a16z Analysis: AI costs halved, usage doubled, Americans in their 30s enter the era of "delayed adulthood"

a16z latest issue “Charts of the Week” dissects four major trends: AI tokens cost half as much but usage doubles, perfectly recreating the Jevons effect; tech giants’ AI capital expenditures approach the total new bank loans in the US; researchers at the Federal Reserve find Kalshi’s prediction market outperforms professional institutions in interest rate forecasts; marriage, homeownership, and childbirth rates among 30-year-olds in the US are declining across the board—college degrees are the only indicator rising against the trend, but “buyer’s remorse” sentiment is spreading. This article is based on a16z’s “Charts of the Week: DExit… real or feigned?” translated and written by Dongqu.

(Background: a16z’s 2026 outlook on 17 major potential trends in crypto)

(Additional context: Why are prediction markets really not gambling platforms?)

Table of Contents

Toggle

- Cheaper AI, more intense usage—Jevons effect reappears

- How exaggerated are AI capital expenditures?

- Kalshi outperforms professional prediction firms

- US 30-year-olds: less marriage, homeownership, and children

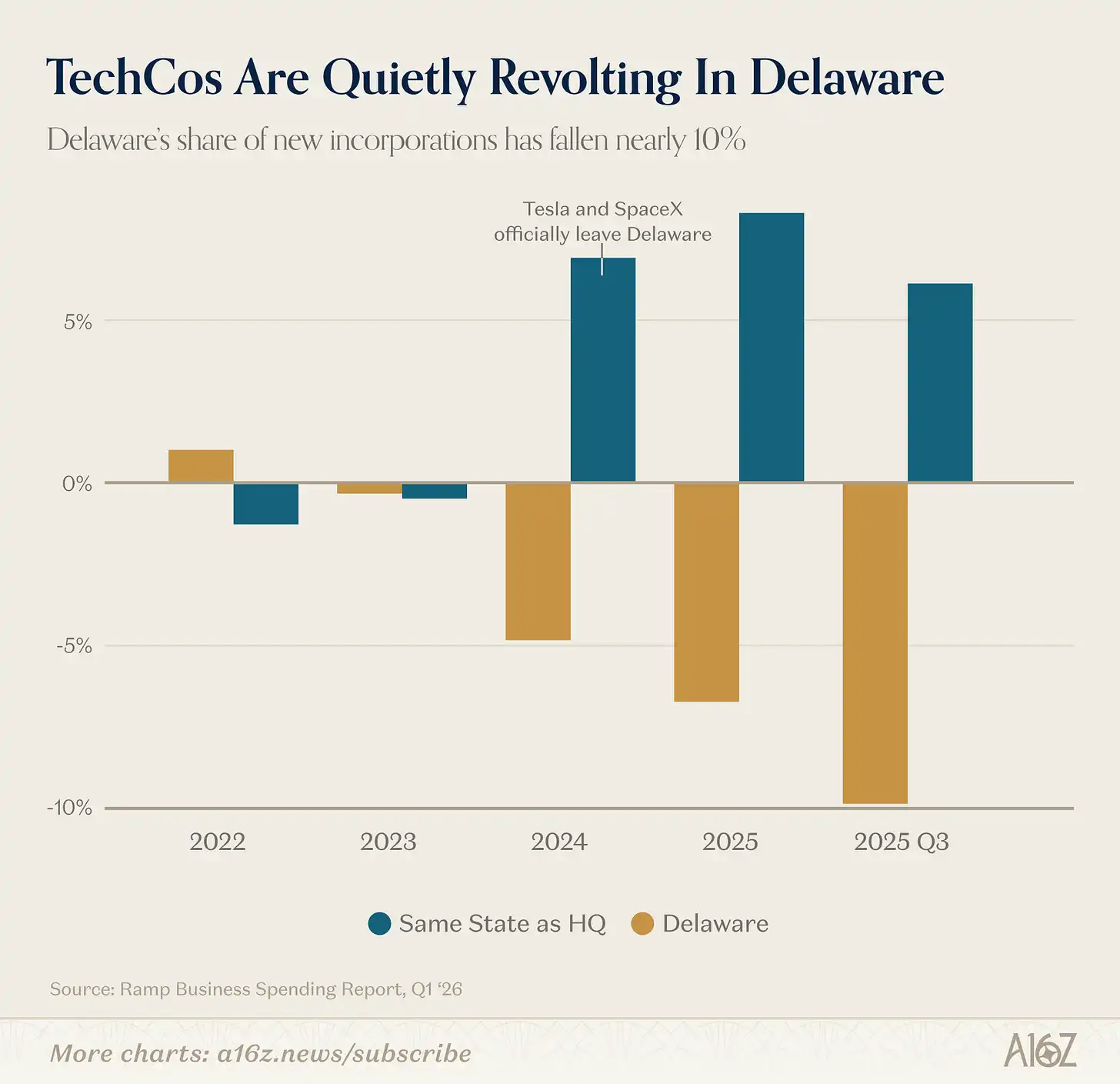

Delaware remains the top state for company registration in the US, but this status is gradually weakening:

According to Ramp, Delaware’s share of new company registrations has steadily declined since 2023, dropping about 10% in Q3 2025.

History doesn’t simply repeat, but it often rhymes… maybe.

