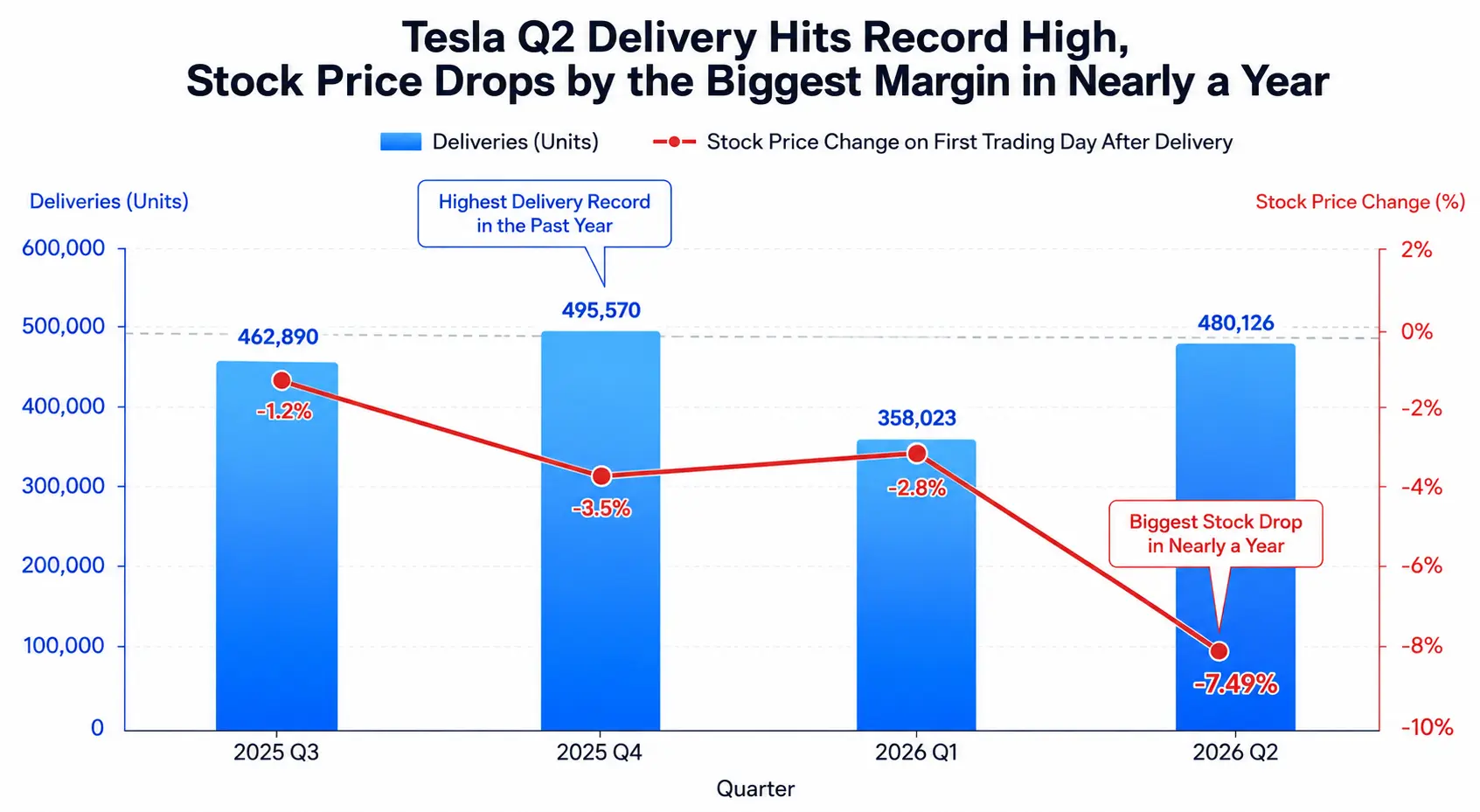

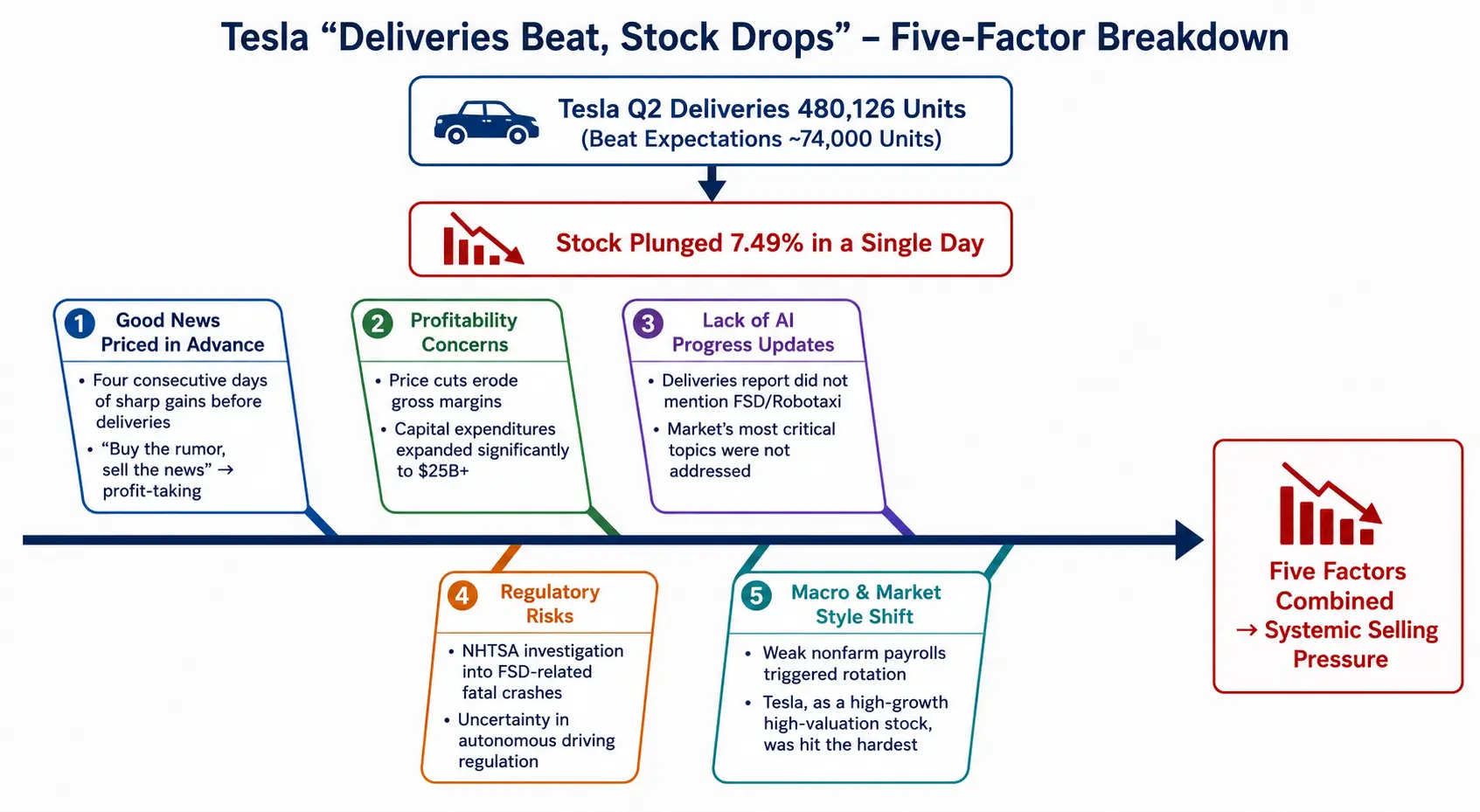

On July 2, 2026, Eastern Time, Tesla released its second-quarter delivery data that excited the market — global deliveries reached 480,126 vehicles, up 25% year-over-year and 34% quarter-over-quarter, marking the company's strongest second-quarter performance in history. This figure far exceeded Wall Street analysts' consensus expectation of about 406,000 vehicles, surpassing it by over 74,000 vehicles. However, during U.S. stock trading on July 2, Tesla's stock price closed sharply down 7.49% at $393.45, posting its biggest single-day drop in nearly a year. This marks the third consecutive time Tesla's stock has fallen after releasing quarterly delivery data.

