Why did the central bank suddenly intervene to stabilize the exchange rate?

Author: Ba Jiuling, Wu Xiaobo Channel

As the RMB exchange rate surges upward, the central bank finally steps in personally to stabilize the exchange rate.

On February 27, 2026, at 8 a.m., the People’s Bank of China issued an announcement: To promote the development of the foreign exchange market and support enterprises in managing exchange rate risks, it has decided that starting March 2, 2026, the foreign exchange risk reserve ratio for forward sale of foreign exchange will be reduced from 20% to 0%.

The announcement is brief, but its effects are immediate. The offshore RMB exchange rate, which was trading at 6.839 yuan per dollar, quickly depreciated by 0.3%, reaching a high of 6.859, putting a pause on the continuous appreciation of the RMB.

So, what exactly is the foreign exchange risk reserve for forward sale? How will this policy affect the exchange rate, investors’ wallets, and import-export companies?

The soaring RMB exchange rate

To understand this policy, we first need to discuss why the central bank took action.

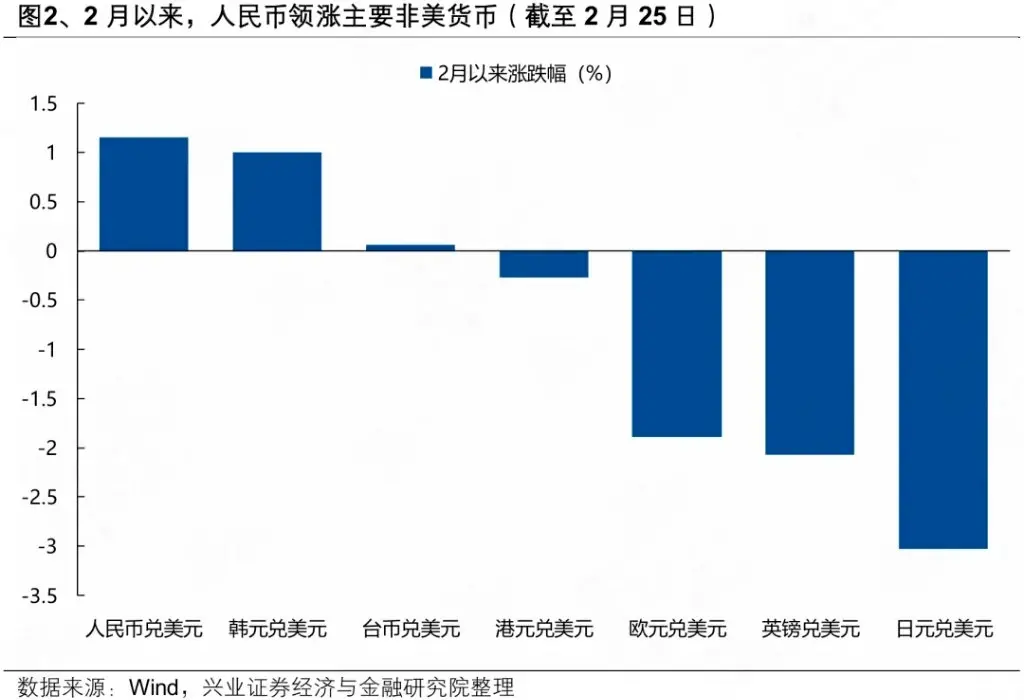

Since last December, when the RMB exchange rate broke through 7, the RMB against the dollar has entered an “accelerated” phase. In just three trading days after the Spring Festival holiday, it appreciated by over 800 points. Notably, on February 26, 2026, the intra-day increase exceeded 2%.

The reasons for RMB appreciation are not complicated.

First, external factors, with the continued weakening of the US dollar being the main driver.

As the Federal Reserve began a rate-cut cycle, the market generally expected the dollar to continue depreciating. Coupled with other factors, this led to a persistent decline in the dollar index, which fell from 100 last year to 95.5 in January this year.

Second, internal factors. China’s economic resilience has laid a foundation for RMB strength. Upgrading export structure, enhanced manufacturing competitiveness, and a high current account surplus all support the RMB’s fundamentals. Data shows that China’s trade surplus reached $1.19 trillion in 2025, giving many export companies large amounts of US dollars.