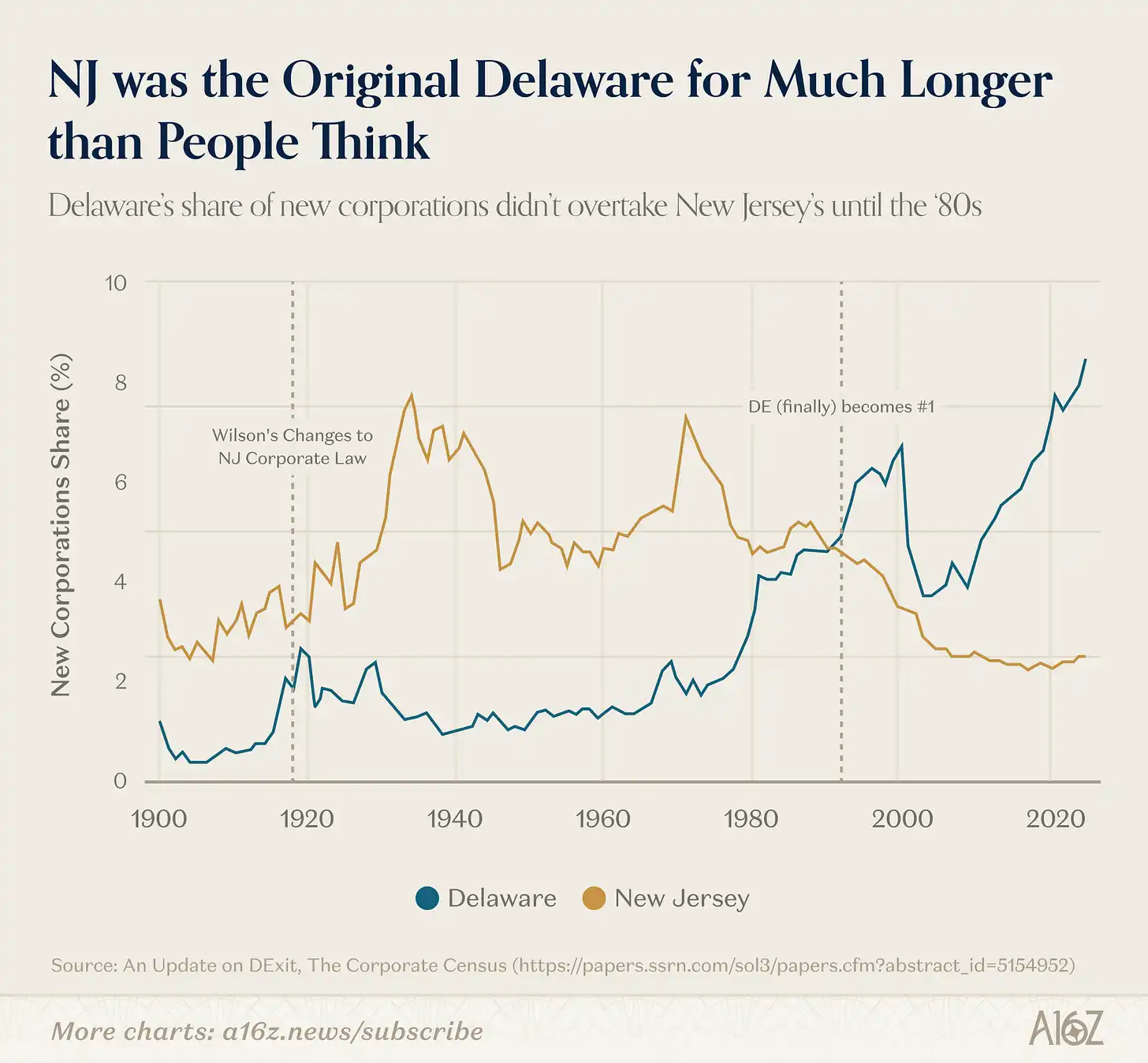

Delaware has not always been the corporate registration capital.

About a century ago, Delaware replaced New Jersey—the original “Trust Mother”—as the preferred registration state. New Jersey lost its edge because then-Governor Woodrow Wilson attempted to curb corporate abuses, severely deteriorating the business environment there. Delaware’s corporate law was modeled after pre-Wilson New Jersey law, and it absorbed many companies fleeing from New Jersey. Over time, with the Delaware Court of Chancery, it built a reputation over nearly 100 years as a fair and mature venue for resolving corporate and investor disputes.

However, the moat built over a century has shown cracks in just a few years. Regardless of who’s right, the Delaware Court of Chancery has recently adopted a more lenient stance on shareholder lawsuits (notably in several high-profile cases, including but not limited to Tesla), prompting companies to consider relocating their registration elsewhere. Good night, good luck, Delaware.

This is at least the mainstream narrative, but other data suggest the reality is far more complex.

First, even the founding myth of Delaware isn’t entirely accurate.

It wasn’t until the 1980s (about 60 years after Wilson’s governorship) that Delaware truly surpassed New Jersey as the top state for company registration:

New Jersey’s dominance lasted longer than mainstream narratives suggest. The catalyst for Delaware’s eventual overtaking was likely its legal framework related to director responsibilities, which made it especially attractive to public companies, combined with network effects that reinforced this inertia.

