DeFi Upward, Users Downward: The New Paradigm of CeDeFi Curator - ChainCatcher

Author: Danny @IOSG

The Explosion of the Curator Model

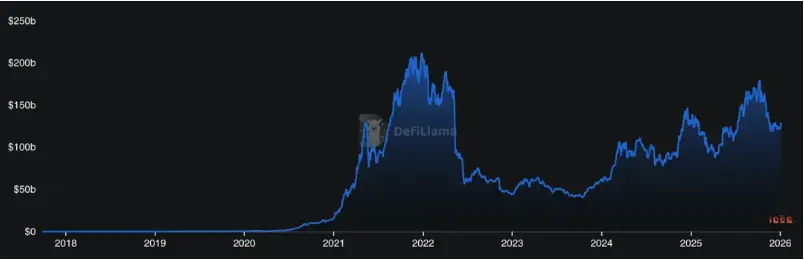

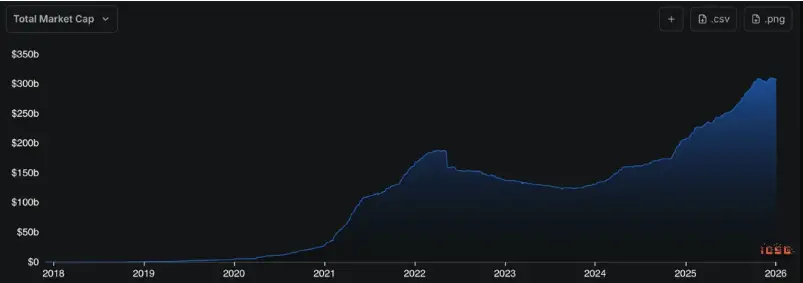

DeFi activity has returned to levels close to DeFi Summer, but on-chain stablecoin supply continues to expand. This means there is more and more money on-chain, while DeFi product forms are temporarily difficult for broader users to understand, use, and distribute.

▲ DeFi TVL, Source: Defillama

▲ Stablecoin Market Cap, Source: Defillama

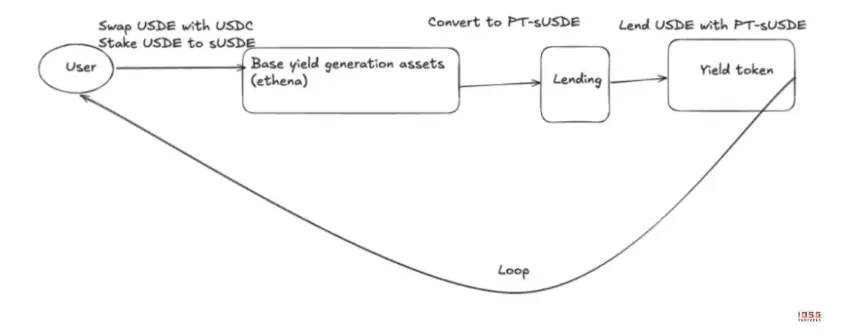

In recent years, DeFi infrastructure has solved issues of accessibility and composability but has become an extremely complex game. For ordinary users, what appears to be simple stablecoin yields may actually involve lending spreads, multi-layer incentives (Funding/airdrops), structured products (Pendle), and leverage looping.

▲ USDE AAVE Pendle loop

Risks have long exceeded the scope of contract hacks, evolving into the amplification of LTV, liquidation liquidity, and oracle risks. For example, in October 2025, an internal oracle failure at Binance caused the USDe price on its platform to briefly crash, triggering a chain of liquidations.

DeFi is experiencing an “counterintuitive” evolution: as technology matures (upward), user understanding costs and risk assessment difficulty increase (downward). When individuals can no longer identify “whose money is being earned” and “where the risks are,” DeFi growth hits a ceiling.

The Curator role emerged to address this distribution problem. Chinese lacks a direct translation; it is more akin to “strategist.” As yield provision and risk pricing power shift from protocol layers, Curators have become an encapsulation layer connecting complex protocols with broad capital.

What Exactly Do Curator Businesses Do

In systems represented by Morpho, protocols provide neutral infrastructure, while the decision of which assets are available, risk levels, and daily management is handled by the Curator. It bears three core responsibilities:

Strategy Selection

The value of a Curator lies in judging which yields are structural and which are merely opportunistic. Strategies are not one-time deployments; they need continuous adjustment based on fund size and risk exposure. For example, different Curators employing USDC strategies can have vastly different outcomes under extreme market conditions. The fundamental difference is whether they possess the ability for ongoing judgment and dynamic leverage reduction.

Risk Pricing

In a modular system, the true determinant of risk exposure is the Curator. What collateral to accept, how high to leverage—these are fundamentally risk pricing decisions. The Curator holds the power of risk pricing, not just execution. Even top-tier Curators can make mistakes; for instance, Re7 Labs relied on the Pyth oracle, which delayed price updates, leading to incorrect liquidations. This warns us that the greatest systemic risk in the current cycle stems from this.

