The sports market is starting to charge! Is Polymarket rushing to issue tokens to generate revenue data?

Author: Frank, PANews

On February 18, 2026, Polymarket announced that starting that day, the platform would pilot a fee on market orders in its sports markets. The initial coverage includes NCAA college basketball and Serie A leagues, with plans to gradually expand to all sports events in the future.

Previously, Polymarket’s revenue was solely from a 15-minute volatility market fee in cryptocurrency, but its recent weekly income has already exceeded $1.08 million. According to on-chain data, sports markets account for nearly 40% of the platform’s total trading activity. If annualized, just the crypto markets’ fees could generate approximately $56 million in revenue per year. As the larger sports markets begin to charge fees, Polymarket may become the biggest money-printing machine in the crypto space.

PANews conducted an in-depth analysis of Polymarket’s fee mechanism, revenue model, competitive landscape, and token airdrop expectations.

From “zero revenue” to weekly millions, the $9 billion giant is eager to start earning

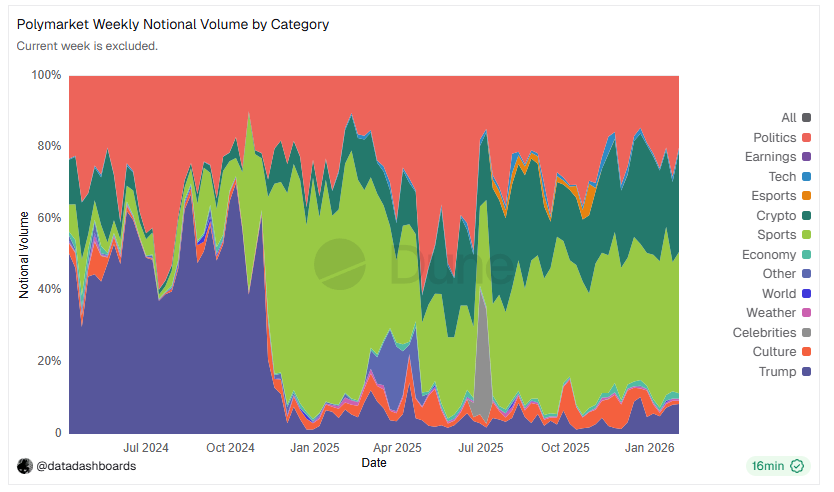

For a long time, Polymarket operated with almost “zero income,” with most markets not charging any transaction fees. This free model fueled remarkable growth: in 2025, total trading volume reached $21.5 billion, nearly half of the global prediction market’s total (which was $44 billion); in January 2026 alone, monthly trading volume hit a record-breaking $12 billion.