When these companies, taking advantage of the Spring Festival, began “settling” their foreign exchange—selling dollars to buy RMB—it further propelled RMB appreciation.

The combination of internal and external factors creates what is called a “procyclical effect”: dollar depreciation triggers more foreign exchange settlement, which in turn promotes further appreciation, forming a positive feedback loop.

Wang Qing, Chief Macro Analyst at Orient Securities, believes that the recent RMB rally, marked by offshore RMB leading the way, reflects heightened market sentiment, further boosting the RMB’s rise.

However, the central bank’s goal in exchange rate management is to base it on market supply and demand, guide expectations through reinforcement, prevent excessive fluctuations, and keep the RMB exchange rate generally stable at a reasonable and balanced level.

If the RMB exchange rate deviates sharply from fundamentals with rapid rises or falls, regulatory tools will be decisively used to send clear policy signals and prevent excessive RMB appreciation.

For some, a stronger RMB is a good thing, but for export companies, the situation is quite the opposite.

In 2025, China’s net exports contributed 32.7% to economic growth. If the RMB appreciates too quickly or too much, the impact on export companies will gradually become evident.

Media reports indicate that after surveying several export-oriented listed companies, RMB appreciation has already significantly impacted their operations.

For example, a listed company in the smart mobility sector reported a foreign exchange impact of 130 million yuan in Q4 2025. Although the company used hedging tools to manage risks and realized a hedging gain of 53 million yuan, it still lost between 70 and 80 million yuan in net profit.

Guan Tao, Chief Economist at Bank of China Securities, states: If domestic companies receive export payments in USD, they will suffer foreign exchange losses due to RMB appreciation. The nominal bilateral RMB exchange rate appreciation evolving into an effective real exchange rate appreciation will affect their export competitiveness.

Against this backdrop, the central bank has introduced a new tool: the “forward sale foreign exchange risk reserve.”

The central bank’s toolbox

To understand this tool, we need to clarify four key concepts: foreign exchange settlement, foreign exchange sale, forward sale of foreign exchange, and foreign exchange risk reserve.

Foreign exchange settlement refers to enterprises and individuals selling their foreign currency to banks in exchange for RMB, while foreign exchange sale means enterprises and individuals using RMB to buy foreign currency from banks.

The so-called forward sale of foreign exchange is a derivative product offered by banks to help enterprises hedge against exchange rate risks. Generally, to avoid exchange rate fluctuations, export companies prefer to lock in rates in advance through forward sales, options, and other instruments. Enterprises do not immediately buy foreign currency; banks involved in this business need to purchase foreign currency in the spot market, which can influence the spot exchange rate.

As for the foreign exchange risk reserve, it traces back to the “8.11 exchange rate reform” in 2015.

To address the significant volatility of the RMB exchange rate at that time, the central bank introduced a series of innovative policy tools, one of which was the “foreign exchange risk reserve.” It requires banks to deposit a certain proportion of their foreign exchange transactions as a guarantee with the central bank.

Bank staff counting US dollars

So, how does this tool help “cool down” the RMB’s movement? It involves a complex transmission chain.

First, according to the central bank’s regulations, each forward sale of foreign exchange by a bank requires setting aside a portion of funds as a deposit with the central bank. Since this deposit earns no interest, it imposes a higher cost on banks engaging in forward sales.

Now that the central bank has lowered the forward sale foreign exchange risk reserve ratio, banks no longer need to freeze interest-free foreign exchange funds, significantly reducing the cost of forward sales.

With lower business costs, banks can offer cheaper forward purchase of USD to enterprises, encouraging importers with demand to buy USD forward in advance.

As a result, more enterprises and banks sign forward sale contracts. To hedge risks, banks immediately buy USD in the spot market, increasing demand for USD. Since the USD/RMB exchange rate is a seesaw, increased demand for USD will slow down RMB appreciation.

This approach has been used by the central bank multiple times before.