Product Distribution

For users, productization offers a single entry/exit interface; for frontends (CEXs/wallets), it provides non-custodial, risk-transparent yield modules. It’s not about competing for protocol users but helping capital find understandable and tolerable risk structures.

Curator is an AUM-driven asset management business. Because revenue is strongly tied to AUM, there is an incentive tension: expanding AUM can amplify income, but rapid expansion may erode strategy capacity and magnify tail risks.

Market cycles directly influence Curator behavior. In bull markets, Curators tend to amplify capital efficiency, using leverage, layered incentives, and looping structures; more lenders participate, risk is masked by Beta, APYs are high, capacity is large, but risks are also elevated.

In contrast, during volatile or bear markets, strategies revert to real yield sources: lending spreads, cash-flow assets like RWA, and low-correlation allocations. Real yields surpass leverage and airdrops, with higher defensive capacity than offensive.

▲ Defillama: Curator

Evolution of Distribution Paradigms: Institutional Adoption and Retail Future

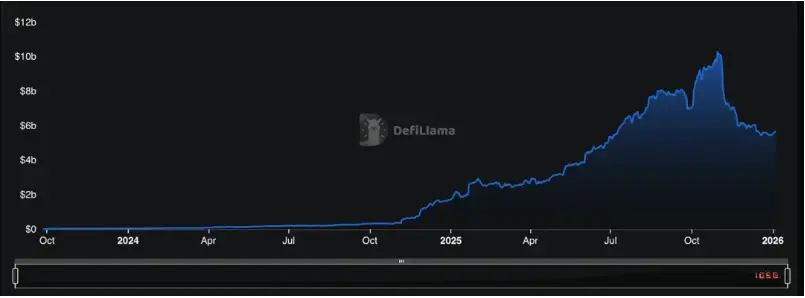

Risk Curator Protocols’ total TVL ≈ $5.68 billion

AUM is highly concentrated, with leading players like Steakhouse Financial (~$1.55B), Gauntlet (~$1.23B), accounting for nearly 50% of the market share, forming a typical power-law structure.

As Curator management assets continue to grow (annual growth rate 2000%), their role has evolved from strategy executor to a central node of DeFi risk and liquidity.

▲ Curator AUM, Source: Defillama

According to DefiLlama data, as of February 2026, the total TVL of Risk Curators is about $5.9 billion, with Steakhouse Financial ($1.53B), Sentora ($1.34B), and Gauntlet ($1.29B) collectively holding nearly 70% of the market share, showing significant top-heavy concentration. This means that if the leading Curators’ strategies or parameters deviate systemically, the impact will far exceed that of any single protocol.

In the future, Curators will not converge into a single form but will at least differentiate into three categories:

First, Capacity-First Curators

These Curators focus on hosting large-scale, low-volatility capital, with strategies leaning toward lending spreads, stable incentives, and RWA yields—emphasizing conservative parameters and transparency. They are more easily integrated into CEXs, wallets, and Fintech frontends, representing the mainstream form of large Vaults on Morpho. Some protocols even delve into Vault tech stacks to build more institution-friendly Curator businesses from the ground up.

Most large-capacity Curators currently act as borrowers, redistributing their managed AUM to more diverse, aggressive-yielding Curators—deciding whom to lend to, thus generating more returns for their AUM. They often serve as “Curator of Curators,” working closely with opportunity-driven Curators discussed later.

For institutions entering DeFi, the choice becomes either building their own Curator or partnering with top-tier ones, actively participating as curators. Morpho’s open, modular architecture makes it the preferred infrastructure for institutional Curator building. Bitwise, for example, launched a non-custodial vault Curator service managed by its internal team on Morpho in January 2026, marking a shift from DeFi users to builders.

Coinbase, on the other hand, chose a different path: outsourcing its lending products (USDC lending, collateralized loans in XRP, ADA, etc.) to third-party Curator Steakhouse Financial on Morpho—front-end familiar to users, back-end driven by DeFi, known as the “DeFi Mullet” model.

▲ Coinbase DeFi Mullet

Institutional involvement is rapidly increasing. Apollo Global Management, managing over $938 billion, signed a strategic partnership with Morpho in February 2026, planning to acquire up to 9% of $MORPHO governance tokens over four years. Their strategy is twofold: their credit funds have tokenized RWA assets like ACRED and ACRDX via Securitize and Anemoy, integrated into Morpho’s lending markets through top Curators like Steakhouse; simultaneously, holding governance tokens allows direct influence over the future of on-chain credit infrastructure.

In the same month, Taurus, which provides custody services for over 40 banks, integrated Morpho into its custody platform, enabling traditional financial institutions to allocate funds directly into Morpho Vaults within existing compliance frameworks, with Curators managing the assets. The question of institutional entry into DeFi has shifted from “whether to participate” to “at what level.”

Second, Opportunity-Driven Curators

These Curators focus on new structures, assets, and early incentive windows, willing to sacrifice capacity and take risks for higher alpha. They typically have clear AUM caps, short strategy lifecycles, and high volatility tolerance, serving professional funds or DeFi communities. They jump into emerging L1/L2 ecosystems, such as Hyperliquid, Plasma, Monad, Megaeth, often with lucrative liquidity incentives to attract early users and developers. Opportunity-driven Curators are among the first to deploy vaults on new chains, leveraging their expertise to capture early bonuses like airdrops and high liquidity mining rewards.