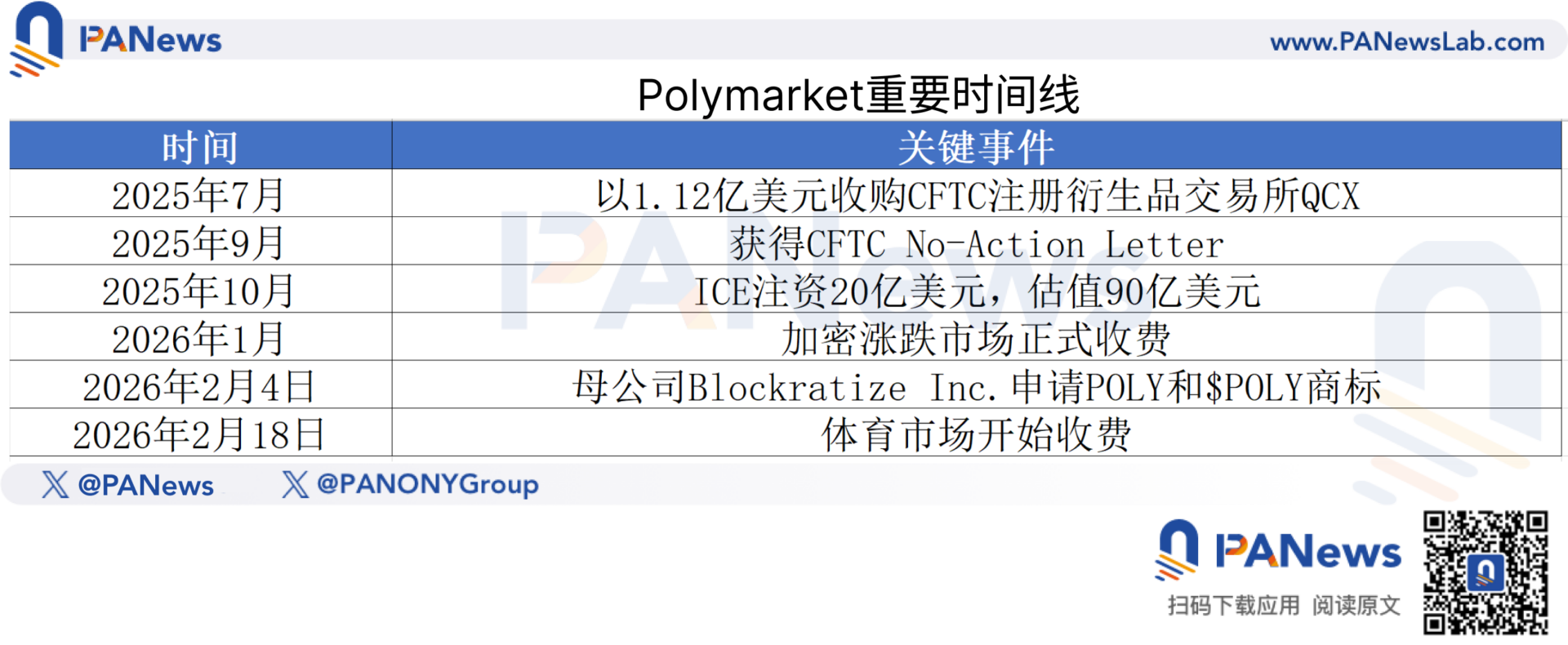

However, as the upcoming token listing approaches, the zero-revenue model clearly no longer matches its valuation. In its latest funding round, the valuation reached $9 billion. In October 2025, Intercontinental Exchange (ICE), the parent company of the NYSE, invested up to $2 billion in Polymarket. According to PM Insights, as of January 19, 2026, Polymarket’s secondary market implied valuation had risen to $11.6 billion, a nearly 29% increase from the previous funding round. There are reports that future funding rounds could value the platform between $12 billion and $15 billion. Such a high valuation requires corresponding revenue to support it.

The turning point came in January 2026, when Polymarket clearly felt the urgency to monetize.

In January, Polymarket officially introduced a “Taker Fee” (market order fee) for its high-frequency trading product, the 15-minute crypto volatility markets, with rates up to 3%. The results were immediate: by early February 2026, weekly fee income surpassed $1.08 million, with one week in January seeing $787,000 from just the 15-minute markets alone—accounting for 28.4% of the platform’s total prediction market fee income (which was $2.7 million) during that period. To date, Polymarket has generated over $4.7 million in fees, ranking among the top revenue-generating platforms.

