Korean stocks plummeted 20% in two days, the worst in Asian markets. Why?

South Korea’s KOSPI Index lost $270 billion in market value over the past 48 hours, far exceeding declines in Taiwan, Hong Kong, and Japan. The underlying factors are a concentrated vulnerability stemming from energy import dependence, semiconductor industry concentration, and foreign investment structure.

(Previous highlights: Market crash! Taiwan plunges 1,300 points, Korean stocks hit an 8% drop and circuit breaker for two days, Nikkei drops over 2,100 points, crude oil hits a one-year high)

(Additional background: Iran blocks the Hormuz Strait, “firing on more than ten oil tankers”! Trump warns: temporarily tolerating rising oil prices, joint efforts with Germany and Israel to counter)

Table of Contents

Toggle

- Iran’s grip on global oil prices

- How important is the Hormuz Strait?

- When half the market is dependent on two companies

- The fate of foreign investment and the won

- Why do foreign investors especially prefer to sell Korean stocks first?

- The persistent “Korea Discount”

- The destiny of high-leverage nations

$270 billion — this is the market value evaporated from the KOSPI index in just 48 hours, roughly equivalent to the total market capitalization of Vietnam’s stock market or four times Korea’s annual defense budget, all gone in two days.

March 3rd, Seoul’s KOSPI plunged 452 points, a 7.24% drop, closing at 5,791 points — the largest single-day decline since August 2024. That alone was devastating, but the next day was even worse…

March 4th opened with the index continuing its free fall, triggering a circuit breaker, halting all trading for 20 minutes, and closing down over 12%.

In total, the two-day decline approached 20%, marking the worst 48 hours in Seoul stock market history since the 2008 global financial crisis.

At the same time, other Asian markets also hemorrhaged. Taiwan’s stocks fell nearly 1,500 points, down 4.3%; Nikkei 225 dropped 3.6%; Hang Seng down 2.2%… but none of these declines approached half of Korea’s.

So why was Korea hit so hard this time? Here are some observations:

Iran’s Grip on Global Oil Prices

First, to understand the panic in global markets, we must look 6,500 kilometers away, to the Persian Gulf.

On February 28, the US and Israel launched a joint military strike against Iran, targeting missile facilities and nuclear capabilities, aiming to kill Supreme Leader Khamenei. The conflict escalated rapidly over the weekend, and Iran’s Islamic Revolutionary Guard Corps announced the closure of the Hormuz Strait — the vital artery for global oil transportation.

How important is the Hormuz Strait?

Approximately 14 million barrels of crude oil pass through this narrow waterway daily, accounting for 32% of global seaborne oil trade. Three-quarters of this oil flows to China, India, Japan, and Korea.

After Iran’s blockade announcement, about 150 ships were forced to anchor around the strait, unable to pass. International oil prices surged 14 days in a row, with Brent crude rising from $72 to $83 per barrel. JPMorgan warns that if shipping disruptions last three to four weeks, oil prices could soar above $100 per barrel.

For most countries, the potential rise in oil prices is a worrying variable. Especially for energy-import-dependent nations like Taiwan and Korea, the tension is even more acute.

Nomura Securities’ analysis indicates that among major Asian economies, Korea’s liquefied natural gas (LNG) reserves can only support about two to four weeks of normal demand. Oil reserves are slightly better, covering about seven months in total. But in geopolitical crises, seven months is a short window — markets never wait until supplies are exhausted before panicking.

When Half the Market Depends on Two Companies

Oil prices are the trigger, but Korea’s real vulnerability lies deeper: its market structure.

On March 3rd, Samsung Electronics closed down 9.88%, breaking the psychological 200,000 won barrier. SK Hynix plunged 11.50%. Hyundai Motor fell 11.72%, Kia dropped 11.29%, LG New Energy down 7.96%.

These numbers are alarming on their own, but more critical is their weight in the index. Just Samsung Electronics and SK Hynix together account for over 40% of KOSPI’s weighting.

In plain terms, nearly half of the KOSPI’s movement depends on these two semiconductor giants. When Samsung drops 10% and SK Hynix 11%, even if all other hundreds of listed companies stay flat, the index will be dragged down.

This extreme concentration is rare among major global stock markets. While the US S&P 500 also faces concentration issues with the “Big Seven” tech giants, the top two (Apple and Microsoft) together account for about 14%. In Japan’s Nikkei 225, the largest, Toyota, accounts for less than 5%.

Furthermore, Samsung Electronics and SK Hynix’s core businesses are highly overlapping: both produce memory chips. DRAM and NAND Flash define almost the entire Korean semiconductor industry. When the global AI boom boosts demand for high-bandwidth memory (HBM), these two companies’ stock prices soar, pushing KOSPI from around 4,300 points at the start of the year to over 6,200 — nearly a 40% increase.

But the flip side is: when panic strikes, this concentration becomes a double-edged sword. The market doesn’t differentiate “good” from “bad” semiconductor companies; it just sees Korea = memory = risk, and sells en masse.

When the pillar shakes, the building sways.

The Hand of Foreign Investors and the Fate of the Won

On March 3rd, foreign investors sold a net 5.18 trillion won (about $36 billion) of KOSPI component stocks — the second-largest single-day net sell in history. Over two days, they sold a total of 12.26 trillion won of Korean stocks.

