STABLECOINS CROSS A NEW THRESHOLD IN THE GLOBAL PAYMENT SYSTEM

As structural transformation accelerates in the digital asset market, stablecoins are marking a critical turning point in financial architecture, surpassing the transaction volume of the Automated Clearing House (ACH), a key payment infrastructure of the US banking system, for the first time. According to February data, stablecoin transfer volume reached approximately $7.2 trillion, while the ACH system remained at $6.8 trillion during the same period.

This development reflects a lasting change in the nature of capital movements rather than short-term market excitement. Stablecoins are no longer merely a tool of the crypto market, but are becoming an increasingly used component of the global payment and consensus layer.

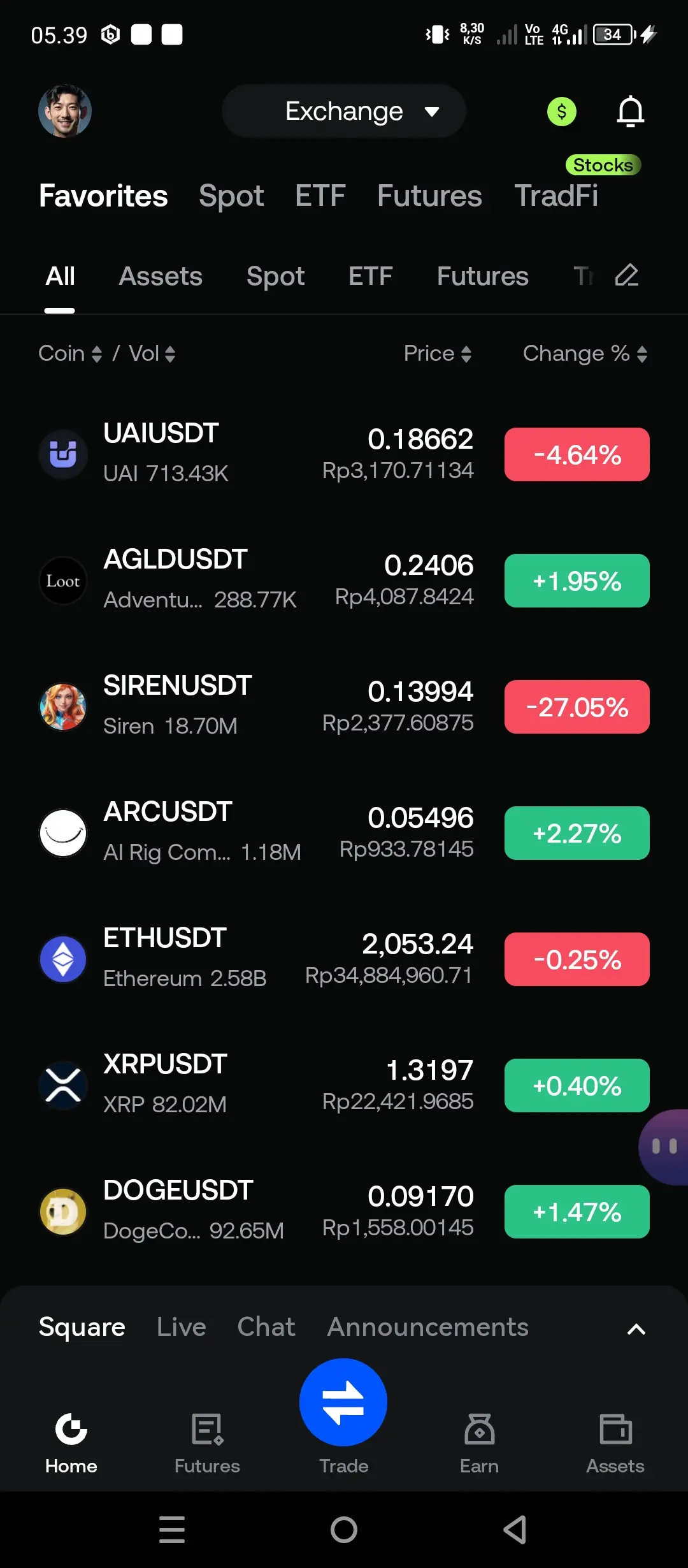

Assets like Tether and USD Coin, central to the stablecoin ecosystem, are preferred, particularly in cross-border payments and institutional transactions, due to their high liquidity, low volatility, and dollar-based value pegging. Unlike traditional banking systems with transaction hours, weekend restrictions, and geographical limitations, stablecoins offer 24/7 uninterrupted and near-instantaneous transfer capabilities. It offers

On the corporate side, the main driving force of growth is not individual speculation, but rather B2B payments, supply chain finance, and international trade flows. Companies are turning to stablecoin-based solutions to achieve operational efficiency, reduce costs, and shorten settlement times. This situation, especially in emerging markets, facilitates access to dollar liquidity and increases financial inclusion.