A sophisticated fee model behind 0.45%—more than just profit

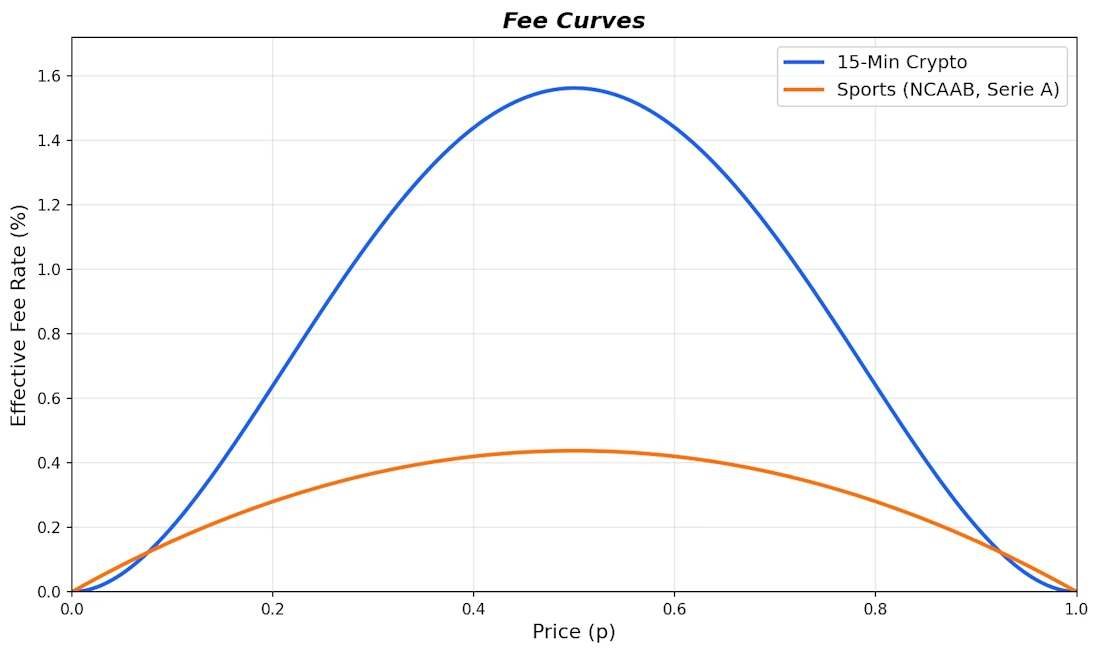

The fee introduced in the sports markets is part of a carefully designed dynamic fee model.

According to official Polymarket documents and community analysis, fees are only charged on market orders (Takers), while limit orders ( Makers) are free and even earn a 25% rebate on Taker fees. Similar to crypto fee structures, the rate is not fixed but fluctuates with the probability of the event:

In simple terms, the less certain the market, the higher the fee. When the probability is around 50%, the fee peaks at 0.44%. When the probability is at 10% or 90%, the fee drops to only 0.13%-0.16%.

Compared to crypto markets, the fee standard for sports markets remains much lower. However, this does not diminish the revenue potential of sports markets.

Data shows that sports markets currently account for 39% of Polymarket’s total trading activity, surpassing political markets (20%) and crypto markets (28%). More importantly, previous PANews analysis indicated that the average trading volume of short-term sports markets (around $1.32 million) is 30 times that of short-term crypto markets (around $44,000). This suggests that if sports markets are fully opened to fees, revenue could see enormous growth.

Take the 2026 Super Bowl as an example: Polymarket’s total trading volume in Super Bowl-related markets reached about $795 million, covering multiple sub-markets such as game outcome, player performance, and halftime show predictions. Weekly prediction market trading volume has once surged past $6.3 billion driven by sporting events.

