Unsecured stablecoin lending

Introduction

Users in the global unsecured consumer credit market are like the fat sheep of modern finance—slow to act, lacking judgment, and lacking mathematical ability.

When unsecured consumer credit shifts to the stablecoin track, its operating mechanism will change, and new participants will also have the opportunity to share in the profits.

The market is huge

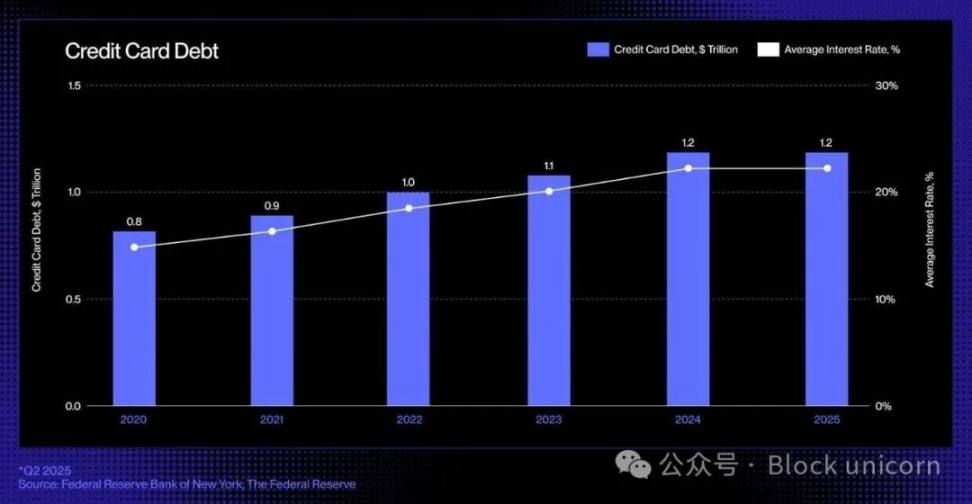

In the United States, the primary form of unsecured lending is credit cards: this ubiquitous, highly liquid, and instantly available credit tool allows consumers to borrow money without providing collateral while shopping. Outstanding credit card debt continues to grow, currently reaching approximately $1.21 trillion.

Outdated Technology

The last significant change in the credit card loan sector occurred in the 1990s when Capital One introduced a risk-based pricing model, a groundbreaking initiative that reshaped the landscape of consumer credit. Since then, despite the emergence of new banks and fintech companies, the structure of the credit card industry has remained largely unchanged.

However, the emergence of stablecoins and on-chain credit protocols has brought a new foundation to the industry: programmable money, transparent markets, and real-time funding. They are expected to eventually break this cycle and redefine the way credit is created, financed, and repaid in a digital, borderless economic environment.

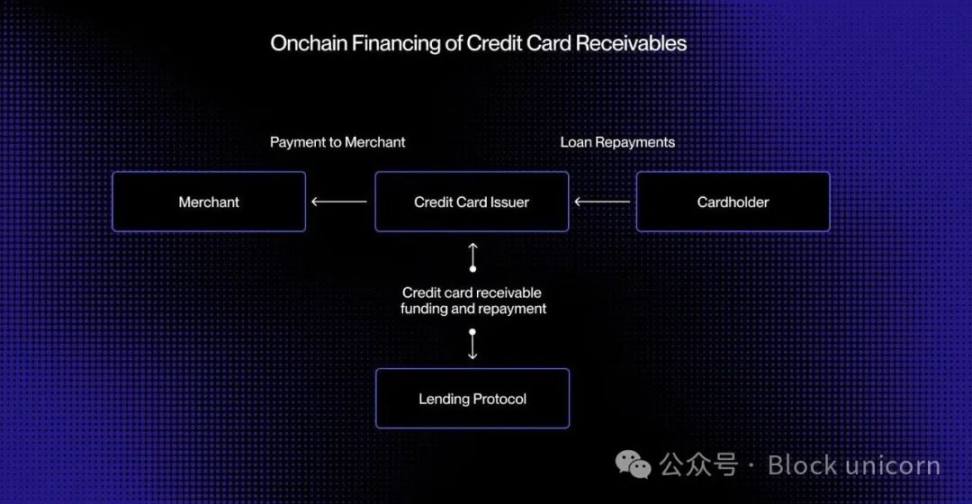

In today's bank card payment systems, there is a time lag between authorization (transaction approval) and settlement (the card issuer transferring funds to the merchant through the card network). By moving the fund processing process on-chain, these receivables can be tokenized and financed in real-time.

Imagine a consumer purchasing a product worth $5,000. The transaction is immediately authorized. Before settling with Visa or Mastercard, the issuing institution tokenizes the receivables on the blockchain and receives $5,000 worth of USDC from the decentralized credit pool. Once the settlement is completed, the issuing institution sends these funds to the merchant.