Significant developments are also taking place in the US and global regulatory framework. Reserve transparency, audit standards, and licensing processes are becoming clearer for stablecoin issuers, while integration between traditional financial institutions and blockchain-based infrastructures is accelerating. This process supports the positioning of stablecoins as regulated financial instruments, moving away from being a systemic risk factor.

From a macro perspective, the fact that stablecoin volumes are surpassing established systems like ACH shows that the financial infrastructure is evolving towards decentralization. In this transformation, speed, accessibility, and programmability stand out as decisive factors. Stablecoins are not only a means of payment but are also becoming the cornerstone of a new generation of financial infrastructure that can work integrated with smart contracts.

In this context, while Bitcoin is increasingly strengthening its role as a digital reserve asset, stablecoins are becoming a key element of liquidity. One is positioned as the main layer enabling circulation, while the other stands out as a store of value, representing the infrastructure that makes the daily functioning of the financial system possible.

In conclusion, stablecoins surpassing ACH volume stands out as a concrete indicator of a paradigm shift in the financial world. Capital is now moving towards systems that are faster, more flexible, and can move across borders. If this trend continues, it is considered highly probable that stablecoins will become one of the central components of the global payment infrastructure in the coming years.

#StablecoinDebateHeatsUp

#TetherEyes$500BFundraising

#GateSquareAprilPostingChallenge

#CreatorLeaderboard

#GENIUSImplementationRulesDraftReleased

As structural transformation accelerates in the digital asset market, stablecoins are marking a critical turning point in financial architecture, surpassing the transaction volume of the Automated Clearing House (ACH), a key payment infrastructure of the US banking system, for the first time. According to February data, stablecoin transfer volume reached approximately $7.2 trillion, while the ACH system remained at $6.8 trillion during the same period.

This development reflects a lasting change in the nature of capital movements rather than short-term market excitement. Stablecoins are no longer merely a tool of the crypto market, but are becoming an increasingly used component of the global payment and consensus layer.

Assets like Tether and USD Coin, central to the stablecoin ecosystem, are preferred, particularly in cross-border payments and institutional transactions, due to their high liquidity, low volatility, and dollar-based value pegging. Unlike traditional banking systems with transaction hours, weekend restrictions, and geographical limitations, stablecoins offer 24/7 uninterrupted and near-instantaneous transfer capabilities. It offers

On the corporate side, the main driving force of growth is not individual speculation, but rather B2B payments, supply chain finance, and international trade flows. Companies are turning to stablecoin-based solutions to achieve operational efficiency, reduce costs, and shorten settlement times. This situation, especially in emerging markets, facilitates access to dollar liquidity and increases financial inclusion.

Significant developments are also taking place in the US and global regulatory framework. Reserve transparency, audit standards, and licensing processes are becoming clearer for stablecoin issuers, while integration between traditional financial institutions and blockchain-based infrastructures is accelerating. This process supports the positioning of stablecoins as regulated financial instruments, moving away from being a systemic risk factor.

From a macro perspective, the fact that stablecoin volumes are surpassing established systems like ACH shows that the financial infrastructure is evolving towards decentralization. In this transformation, speed, accessibility, and programmability stand out as decisive factors. Stablecoins are not only a means of payment but are also becoming the cornerstone of a new generation of financial infrastructure that can work integrated with smart contracts.

In this context, while Bitcoin is increasingly strengthening its role as a digital reserve asset, stablecoins are becoming a key element of liquidity. One is positioned as the main layer enabling circulation, while the other stands out as a store of value, representing the infrastructure that makes the daily functioning of the financial system possible.

In conclusion, stablecoins surpassing ACH volume stands out as a concrete indicator of a paradigm shift in the financial world. Capital is now moving towards systems that are faster, more flexible, and can move across borders. If this trend continues, it is considered highly probable that stablecoins will become one of the central components of the global payment infrastructure in the coming years.

#StablecoinDebateHeatsUp

#TetherEyes$500BFundraising

#GateSquareAprilPostingChallenge

#CreatorLeaderboard

#GENIUSImplementationRulesDraftReleased