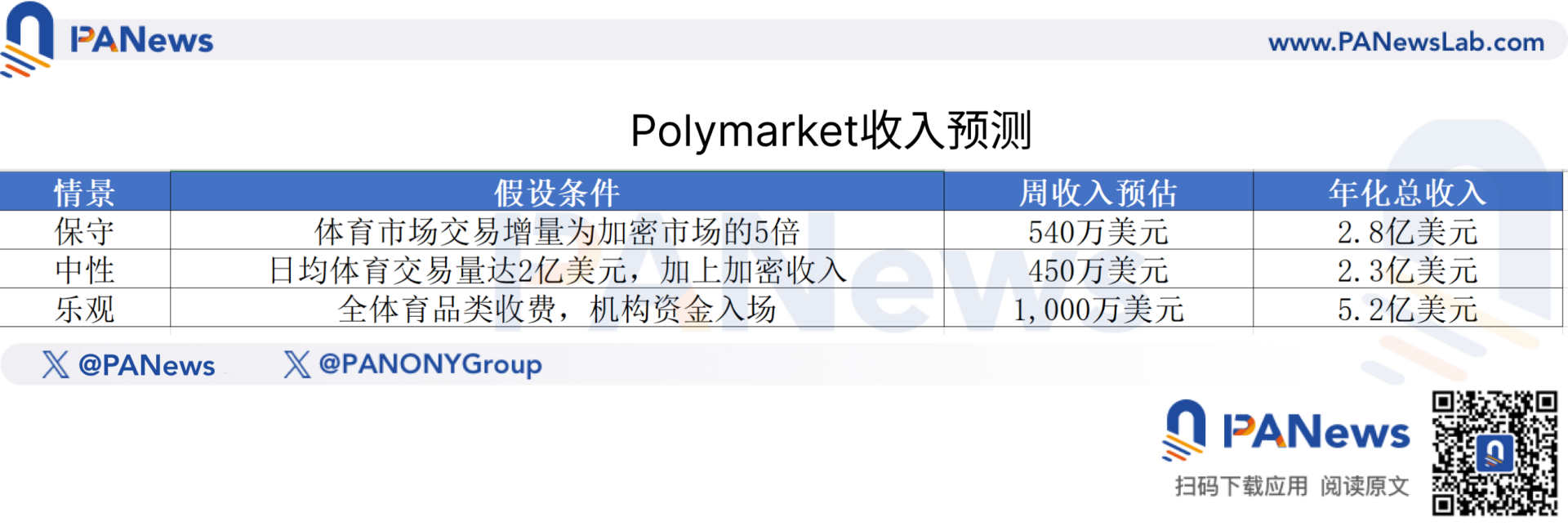

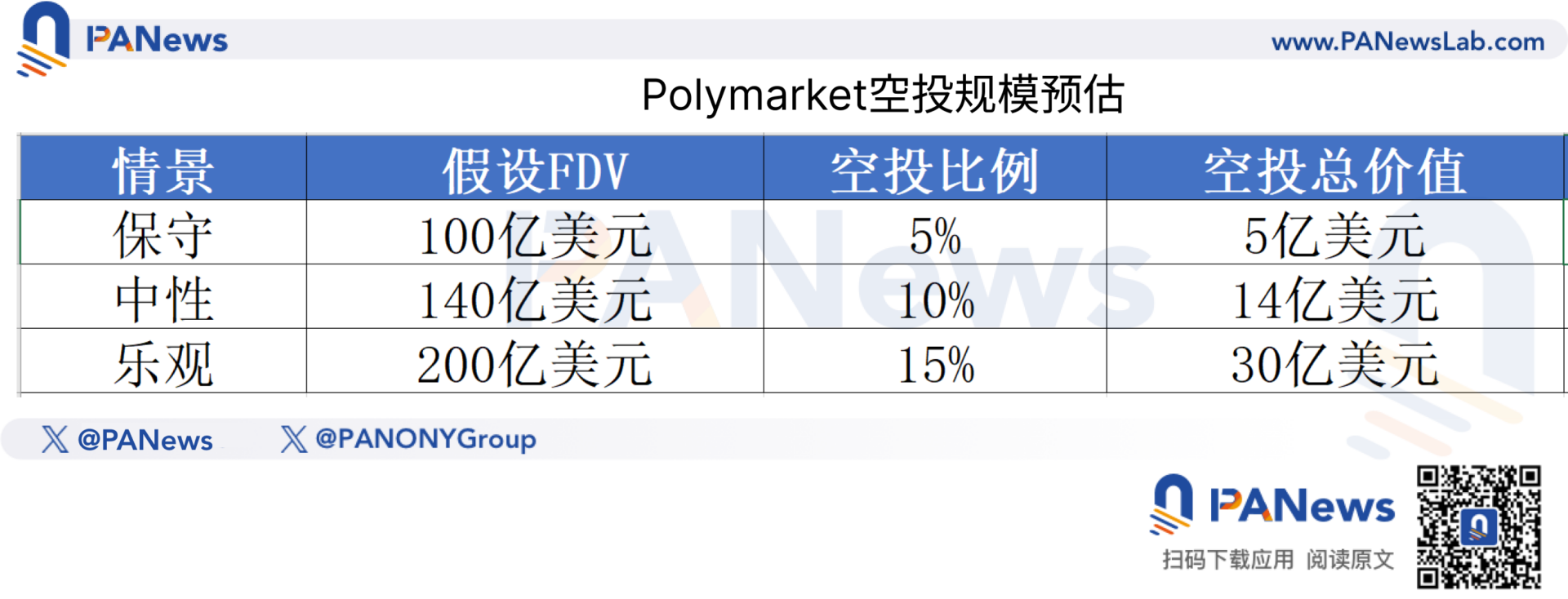

Based on current data, PANews constructed three profit forecast scenarios (assuming an average effective fee rate of 0.25% for sports markets, considering probability distributions and free limit orders):

Even with the most conservative estimates, full fee implementation could generate annual revenue exceeding $200 million, enough to place Polymarket among the highest-earning protocols in the Web3 space.