At the same time, the U.S. Bureau of Labor Statistics released the June nonfarm payrolls report, which showed only 57,000 new jobs added in the month, far below the market expectation of 115,000. The unexpectedly cooling job market drove the Dow Jones Industrial Average up 1.14% to 52,900.07, a record high, but the Nasdaq Composite fell 0.8% to 25,832.67, dragged down by chip stocks. Tesla, as a key component of the Nasdaq, saw its 7.49% single-day decline become a major factor dragging the tech sector.

Deliveries set a record, yet the stock plummeted — behind this anomaly lies a systemic selling pressure formed by multiple factors. From the early digestion of positive news, profitability concerns, lack of AI progress, regulatory risks, and macro style rotation, we deconstruct the complete logic chain behind Tesla's stock price divergence from its fundamentals.

Tesla Q2 Deliveries Hit Record High, Stock Posts Biggest Drop in Nearly a Year

"Buy the Rumor, Sell the Fact": Delivery Positives Already Priced In

Before Tesla's Q2 delivery data was released, the market had already fully priced in this "better-than-expected report card." Data shows that in the four trading days before the delivery report, Tesla's stock price rose continuously, with a single-day gain of about 8% on Monday alone. By the close on July 2, the stock had risen to $425.30. This meant that when the delivery figure of 480,126 finally landed, the market had little room left to continue buying.

This classic "buy the rumor, sell the fact" pattern has occurred before with Tesla. Gene Munster of Deepwater Asset Management described the delivery performance as a "monster beat," but noted that the stock decline reflected profit-taking after the four-day rally. Gary Black, managing partner of Future Fund, also observed that although Tesla "crushed" Q2 delivery expectations, many investors had already priced in this positive news in advance.

The trend of "stock falling upon delivery" for three consecutive quarters indicates that the market's reaction mechanism to delivery data has shifted from "data-driven" to "expectation-gap-driven" — only when actual deliveries significantly exceed the already raised market expectations can the stock receive positive feedback. The current state of "beating expectations but already priced in" instead becomes a catalyst for profit-taking.

More critically, the magnitude of the delivery "beat" itself has structural limitations. While the absolute figure of 480,126 is impressive, the model mix is highly concentrated — Model 3 and Model Y together delivered 467,762 vehicles, accounting for about 97% of total deliveries. Model S and Model X were discontinued in May. In other words, this round of delivery growth came mainly from lower-priced models rather than a full product line expansion. Without new models to drive growth, the marginal contribution of sales volume to valuation is diminishing.

Profitability Concerns: Double Squeeze from Price War and Gross Margin

Tesla's second-quarter delivery growth was, to a significant extent, the result of "trading volume for price." To boost sales, Tesla continued to launch lower-priced versions of the Model 3 and Model Y. Coupled with the formal expiration of the U.S. federal electric vehicle tax credit at the end of September 2025, Tesla's automotive gross margin faces continuous downward pressure.

Analysts point out that investors worry Tesla is relying on price cuts and inventory clearance to drive sales, and with the exit of the U.S. federal EV tax credit, the company's automotive gross margin may see a significant decline. In fact, Tesla has experienced an annual decline in vehicle sales over the past two years, pressured from multiple directions: consumer backlash over Musk's political statements, changes in U.S. federal EV tax credit policy, and intensified competition from Chinese, Korean, and European automakers.