Additionally, these Curators explore new assets, structures, and DeFi primitives. Unlike blue-chip Curators focusing on mature assets (ETH, USDC), opportunity-driven ones are more willing to incorporate new asset classes. For example, Re7 Labs became a RWA asset Curator for BlackRock’s BUIDL, pioneering large-scale RWA applications in lending.

This type of Curator is highly sensitive to market changes, capable of rapid responses and arbitrage during volatility or specific events. Their strategies often involve complex logic, such as cross-protocol interest rate arbitrage or liquidation profit extraction. Although riskier, they can deliver returns far exceeding market averages.

Third, Productized Curators

Productized Curators no longer just configure backend strategies but encapsulate them into Vault-as-a-Service, assets, or stablecoins, directly facing users. This path demands high standards for risk control, transparency, and accountability, but once established, offers the highest distribution efficiency.

The challenge for these Curators is to find high-yield, large-capacity strategies—most DeFi strategies have clear capacity limits. For example, current mainstream looping/basis strategies have a market size approaching $20B (about 10% of DeFi TVL), up from around $5B six months ago. Once capacity is filled, marginal returns decline sharply, and parameter tolerance shrinks.

Successful productization of such Curators can better integrate into Fintech apps and Web2 capital, becoming a crucial step toward mass adoption.

Returning DeFi to Users

The biggest current problem in DeFi is that complexity and risk exposure methods have exceeded individual users’ decision-making capacity, leading to distrust in saving. Incidents like StreamFinance’s yield-stablecoin misuse causing crashes, combined with a bear market, have caused overall yield-bearing stablecoin TVL to decline, with funds shifting back to conservative lending protocols.

Today, about 45% of DeFi TVL (~$56B) is chasing new yield opportunities, concentrated in protocols like Aave, Morpho, Spark, but large amounts of USDC remain idle long-term. The reason isn’t lack of opportunities but high costs of strategy understanding, risk judgment, and dynamic management.

For most users, what they truly need is:

- Simple, trustworthy entry points;

- Diverse, constantly adjustable yield structures;

- Clear, understandable risk exposure methods;

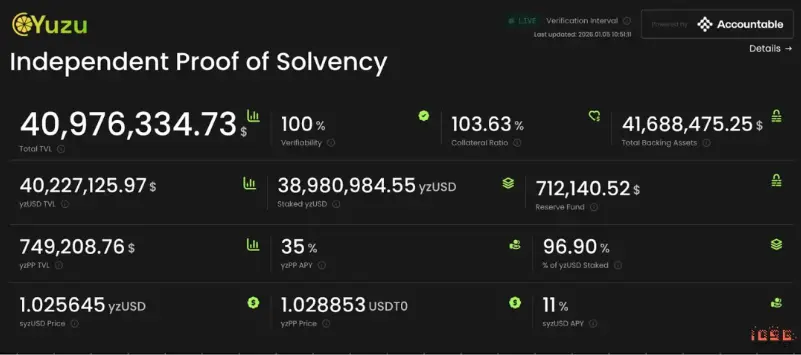

Entry points can be streamlined through consolidating current Vault exposures or productization. Yield structures can be improved by introducing more high-quality Curators to the market. What’s most needed now is building a healthy, transparent Curator audit system, including:

- On-chain verifiable asset allocation paths;

- Structured risk annotations;

- Clear exit conditions and paths in extreme scenarios.

This won’t eliminate risks entirely but can transform systemic uncertainty into understandable, priced choices. Without such transparency, Curators risk becoming shadow banking systems, no different from Celsius or BlockFi. Conversely, if Curators can break down, price, and pre-collect risks at the intermediary layer, they could serve as buffers rather than amplifiers, helping professionalize DeFi risk management.

▲ DeFi Dashboard for Asset Management Transparency

In the long run, Curator is not the final form of DeFi, but it is an almost unavoidable layer before DeFi reaches larger user bases. DeFi has proven the feasibility of its infrastructure; what’s missing now is the middle layer capable of packaging, distributing, and embedding these capabilities into real-world use cases. Curator is taking on this role.

When complexity is reasonably encapsulated, risks are clearly annotated, and responsibility boundaries are sufficiently transparent, DeFi can truly return to its original promise: not just serving a niche of professionals but becoming a broadly accessible financial system.

References

[1] BeInCrypto. (2025, October 12). Ethena USDe “Depeg”, What Really Happened?. Retrieved from

[2] Blockworks. (2025, March 20). Who’s responsible when something breaks in DeFi?. Retrieved from

[3] Chorus One. (2025, December 2). DeFi Curators in 2025: Navigating Chaos, Building Resilience. Retrieved from

[4] DefiLlama. (2026, February 24). Risk Curators Rankings. Retrieved from

[5] Chorus One. (2025, December 2). DeFi Curators in 2025: Navigating Chaos, Building Resilience. Retrieved from