On March 8, U.S. President Trump announced on Truth Social that he will refuse to sign any bills until the “Save America Act” (SAVE Act) is passed in the strongest possible form. This statement directly constrains the already stalled progress of the “Digital Asset Market Transparency Act” (CLARITY Act).

Trump’s Final Ultimatum on the SAVE Act: The Resource Competition Effect in Legislation

The SAVE Act requires voters to provide proof of citizenship when registering, which is a core issue in Trump’s push for election reform. The House of Representatives passed it strictly along party lines, but in the Senate, without bipartisan support, there is a clear gap to reach the 60-vote threshold needed to block procedural motions.

Trump’s hardline stance of “pass the SAVE Act first or I will veto everything” directly occupies legislative resources in the Senate. As noted by well-known X platform user Chad Steingraber: “The Senate must first handle the SAVE Act, then we can push forward the CLARITY Act. But we don’t have much time left.”

Dual Barriers Facing the CLARITY Act: The SAVE Act and Stablecoin Controversy Coexist

Even without external interference from the SAVE Act, the CLARITY Act faces two core obstacles:

First: Stablecoin Yield Provisions Trigger Strong Banking Industry Opposition

The core controversy of the CLARITY Act concerns whether crypto platforms can offer rewards similar to deposit interest to stablecoin holders. The opposition is led by financial institutions:

JPMorgan CEO Jamie Dimon: Argues that yield-bearing stablecoins will accelerate the outflow of commercial bank deposits, continuing pressure through banking policy research.

Bank of America CEO Brian Moynihan: Warns that such products could lead to a 30% to 35% loss of commercial bank deposits.

U.S. Treasury Analysis: Potential risk exposure approaches $6.6 trillion, making stablecoin yield provisions a highly sensitive issue for systemic financial stability.

Second: Ongoing Time Pressure

The CLARITY Act was passed in the House in July 2025 with a bipartisan vote of 294 to 134 and was immediately placed in the Senate Banking Committee. The scheduled review on January 15, 2026, was indefinitely postponed after major industry players like Coinbase withdrew support for stablecoin provisions; the White House’s March 1 deadline has passed without resolution.

Next Steps: Legislation, Negotiation, and Enforcement Alternatives

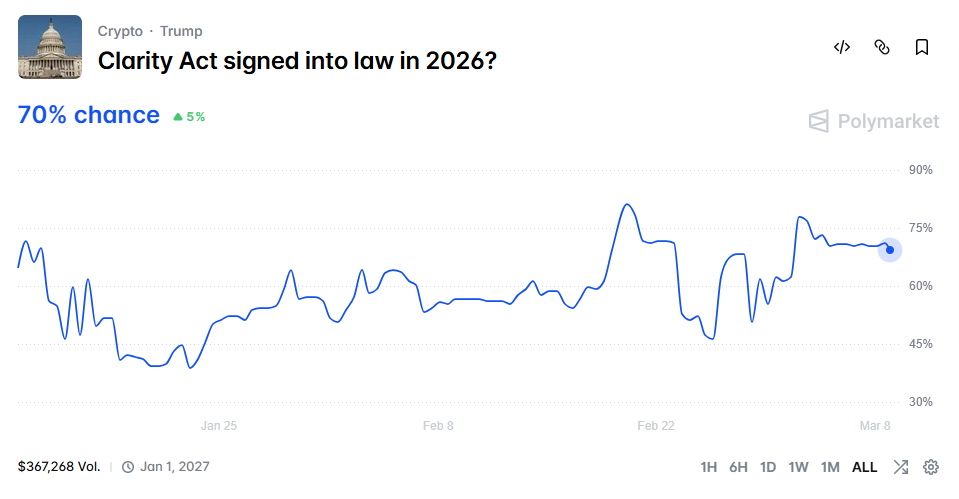

(Source: Polymarket)

(Source: Polymarket)

The Senate Banking Committee is expected to resume review in mid to late March, with negotiations possibly extending into April. If the fight over the SAVE Act continues, cryptocurrency regulation agenda may be delayed until after the 2026 midterm elections.

Polymarket predicts a 70% chance that the CLARITY Act will ultimately pass in 2026, indicating market optimism despite the short-term deadlock. JPMorgan analysts note that if the bill passes, it could serve as a significant positive catalyst for the crypto market and potentially be implemented in the second half of 2026.

If legislative progress stalls, the SEC and OCC may fill the regulatory vacuum through enforcement actions—OCC recently released a 376-page draft rule on reward provisions, showing regulators are preparing for enforcement pathways.

Frequently Asked Questions

How does the SAVE Act affect the progress of the CLARITY Act?

Trump’s declaration to veto all bills until the SAVE Act passes creates direct competition for the limited legislative resources in the Senate. Since the probability of the SAVE Act passing in the Senate is only 18%, a prolonged stalemate could further shrink the window for the CLARITY Act’s review, possibly delaying it until after the midterm elections.

What is the core issue of stablecoin controversy in the CLARITY Act?

The main dispute concerns whether crypto platforms can offer stablecoin holders interest-like rewards. The banking industry, including JPMorgan and Bank of America, believes this threatens deposit outflows. The U.S. Treasury estimates potential risk exposure near $6.6 trillion. This disagreement is the primary policy obstacle causing the CLARITY Act’s stagnation in the Senate.

If the CLARITY Act cannot be legislated soon, what challenges will the industry face?

The SEC and OCC may resort to enforcement actions to fill the regulatory gap, rather than legislative solutions. The OCC’s recent 376-page draft rule on reward provisions indicates a move toward enforcement-driven regulation, which could impact long-term institutional capital inflows due to the lack of clear legislative framework.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.