For example, on October 10, 2020, the central bank announced that the foreign exchange risk reserve ratio for forward sales was reduced from 20% to 0%. The goal was to slow the pace of RMB appreciation. The current policy change is almost a replay of what happened six years ago.

Liu Tao, senior researcher at Guangfa Securities, believes that lowering the foreign exchange risk reserve ratio for forward sales shifts from emergency measures to normalize management, allowing market mechanisms to play a fuller role, guiding rational expectations about exchange rate fluctuations, reducing procyclical “herd behavior,” and maintaining the RMB’s basic stability at a reasonable and balanced level.

Wen Bin, Chief Economist at Minsheng Bank, states that with no current pressure for RMB depreciation, the countercyclical adjustment tools should be phased out, returning policies to a neutral stance and reducing direct market intervention.

After policy implementation, what are the impacts?

The central bank’s policy adjustment is a tangible benefit for enterprises.

Liu Tao explains: “Previously, the 20% foreign exchange risk reserve for forward sales was paid by banks. But in practice, some banks might pass this hidden cost onto enterprises by adjusting forward quotes or widening spreads.”

For example, if a bank conducts a forward sale of $1 million, with a 20% reserve ratio, it needs to set aside $200,000 as foreign exchange risk reserve, deposited interest-free with the People’s Bank for a year.

In this case, this cost is ultimately borne by the enterprise that enters into the forward contract, which may reduce their enthusiasm for forward purchase of foreign currency. When the reserve ratio drops to zero, enterprises with actual trade needs can buy foreign currency at lower costs.

For small and medium-sized enterprises, the cost of using forward sales to lock in exchange rates was not low, which led some firms that could have hedged exchange rate risks to abandon the tool due to “cost concerns.”

Now that the reserve ratio is lowered to zero, the central bank encourages more SMEs to hedge exchange rate risks through forward sales, stabilizing production expectations and better serving the foreign exchange needs of the real economy. For importers with thin profit margins, this effectively increases their profits.

It’s worth noting that in 2025, China’s foreign exchange market trading volume reached $42.6 trillion, with the foreign exchange hedging ratio among enterprises rising to 30%, both hitting record highs.

This data indicates that Chinese companies are increasingly aware of exchange rate risk management, and hedging has become a “standard operation” for more and more firms. This policy adjustment is expected to further raise that ratio.

How should investors respond to RMB fluctuations?

For investors focused on foreign exchange, RMB volatility impacts asset allocation, such as USD assets, Hong Kong dollar investments, etc.

Many institutions and experts agree that currency exchange should be based on personal needs; unilateral bets are not advisable. In other words, individual investors should manage exchange rate risks according to actual needs rather than using the currency as a speculative tool.

Li Nan, Associate Professor at Shanghai Jiao Tong University’s School of Finance, points out: Currently, the interest rate difference between USD deposits and RMB deposits is about 2%. As long as the USD depreciates by 2% against the RMB, this interest rate gap disappears. If the USD depreciates more than 2%, it’s better to hold RMB directly.

For investors already holding USD assets, some experts suggest splitting their USD holdings into several parts and gradually closing positions at different exchange rates to reduce the risk of missing out or chasing highs.

For individuals with genuine needs such as studying abroad, traveling, overseas shopping, or overseas payments, it’s advisable to retain a certain amount of USD. Those holding USD purely for interest rate differentials without actual needs should modestly reduce their USD holdings during RMB strength periods.

Final thoughts

Overall, the central bank’s reduction of the forward sale foreign exchange risk reserve ratio is essentially a move toward policy normalization. From 2015 to 2025, the central bank adjusted the foreign exchange risk reserve ratio five times.

From the large fluctuations after the “8.11 reform” to the current increased flexibility and two-way volatility of the RMB exchange rate, the central bank has repeatedly demonstrated its ability to guide exchange rate trends and prevent risks at critical moments.

In a turbulent external environment, both individual investors and enterprises need to learn to coexist with exchange rate fluctuations.

As the central bank repeatedly emphasizes: adhere to the concept of neutral exchange rate risk, and strengthen risk management. This is not just empty talk but a compulsory lesson for every market participant.