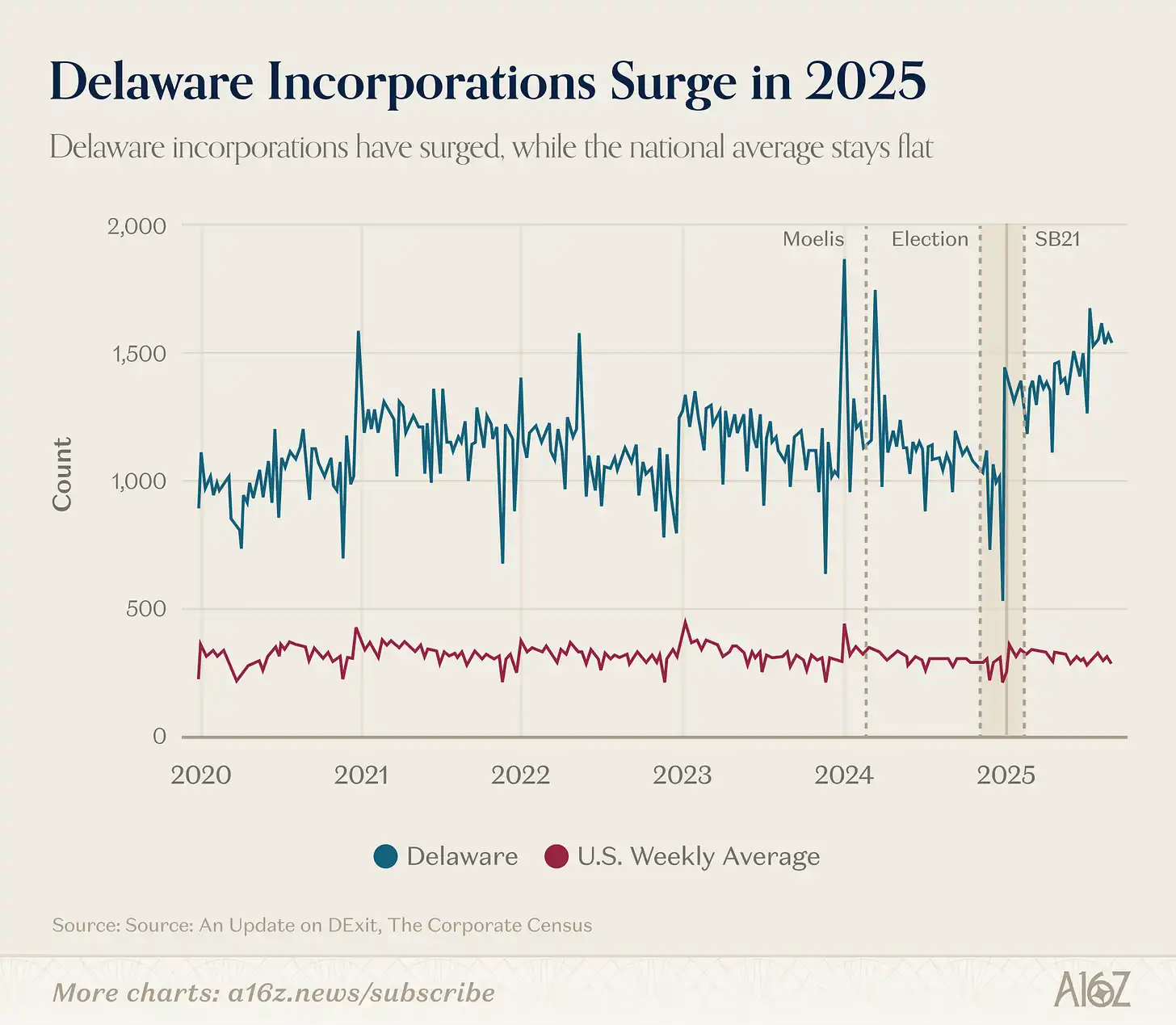

Second, regardless of what’s happening with high-profile IPOs (and the companies in Ramp’s data), Delaware overall still performs well—actually, it’s doing better than just “well”:

According to data from Harvard Law School’s Forum on Corporate Governance, from late 2024 through 2025, Delaware’s share of the total US corporate count actually increased significantly.

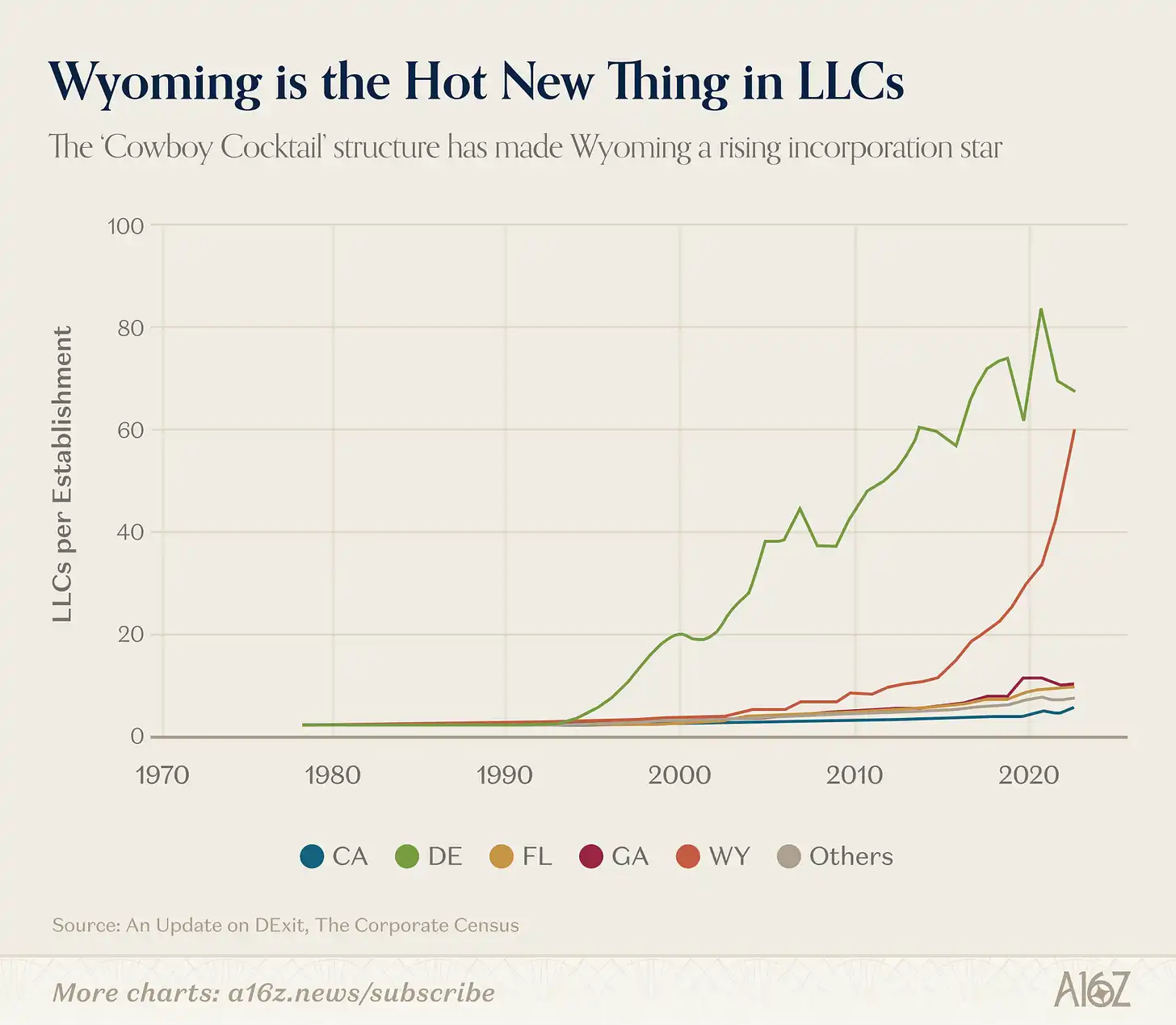

In fact, if you’re looking for a clear “DExit” case, it’s probably this one, and it has nothing to do with Tesla but involves a specific corporate form:

Wyoming LLCs started to surge around 2015.

Why? This is likely related to Wyoming’s LLC laws, which emphasize asset protection and privacy, and the state promotes this corporate structure as a “cowboy cocktail.”

In summary, the point isn’t that DExit isn’t happening (since at least some data indicate it is—though only a few high-profile companies moving out is significant), but that the reality is more nuanced than the market narrative suggests.

Ultimately, Delaware still holds the advantage of the “default option,” reinforced by years of network effects, making it difficult to dislodge.

a16z has previously shared an early version of this chart, but as data accumulates, the effect becomes more astonishing.

