Primitive Ventures: The "East-West Divide" in Prediction Markets — Why Are We Betting on Opinion Labs?

Author: Yetta, Partner at Primitive Ventures, Wildon, Researcher at Primitive Ventures

Weekly trading volume: $1.5 billion, with a total trading volume surpassing $10 billion within 60 days. While everyone is applauding Polymarket’s $13 billion valuation and its high-profile partnership with the NYSE, this platform from the East, still in its “seed stage,” quietly achieved a bottom-up breakthrough. This is our full investment assessment of Opinion Labs.

The Era of Standalone NPCs Is Coming to an End

For decades, we’ve been living in a “single-player game.” Truth is produced by a few institutions, narratives are finalized in conference rooms, and most of us are just NPCs following a predetermined storyline. Web2 gave us a voice but didn’t truly involve us in decision-making. How beliefs are formed and consensus is shaped remains locked inside algorithmic black boxes and power structures.

But what if beliefs could flow freely and be priced?

- Opinions are not just expressions of attitude but bets

- Disagreements are not just emotional conflicts but price bifurcations

- Consensus is not just retweets but a curve that can reverse at any time

- Reality is no longer a scripted show to be watched but a multiplayer game of strategy

The Paradox of the “Less Long-Tail” Market

Is prediction market more a financial market or a content market? It’s an interesting debate. As a financial market, it performs very well in certain scenarios. Without liquidity, there are no prices; without prices, there are no signals. Mechanisms like order books, market makers, and depth work smoothly during globally attention-grabbing events like US elections, but tend to fail outside these scenarios.

Human attention itself is fragmented. Most things we care about depend heavily on specific contexts and regional backgrounds, such as cultural gossip, local politics, celebrity scandals, and social topics. The internet has not converged these interests but instead caused them to branch infinitely. Content is exploding, but capital and liquidity remain scarce.

Thus, a paradox emerges:

- Markets need concentration to be effective

- Human opinions are inherently dispersed

If a platform can only rely on a few headline events to maintain liquidity, it’s more like an “event exchange” than a true belief market. So the question becomes: when information refuses to converge, how do you build a financial system on top of it?

Why We Invest in Opinion Labs

A year ago, we invested in @opinionlabsxyz. At that time, Polymarket had just completed its first large-scale validation during an election cycle, and prediction markets had become one of the strongest narrative threads in Western VC circles. We believed that this content/event-driven approach wouldn’t be absent in the East, so we invested in Opinion Labs. Six months later, discussions around prediction markets spread to Asia, reaching BNB Chain. At that moment, the only product with a mature offering, capable of launching immediately and capturing momentum, was Opinion.

More importantly, they achieved this scale with almost minimal capital expenditure. In terms of product pace, execution density, and per capita output, they are among the most efficient teams we’ve seen.

East ≠ West: Prediction Markets Are Diverging

Prediction markets are clearly diverging between East and West, and the reason is simple. Assets can converge globally, but opinions cannot. USD, gold, and US stocks can have unified prices, but what people are willing to bet on is a cultural product. The expansion of prediction markets fundamentally depends on liquidity and shared attention.

In the US, this shared attention is highly concentrated. Decades of sports betting have cultivated retail habits, and politics has evolved into a nationwide reality show. Attention naturally converges on a few major events. Kalshi and Polymarket have logically focused on top markets, serving high-frequency and professional traders with deeper order books.

In East Asia, the situation is entirely different. China’s political discussion space is limited, Japanese retail investors are generally less politically engaged, and Korean users’ attention is more focused on speculation, entertainment, social issues, and pop culture. In different markets, what retail investors truly care about and have enough understanding to form judgments on varies greatly.

This difference is vividly reflected in data. In the 2026 Korean presidential election, Polymarket’s trading volume was about $40,000, while Opinion Labs reached $52 million. Prediction markets cannot be monopolized by winners because belief formation is highly localized.