Afterwards, when the borrower makes a repayment, the repayment amount will be automatically returned to the on-chain lender through a smart contract. Similarly, the entire process occurs in real-time.

This method enables real-time liquidity, transparent funding sources, and automatic repayments, thereby reducing counterparty risk and eliminating many of the manual processes still present in today's consumer credit.

From Securitization to Fund Pool

For decades, the consumer credit market has relied on deposits and securitization to achieve large-scale lending. Banks and credit card issuers bundle thousands of receivables into asset-backed securities (ABS) and then sell them to institutional investors. This structure provides ample liquidity, but also introduces complexity and opacity.

“Buy Now, Pay Later” (BNPL) loan institutions like Affirm and Afterpay have demonstrated the evolution of credit approval processes. They no longer provide a universal credit limit, but instead evaluate each transaction at the point of sale, differentiating between a $10,000 sofa and a $200 pair of sneakers.

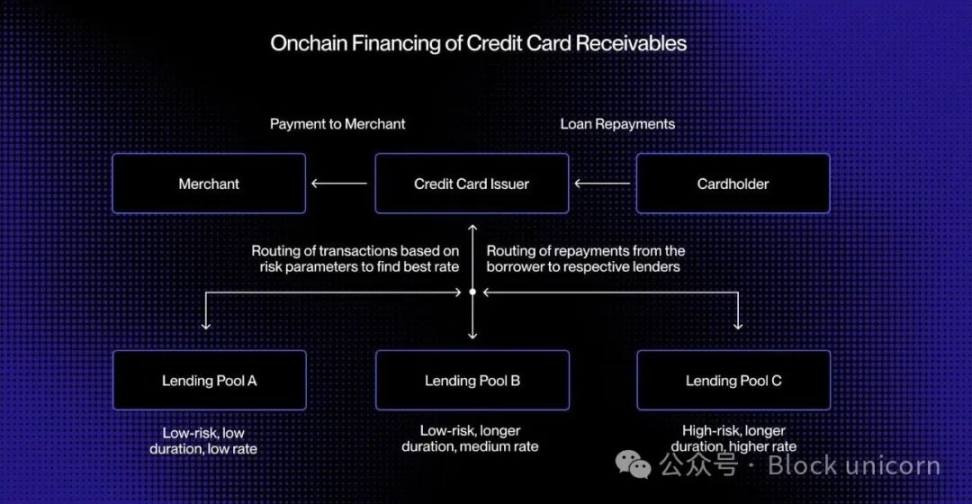

This transaction-level risk control produces standardized and divisible receivables, each with a clear borrower, term, and risk profile, making it an ideal choice for real-time matching through on-chain lending pools.

On-chain lending can further expand this concept by creating dedicated credit pools tailored to specific borrower demographics or purchase categories. For example, one credit pool could fund small transactions for high-quality borrowers, while another credit pool could specifically provide travel installment plans for sub-prime consumers.

Over time, these liquidity pools may evolve into targeted credit markets, achieving dynamic pricing and providing transparent performance metrics for all participants.

This programmability leads to more efficient capital allocation, providing consumers with better interest rates and opening the door to an open, transparent, and instantly auditable global unsecured consumer credit market.

Emerging On-Chain Credit Stack

Reimagining unsecured loans for the on-chain era is not merely about transplanting credit products onto the blockchain, but fundamentally rebuilding the entire credit infrastructure. In addition to issuing institutions and processing entities, the traditional loan ecosystem also relies on a complex network of intermediary institutions:

We need a new way to assess credit scores. Traditional credit scoring systems, such as FICO and VantageScore, may be transplantable to the blockchain, but decentralized identity and reputation systems could play a much larger role.

Lending institutions will also require credit assessments, which are equivalent to ratings from S&P, Moody's, or Fitch, to evaluate underwriting quality and repayment performance.

Finally, the less prominent but crucial aspects of loan collection also need improvement. Debt denominated in stablecoins still requires enforcement mechanisms and recovery processes, combining on-chain automation with off-chain legal frameworks.

Stablecoin cards have bridged the gap between fiat currency and on-chain consumption. Lending protocols and tokenized money market funds have redefined savings and yields. By introducing unsecured credit on-chain, this triangular relationship has been refined, enabling consumers to borrow seamlessly and allowing investors to fund credit in a transparent manner, all driven by open financial infrastructure.

Related Articles

Circle Stock Surges 60% After Earnings as USDC Growth and GENIUS Act Boost Investor Confidence

A newly created wallet deposits $1,135,000 USDC to open a 3x leveraged NVDA long position, with a position value of $2.6 million.

Circle stock soars 60%! The surge in USDC volume and favorable regulations for stablecoins continue to drive CRCL's strength

U.S. 303-page Housing Bill Hidden CBDC Ban, White House Endorses

Huang Licheng deposited 250,000 USDC into HyperLiquid again 7 hours ago and increased his ETH long position.