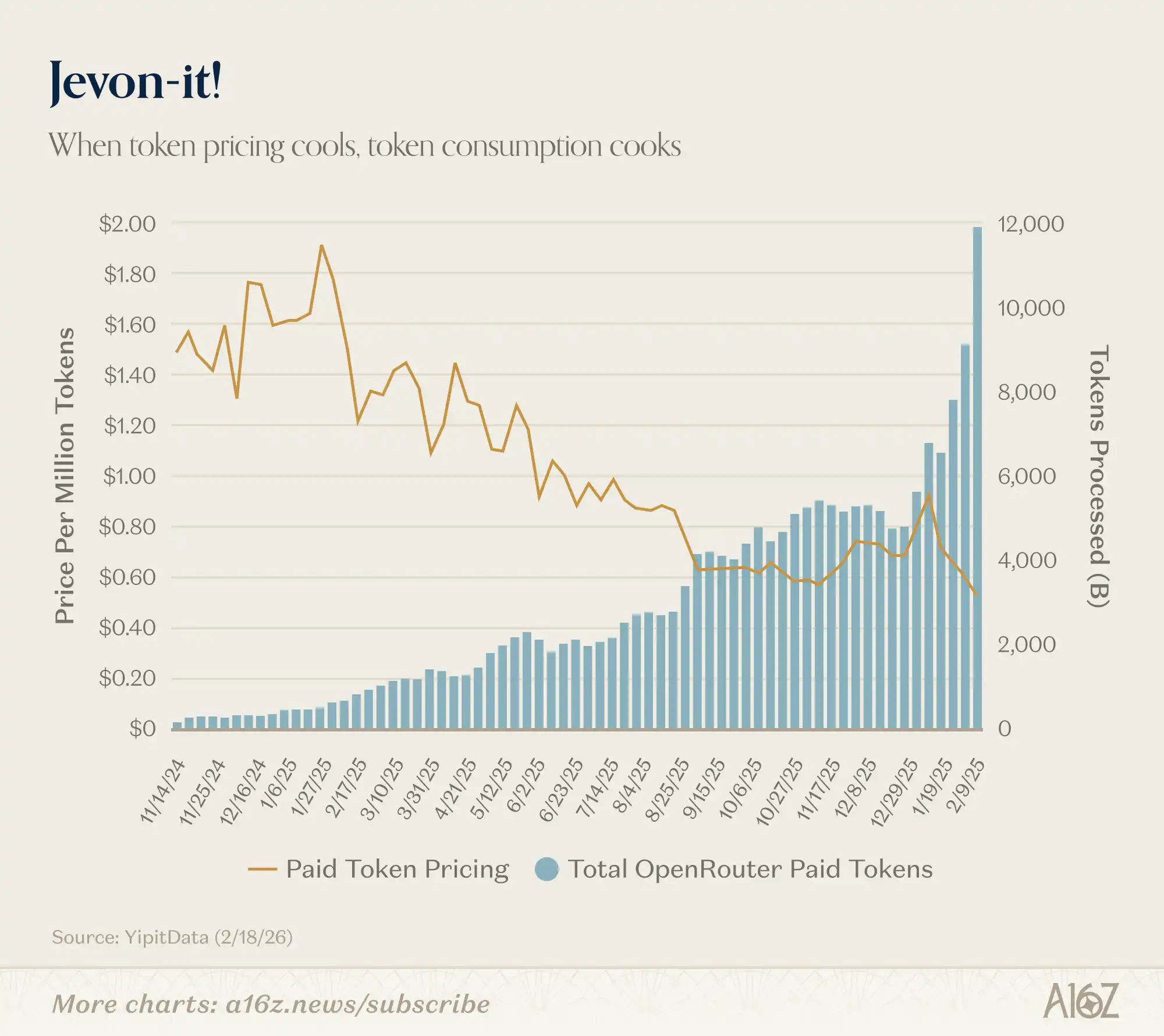

Cheaper AI, more intense usage—Jevons effect reappears

Token prices fall, but token usage surges against the trend:

Since the beginning of this year, paid token prices have dropped from about $0.90 per million tokens to $0.50, while the volume of tokens processed nearly doubled—from around 6,000 to 12,000.

This is textbook Jevons effect: the cheaper AI gets, the more people use it. Exciting.

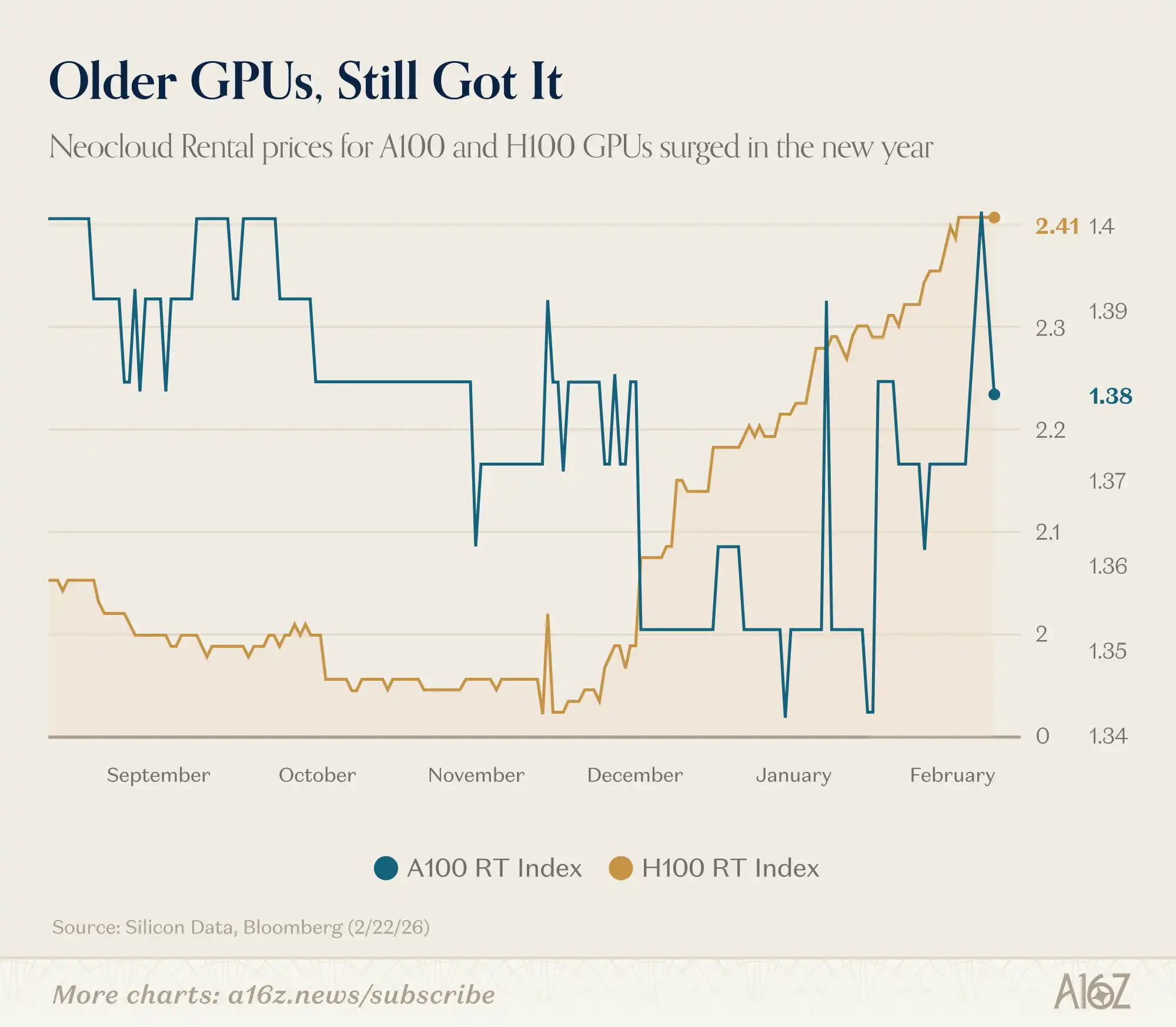

Remember when someone said that once better GPUs come out, old GPUs will be worthless?

