 60 days.

Scope of the Drafts

Who is affected: National banks and their subsidiaries, federal savings associations, federal branches, and state banks under FDIC supervision. Also, foreign and state-qualified issuers within the OCC's jurisdiction.

What is regulated: Application and approval process, evaluation criteria, timelines, right to appeal. On the OCC side: Licensing, supervision, reserve asset structure, and capital requirements.

What is excluded: Anti-money laundering (AML) and sanctions compliance obligations are not covered in these drafts; separate regulations are expected for these topics.

What's Next?

Both drafts will enter a 60-day public comment period after being published in the Federal Register. Regulators will evaluate the comments received and shape the final rules. Once the process is complete, a clear legal procedure will be established in the US for the first time for the issuance of payment stablecoins through bank subsidiaries.

This step puts the GENIUS Act's claim to "drive innovation" into action: it opens a predictable application path for banks while regulators link reserve quality, consumer protection, and financial stability to the supervisory framework.

#GENIUSImplementationRulesDraftReleased