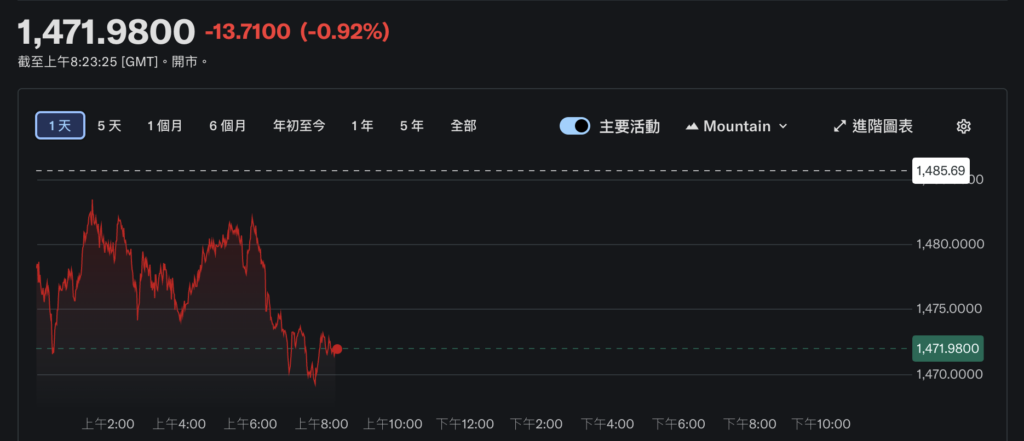

The won also collapsed in tandem. The USD/KRW exchange rate is now around 1,471, with the largest single-day depreciation in nearly a month.

A vicious cycle forms: foreign selling → converting won to dollars for export → won depreciation → Korean stock losses denominated in won increase → further foreign selling → continued won depreciation.

Korea’s reliance on foreign investors is among the highest in Asia. Data shows that foreign holdings account for about 30% of the free float market cap of KOSPI-listed companies. This means every global risk event makes Seoul one of the first targets for “sell first, ask questions later.”

Why do foreign investors prefer to sell Korean stocks first?

First, liquidity. KOSPI is one of Asia’s most active markets, with many stocks that can be sold quickly, unlike some emerging markets with liquidity shortages.

Second, high correlation. Korea’s economy is heavily dependent on global trade and tech cycles. Any global risk — war, oil prices, interest rates — directly impacts Korean companies’ fundamentals. This makes Korean stocks a natural proxy for global risk.

Third, hedging convenience. The Korean won is one of Asia’s most traded currencies, with relatively low costs for shorting. When risk aversion rises globally, shorting the won and Korean stocks often go hand in hand.

These factors combine to create a brutal reality: the movement of Korea’s stock market is largely dictated not by Koreans, but by fund managers in New York, London, and Singapore.

The Unshakable “Korea Discount”

Wall Street has a term for this phenomenon: the Korea Discount.

It refers to Korea’s stock market valuation consistently trading below similar markets. Latest data shows KOSPI’s P/E ratio is about 10.8x, compared to 15.4x for the broader Asia-Pacific region. Many large Korean conglomerates’ price-to-book ratios (PBR) are even below 1, implying the market values these companies below their net asset value.

The Korea Discount stems from multiple reasons.

Superficially, it’s about chaebol governance. Korea’s economy is dominated by a few family-controlled conglomerates: Samsung, Hyundai, SK, LG, Lotte. Their cross-shareholding structures are complex, minority shareholders’ rights are often diluted, dividend payout ratios are low, and corporate transparency is lacking. For international investors, putting money into companies where they can’t influence decisions or receive substantial dividends warrants a “discount” to compensate for risk.

The Korean government is aware of this. The 2024 “Corporate Value Enhancement Plan” aims to emulate Japanese reforms: lowering dividend income taxes, encouraging companies to increase shareholder returns. The strong performance of KOSPI in 2025 is partly attributed to optimistic expectations from these reforms.

But the deeper reason — “structural fragility of the economy” — cannot be fixed by a few policies.

Korea relies on Middle Eastern oil, global semiconductor demand, foreign investment willingness, and the stability of the won exchange rate. Any problem in these four variables can trigger a crisis. When two or more falter simultaneously — as now — the result is $2.7 trillion evaporated in 48 hours.

The script is always eerily similar: global crisis erupts → oil or currency swings wildly → foreign investors panic and sell Korean stocks → won depreciates further, fueling more selling → KOSPI becomes Asia’s worst market — history keeps echoing.

The Fate of High-Leverage Nations

Returning to the core question: why Korea? Because Korea’s economy is fundamentally a high-leverage gamble.

It bets almost everything on semiconductor and auto exports, relies on imported energy to operate, depends on foreign capital to sustain stock valuations, and needs a stable won for trade balance. When favorable winds blow — AI demand surges, oil prices stabilize, global trade flows smoothly — this model yields astonishing returns.

But high leverage means high fragility. When headwinds arrive, the same structure amplifies shocks. A 14% rise in oil prices might have three times the impact on Korea compared to other countries. A $3.6 billion foreign withdrawal could have ten times the impact on KOSPI as on the S&P 500.

Korea’s semiconductors can win global orders, but not energy independence. Its companies can lead in technology, but cannot prevent a strait blockade.

This is the structural fate of an export-oriented, energy-importing, foreign-investment-dependent economy — a fundamental crack that must be addressed.