It seems that’s not entirely true:

According to Silicon Data, the rental prices for NVIDIA H100 and A100 have both increased this year.

The market is still far from oversupply of computing power; even existing demand has not been fully satisfied.

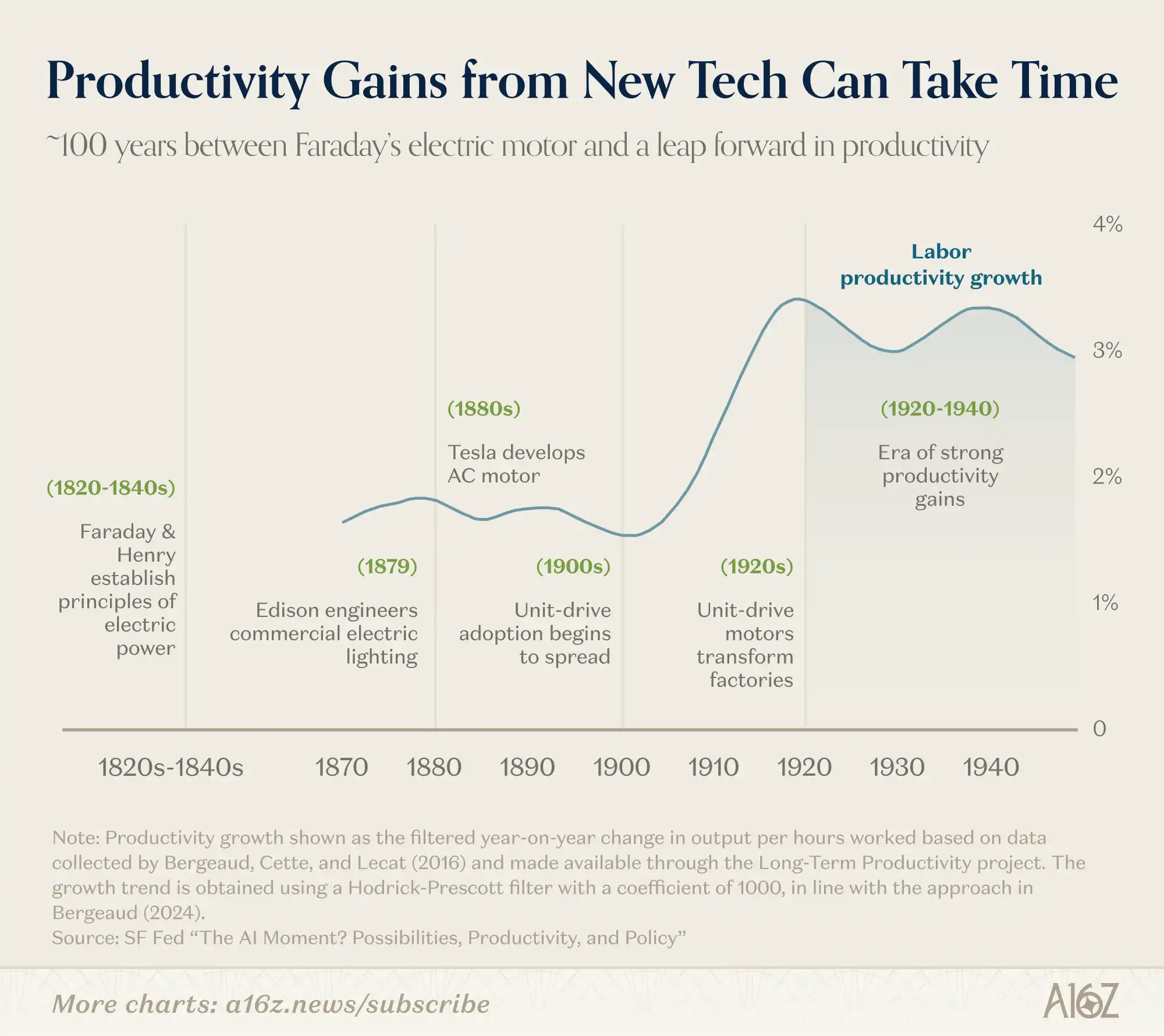

This comparison isn’t perfect, but if history offers any clues, we might need more time to truly understand what an AI-driven “economy” looks like:

From Faraday and Henry’s initial discussions of electricity, to the industrial productivity boom of the early 20th century, it took about 100 years.

Since the 1820s, technological iteration cycles have indeed sped up, but a platform-level shift involves many variables.

Roy Amara’s famous quote: “We tend to overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten.”