While surpassing Tether’s bond interest income or Ethereum’s gas fees may be unrealistic, Polymarket has the potential to become the “most profitable dApp” at the application layer. Especially considering its user retention rate of 85%, far above typical DeFi protocols, this high stickiness indicates higher quality revenue.

POLY Token and Airdrops—A multi-hundred-million-dollar “Wealth Feast”?

Polymarket’s high valuation and large user base make its token airdrop one of the most anticipated events of 2026.

Polymarket’s Chief Marketing Officer Matthew Modabber has explicitly stated, “There will be tokens, there will be airdrops.” Market predictions suggest a 62%-70% chance that Polymarket will issue tokens before December 31, 2026. Given the progress of its US operations, the token generation event (TGE) is likely to occur mid-2026.

On February 4, 2026, its parent company Blockratize Inc. applied for trademarks for “POLY” and “$POLY,” which is seen as a key milestone for the TGE. Based on industry norms, trademark registration typically takes 3-6 months from filing to TGE.

Airdrop scale surpassing Hyperliquid—The era of hype and volume inflation is over

Referring to recent airdrop ratios of top projects (Arbitrum, Jupiter, Hyperliquid), community allocations usually account for 5%-15% of the total supply. PANews estimated based on different valuation assumptions:

If the total airdrop amount is $1.4 billion, and approximately 500,000 active addresses qualify, the average airdrop per account could reach about $2,800. However, following the “80/20 rule,” top users might receive tens or even hundreds of thousands of dollars, while ordinary retail users should manage expectations reasonably.

It’s worth noting that Polymarket, alongside fee implementation, has introduced a 4% annualized holding reward, distributed via hourly snapshots and daily payouts. This mechanism reveals the project’s clear preference: capital retention is far more important than trading frequency.

Moat and Risks: Where does this “money printer” face danger?

Charging fees means users incur additional costs—so what gives Polymarket the ability to keep fees?

Three clear moats are evident: first, the platform possesses unmatched liquidity depth in prediction markets, crucial for large trades; second, compared to traditional betting (5%-10% rake) and Kalshi’s 1%-3.5%, the peak fee of 0.45% still offers a significant cost advantage; third, ICE’s involvement not only brings capital but also data distribution capabilities—ICE plans to integrate Polymarket’s real-time prediction data into global institutional clients, creating a “second growth curve” beyond transaction fees.

However, risks cannot be ignored:

Short-term trading volume fluctuations: Polymarket’s monthly volume once peaked at $10.26 billion in November 2025 but fell to $5.43 billion in December. Will fees exacerbate this trend? Yet, considering the positive effects of introducing Maker rebates—such as increased order book depth and narrower spreads—long-term trading volume may actually rise.

Competitive landscape: Kalshi has an early-mover advantage in the compliant US market (2025 revenue around $260 million), Hyperliquid is attempting to enter the prediction space via “Outcome Trading” (FDV about $16 billion), and Predict.fun is attracting users with DeFi yield stacking.

Regulatory uncertainty: Despite obtaining a CFTC No-Action Letter and acquiring a compliant exchange (QCX), the evolving US regulatory environment remains a looming threat over prediction markets.

Postscript

From free to paid, from crypto volatility markets to global sports events, Polymarket is executing a carefully planned business model upgrade. Just within crypto markets, weekly income can reach millions, and in the massive sports markets—accounting for nearly 40% of platform volume and with liquidity 30 times that of crypto—the fee rollout has only just begun.

Polymarket’s story offers a thought-provoking model: a platform’s true value may not lie in how much it’s earning now, but in its ability to demonstrate “the confidence to charge whenever it wants.” When the cake is big enough and the moat deep enough, opening the fee gate is only a matter of time.

And this “money printer” that’s heating up, February 18 was just the start button.