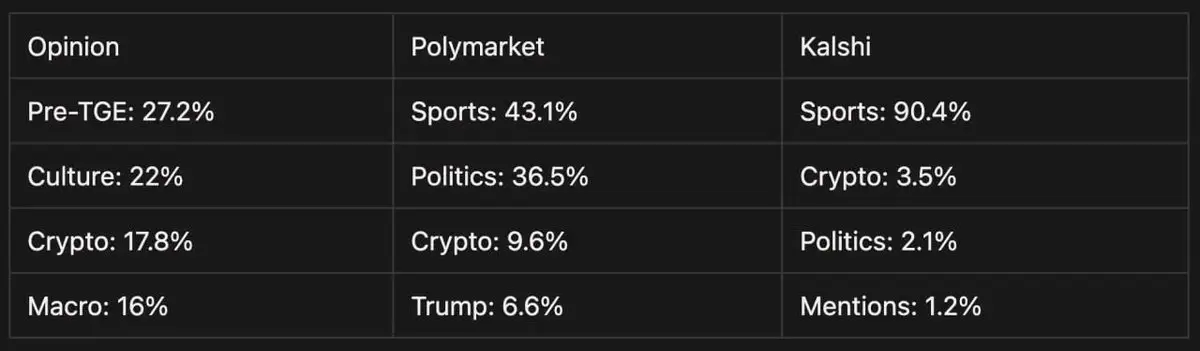

When shared attention is absent, liquidity does not automatically concentrate but disperses naturally. The structure we observe confirms this: compared to Polymarket and Kalshi, Opinion’s trading distribution is noticeably more dispersed. Trading volume has not collapsed into a few top events but continues to spread across numerous offshore markets that truly matter to users in the long tail.

AI as the Key to Scaling

Markets created by humans alone can no longer keep up with this era. When opinions are infinite and contexts highly localized, relying on manual curation and manual launches forces prediction markets to converge on only a few headline events.

This is precisely why AI becomes indispensable.

At Opinion Labs, AI transforms scattered claims into structured markets: automatically generating clear settlement rules, defining failure boundaries, and using staking mechanisms to constrain behavior and reinforce accountability. Market creation no longer depends on a small team’s judgment but can scale massively. A large number of culturally and regionally specific local markets can be rapidly generated without being overwhelmed by spam content.

As markets extend into the long tail, the real challenge is settlement. Long-tail markets often depend on complex, dispersed, unstructured information sources. A single decision mechanism cannot handle this complexity. AI can process and cross-verify information at scale, while hardware-level security and human governance serve as the final safety net.

This means prediction markets can finally expand horizontally for the first time. Instead of compressing global attention into a few super-events, in a highly dispersed world, beliefs can be organized, traded, and verified.

Prediction Market 2.0: One Paradigm, Two Evolutions

In prediction markets, a clear divergence between East and West is emerging.

The West has chosen financialization and institutionalization. We see IB founders saying the highest-frequency trading involves weather/temperature contracts. More broadly, industries like energy, agriculture, and shipping, which are exposed to climate risks, lack sufficiently detailed and tradable hedging tools. In this context, the development of prediction markets is about whether liquidity can be scaled, whether strong derivative structures can be created, and whether institutions can understand and accept them as part of risk management infrastructure. Entrepreneurs are thinking about how to refine prediction markets into robust financial infrastructure.

The East is moving toward internetization and contentification. It resembles an entertainment-oriented information consumption and expression mechanism. The core is when users are willing to bet and why. It’s a form of content monetization: betting provides participation, odds reflect narrative strength, and trading volume indicates emotional consensus. The product’s goal is not complex financial engineering but a content operation logic—how to turn hot topics, public opinion, social discussions into sustained trading motivation.

Prediction Market has entered 2.0. It is no longer a single market where winners take all but two distinct evolutionary paths shaped by culture. Both point toward a larger shift: markets are no longer just places for trading outcomes but mechanisms for organizing and processing uncertainty at the atomic level.

Related Articles

February Pullback Ends Six-Month Growth Streak for Prediction Markets

Iran's crackdown on Gulf countries' pressure on the United States is counterproductive; multiple countries may retaliate against Iran

Kalshi: Supports trading price fluctuations of Rolex, Omega, and other watch brands

Anonymous Trader Bets $25,676 on Iran Closing Strait of Hormuz by March 31

Federal Ruling Raises Risk for Polymarket, Kalshi in Nevada