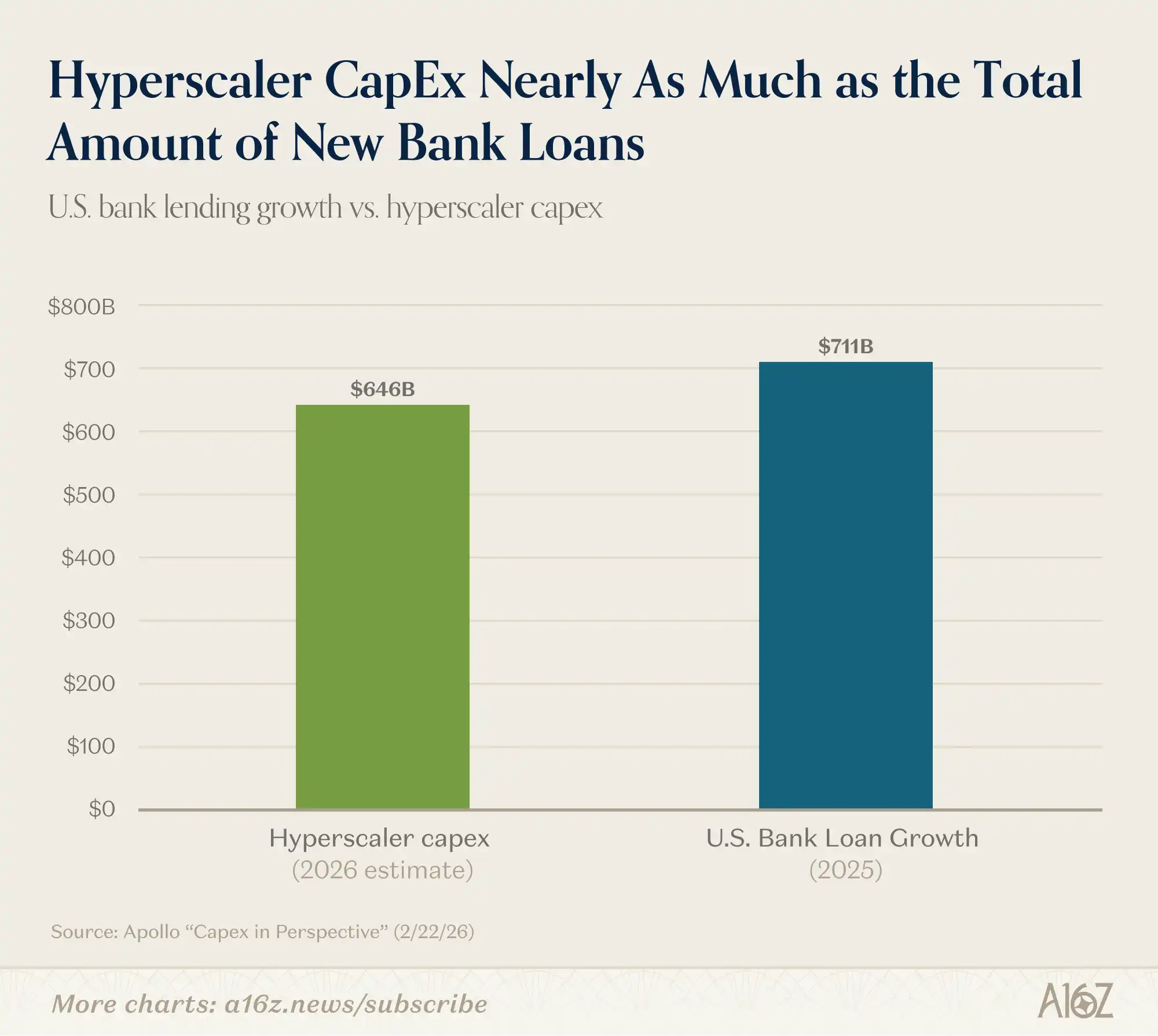

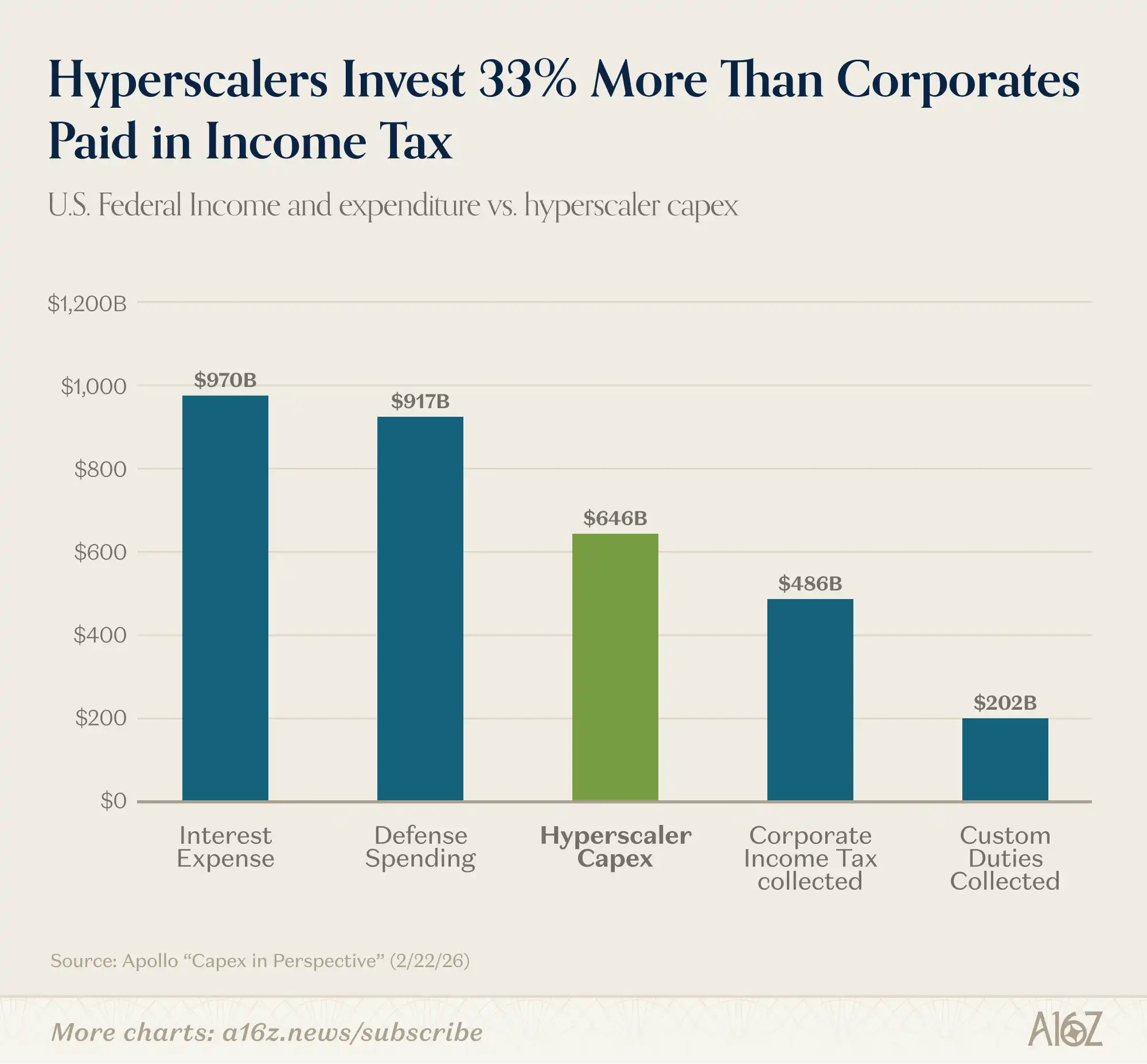

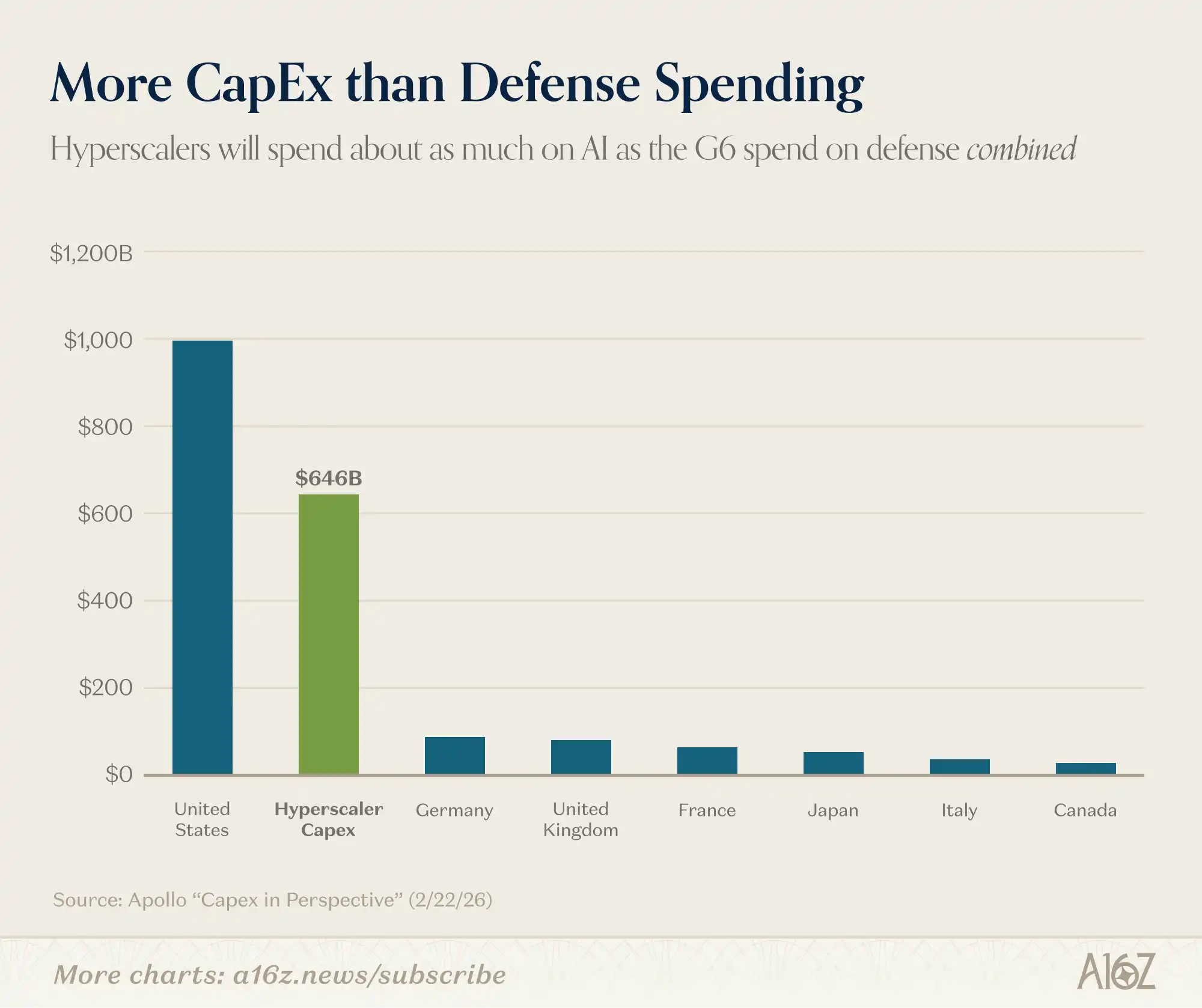

How exaggerated are AI capital expenditures?

Look at this set of staggering data: AI capital expenditures are far beyond what you might imagine.

Compare:

Projected AI capital expenditure in 2026 will approach the total net new bank loans in the US in 2025:

Capital expenditure is about 33% higher than total corporate income tax revenue in the US, roughly three times the total tariffs:

It’s about six times the combined military budgets of any G7 country:

So, yes, AI capital spending is truly off the charts.