In the market share battle, Tesla's competitive landscape remains intensifying. By pure EV sales, Tesla's Q2 figure of 480,126 still trailed BYD's 557,090, failing to reclaim the global pure EV sales crown.

Meanwhile, Tesla's planned capital expenditure this year has expanded significantly, mainly directed toward Optimus humanoid robots, autonomous Cybercab, and AI infrastructure. Massive capital expenditure means that even with revenue growth, free cash flow will remain under pressure. China Merchants Securities recently lowered its earnings forecasts for Tesla for 2026 and 2027 by 20% and 39%, respectively, to reflect downside risks in the automotive business, surging R&D spending, and substantial increases in capital expenditure.

Lack of AI Progress: The Market's Most Concerned Issue Unaddressed

Perhaps the most noteworthy aspect of Tesla's Q2 delivery report is not the delivery figure itself, but what was omitted from the report.

William Stein, managing director of Truist Securities, explicitly stated after the delivery data release that the importance of AI development to Tesla's long-term cash flow and stock performance far exceeds that of vehicle deliveries. He further noted that in the short term, the market is most focused on the progress of FSD and related projects (Robotaxi and Cybercab), yet Tesla provided no updates on these key issues in the delivery report. The brokerage reiterated its "Hold" rating on Tesla and raised its target price from $400 to $430.

Andrew Percoco of Morgan Stanley, while calling the 480,126 figure a "clear upside surprise" and "the highest automotive business growth rate since Q3 2023," still maintained a "Neutral" rating and $415 target price. William Blair stated that the strong automotive performance shows Tesla's core auto business "still exists," but noted that energy storage deployments of 13.5 GWh fell short of its own expectation of 20.6 GWh.

Tesla's market cap of about $1.6 trillion is largely dependent on the realization of long-term businesses such as AI, autonomous driving, and humanoid robots. Even if the traditional EV business delivers record numbers, it merely serves as a "ticket" to support this grand narrative, not the core driver of valuation itself. When the market's most concerned AI topics are absent from the delivery report, it is unsurprising that investors vote with their feet.

Regulatory Risk: FSD Safety Investigation Persists

Beyond the lack of AI progress, regulatory uncertainty also pressures Tesla's stock.

The National Highway Traffic Safety Administration (NHTSA) is still investigating a fatal accident that occurred in Texas on June 19, 2026, involving the Full Self-Driving (FSD) system. This safety investigation keeps regulatory risks for autonomous driving technology in the market spotlight. Just nine days ago, Tesla's stock fell 4.8% due to a similar investigation into driver-assistance software.

Tesla's valuation has shifted from traditional car sales to autonomous driving and robotaxi narratives. Any regulatory uncertainty regarding the software can directly impact market confidence. Currently, Tesla's stock is at $393.45, about 20.3% below its 52-week high. The direction of the regulatory investigation will largely determine the speed of market confidence recovery in Tesla's autonomous driving narrative.

Macro Style Rotation: Headwinds for High-Valuation Growth Stocks

Placing Tesla's stock performance in a broader market context makes the logic clearer.

On July 2, after the release of U.S. June nonfarm payroll data, market expectations for a Fed rate hike further cooled. However, the Nasdaq failed to rally in tandem — chip stocks continued to fall, with the Philadelphia Semiconductor Index plunging 5.44%. Clear divergence emerged within the tech sector: Apple surged nearly 5%, while Tesla dropped over 7% and Meta fell nearly 5%.

This divergence precisely reflects the core contradiction in the current U.S. stock market: weak employment data, while easing rate hike fears, also heightens concerns about an economic slowdown. In such an environment, capital tends to rotate out of high-valuation, high-expectation growth stocks into more defensive and dividend-supported value sectors. Tesla, as a representative high-valuation growth stock — whose valuation heavily relies on AI and autonomous driving businesses not yet commercialized at scale — bears the brunt of this style rotation.