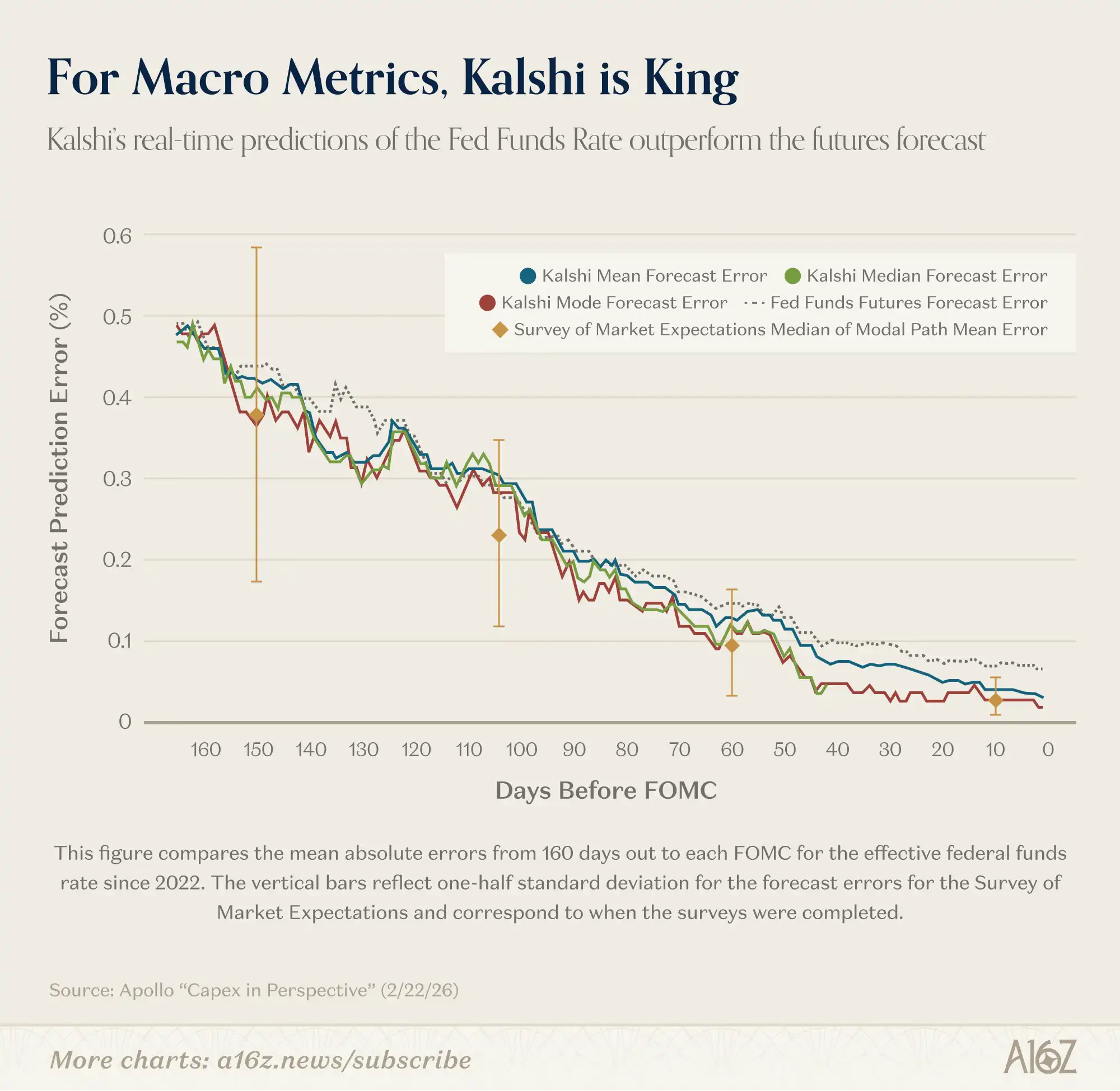

Kalshi outperforms professional prediction firms

Federal Reserve researchers believe prediction markets are impressive.

At least on one metric, Kalshi’s forecasts for the federal funds rate have already surpassed those of professional prediction firms:

For the forecast of the federal funds rate 150 days ahead (after three FOMC meetings), Kalshi’s mean absolute error is very close to that of professional forecasters. Unlike surveys that only provide modal paths every six weeks, Kalshi offers continuous updates of full probability distributions… We found that Kalshi’s median and mode predictions perfectly matched the actual rate the day before the FOMC meeting, a statistically significant improvement over federal funds futures forecasts.

In other words, although all predictors start at similar points, Kalshi’s continuously updated forecasts keep improving over time, ultimately achieving perfect prediction the day before the rate is officially announced. Moreover, Kalshi outperforms futures market predictions.

Kalshi’s advantage isn’t limited to the federal funds rate. As Fed researchers point out, because macro indicators like inflation, growth, and unemployment lack other options markets, Kalshi is the only place providing “high-frequency, continuously updated, rich probability distributions” that reflect the “public’s” judgment on these economic indicators.

This is significant.

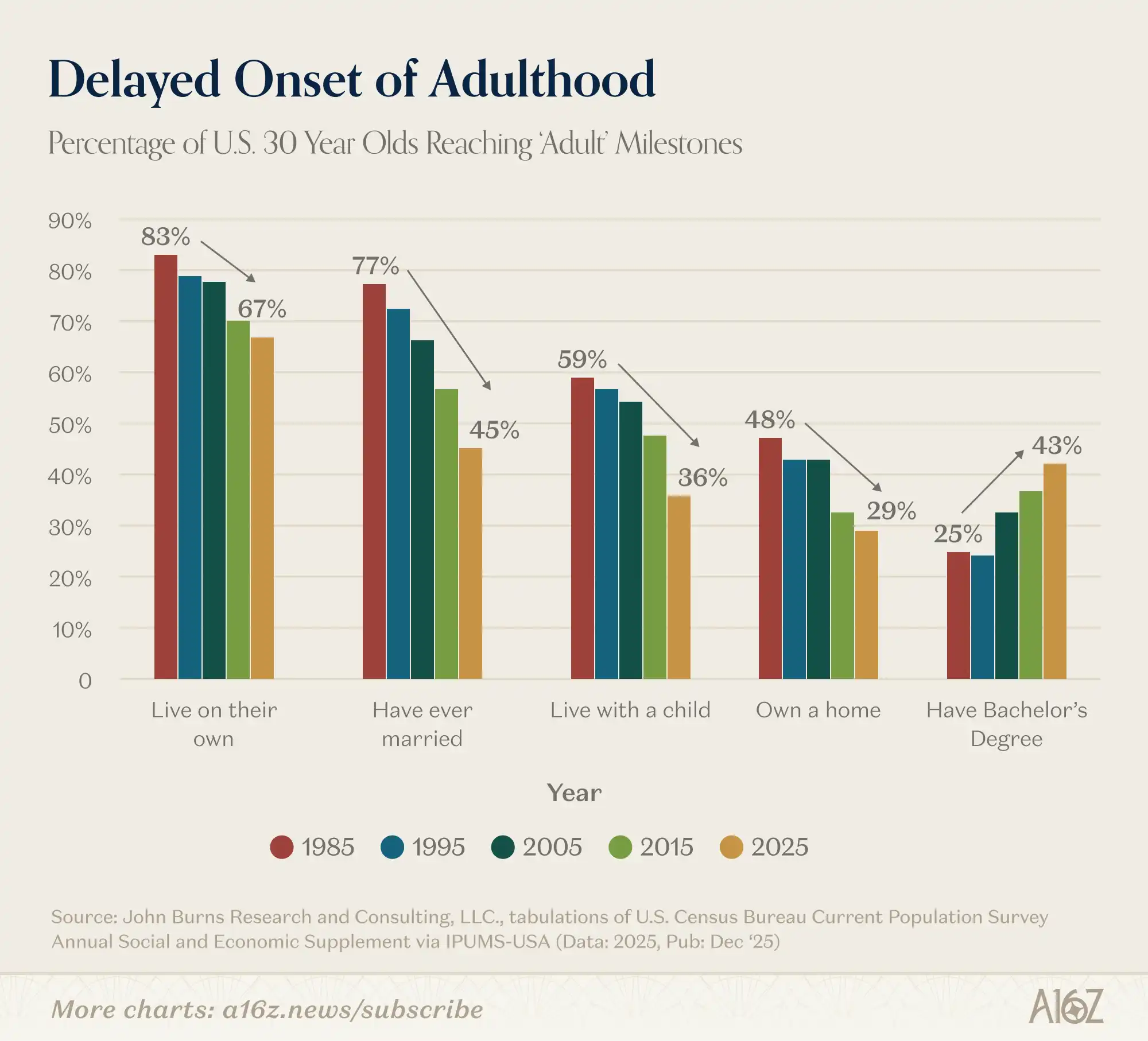

US 30-year-olds: less marriage, homeownership, and children

Finally, a thought-provoking chart with brief commentary:

The proportion of 30-year-olds reaching key life milestones has been declining since at least the 1980s.

Among 30-year-olds, fewer and fewer are:

Living independently;

Getting married;

Living with children;

Owning their own home.

The only exception is college enrollment—the proportion of 30-year-olds with a bachelor’s degree has nearly doubled since 1995.

So, is college worth it?

Milestones? For this generation, more like a millstone around the neck.

Maybe yes, maybe no, but the “regret after reading” atmosphere is definitely spreading.