After the nonfarm data release, the dollar index dropped sharply, and global capital reallocation is accelerating, with Tesla right at the epicenter of this rotation.

Future Outlook: Key Variables and Time Window

Looking ahead, Tesla's stock price trajectory will depend on the evolution of several key variables.

First, Q2 earnings on July 22. Tesla will report its full second-quarter financial results after the U.S. market closes on July 22, 2026. The market consensus expects Q2 adjusted EPS of $0.45. At that time, data on gross margin, free cash flow, and AI capital expenditure details will provide more critical valuation bases than delivery numbers. More importantly, management's comments on FSD, Robotaxi, and Optimus progress during the earnings call will be core inputs for market repricing.

Second, the commercialization pace of FSD and Robotaxi. Tesla launched limited commercial Robotaxi services in Austin, Texas in June 2026, and the company said it will continue to expand operations in 2026. Deployment of the FSD system in European markets is also progressing. However, the speed, scale, and regulatory approval pace of these developments remain highly uncertain.

Third, the battle of institutional ratings and target prices. Currently, the average target price for Tesla from 51 Wall Street analysts is $404.55, with an average rating of "Hold." Divergence among institutions is significant: Baird gives a $522 target price and an "Outperform" rating, Haitong International raised its target price to $533.2, while Goldman Sachs gives only a $395 target price and a "Neutral" rating, expecting full-year 2026 deliveries of 1.865 million vehicles.

Fourth, the persistence of macro liquidity and style rotation. If employment data continues to weaken without triggering a recession, the relative advantage of value sectors may continue, putting sustained pressure on high-valuation growth stocks like Tesla. Conversely, if new breakthrough progress occurs in the AI field or the Fed signals clear easing, the style rotation could reverse.

Five Factors Behind Tesla's "Stock Falls on Delivery"

FAQ

Q1: What exactly was Tesla's Q2 delivery volume? How much did it exceed market expectations?

Tesla's global deliveries in the second quarter of 2026 were 480,126 vehicles, up 25% year-over-year and 34% quarter-over-quarter. Wall Street analysts' consensus expectation was approximately 406,000 vehicles, with actual deliveries exceeding by about 74,000 vehicles, or about 18%. This is Tesla's strongest second-quarter performance ever.

Q2: Why did Tesla's stock plummet 7.49% despite beating delivery expectations?

There are five main reasons: First, the stock had been rising for four consecutive days before the delivery data release, with positives already priced in, triggering profit-taking. Second, market concerns that the price war continues to erode gross margins. Third, the delivery report provided no updates on FSD, Robotaxi, or other AI topics, which are currently the market's main focus. Fourth, NHTSA is still investigating a fatal accident involving FSD, creating regulatory pressure. Fifth, weak nonfarm data led to a style rotation in U.S. stocks, pressuring high-valuation growth stocks.

Q3: How did Tesla's energy storage business perform this quarter?

Tesla deployed 13.5 GWh of energy storage products in the second quarter. Some institutions consider this below expectations — William Blair's own expectation was 20.6 GWh. However, some analysts believe that with AI data centers driving global electricity demand growth, the long-term demand for large-scale energy storage systems like Megapack still has growth potential.

Q4: What are the core challenges Tesla currently faces?

There are four main aspects: At the product level, Tesla is in a vacuum period without new models. At the profitability level, the price war continues to squeeze gross margins. At the strategic level, the commercialization progress of AI and autonomous driving businesses remains uncertain. At the competitive level, Chinese automakers like BYD continue to capture market share, and Tesla still trails BYD in the pure EV segment.

Q5: What are the key drivers for Tesla's stock price in the future?

Market attention has shifted from quarterly delivery volumes to four directions: gross margin and free cash flow data in the Q2 earnings report on July 22; progress of FSD deployment in European markets; the expansion pace of Robotaxi commercial services in Austin, Texas; and the production progress of Optimus humanoid robots. These factors will determine whether the market can maintain confidence in Tesla's AI narrative.