The Granularity Revolution in Digital Asset Taxation: Analysis and Compliance Guide for U.S. 1099-DA Form

Author: FinTax

1 Introduction

As crypto assets move from the fringe to the mainstream, the global “tax enforcement net” is rapidly tightening. Following the official release of the 2025 Digital Asset Broker Information Reporting Form (Form 1099-DA,简称1099-DA) and its accompanying guidance, the IRS has recently updated two detailed rules. These updates not only clarify the mandatory reporting obligations for digital asset brokers but also refine the de minimis exemption thresholds through supplementary rules. Additionally, they introduce an innovative optional reporting method for stablecoins and specified NFTs. This shift is more than just a form update; it reflects a regulatory granularity that penetrates down to individual tokens. While ensuring tax transparency, regulators are reducing compliance costs for market participants through differentiated rules. This article dissects the recent updates to Form 1099-DA, analyzes the IRS’s current regulatory direction and core implications, and offers compliance insights.

2 Tracing the Roots: Content and Background of Form 1099-DA

2.1 Overview

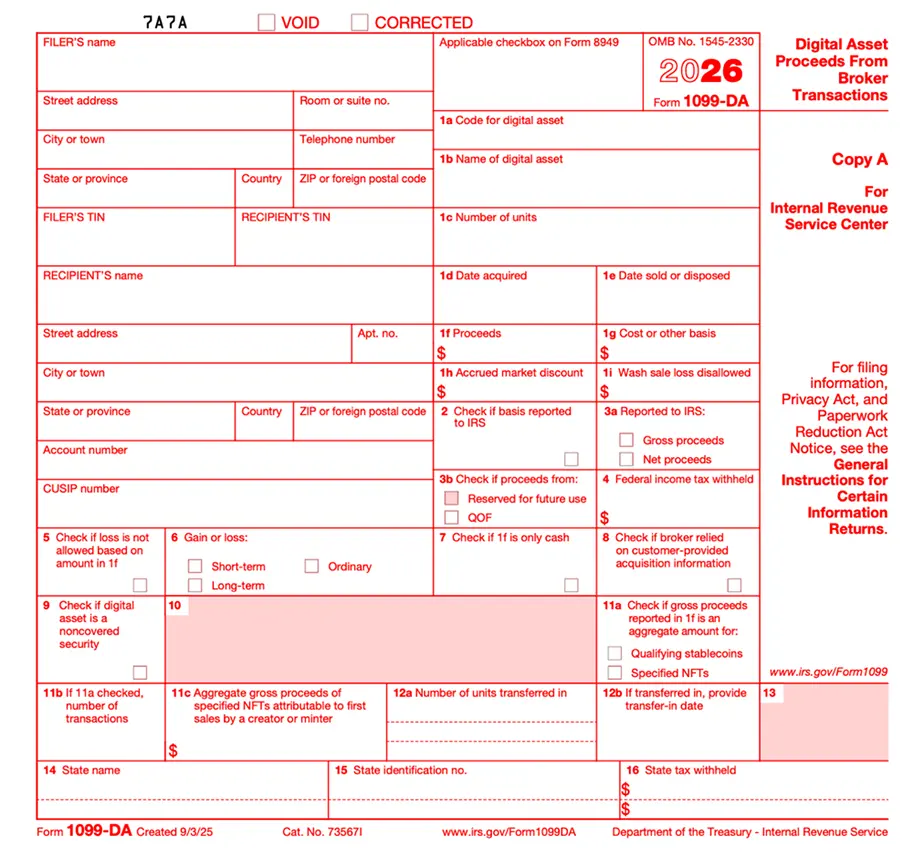

Form 1099-DA is a reporting form used by digital asset brokers to report gains and losses from digital asset transactions to the IRS and clients. It is not merely a patch on existing systems but a dedicated reporting form designed specifically for the native attributes of digital assets.

According to the latest instructions for Form 1099-DA (Instructions for Form 1099-DA (2025)), starting January 1, 2025, brokers must record and report the gross proceeds of each sale transaction. Notably, the IRS will not require the reporting of cost basis and gain/loss details in 2025; instead, it grants a voluntary reporting grace period, explicitly stating that no penalties will be imposed for reporting errors during this period. The mandatory reporting of cost basis and gain/loss will be deferred until 2026 (for “covered digital assets” acquired after January 1, 2026), providing a one-year transitional period for brokers to address issues such as chain-of-title verification and cost tracing.

Furthermore, the latest guidance emphasizes more granular data reporting requirements, focusing on two dimensions: asset identity “uniqueness” and transaction “structure.” Asset identification is enhanced through the introduction of the Digital Token Identifier Foundation (DTIF) codes to eliminate ambiguity in token naming. Transaction structuring involves isolating specific asset flows to distinguish primary sales (original minting proceeds) from secondary market transfers, achieved via new Box 11c, which separates the original minting income of specified NFTs from secondary transfer gains, resulting in more detailed reporting data for the IRS.

- Digital Assets: Under 1099-DA, digital assets refer to any value expressed in digital form recorded on cryptographically secured distributed ledgers (such as blockchains or similar technologies), regardless of whether each transaction is individually recorded on the ledger; they do not include cash (such as USD or other fiat currencies issued by governments or central banks). The IRS’s definition is broad, covering any digital representation of value recorded on cryptographically protected distributed ledgers, including cryptocurrencies, tokenized securities, and specified NFTs.

- Qualifying Stablecoins: Digital assets meeting all three criteria are considered qualifying stablecoins:

(1) Designed to track a single fiat currency issued by the government or central bank (including USD) on a 1:1 basis;

(2) Employ effective stabilization mechanisms;

(3) Widely accepted as a means of payment outside the issuer.

Reporting entities mainly include brokers and digital asset intermediaries.

- Broker: As revised under the regulations implementing Section 6045 of the Internal Revenue Code, a broker is any person regularly engaged in the business of executing digital asset sales for others. Specifically, a person is considered a broker if:

(1) They regularly suggest clients redeem digital assets they have created or issued; or

(2) They act as an agent, dealer, or intermediary executing client dispositions of digital assets.

-

Digital Asset Middleman: A person providing facilitation services for digital asset sales who can identify the seller and the nature of the transaction.

-

Such middlemen include:*

(1) Entities accepting or processing digital assets as payment for stocks, commodities, regulated futures contracts, securities futures, forward contracts, foreign currency contracts, debt instruments, options, or securities futures;

(2) Real estate reporting agents who know or should know that the buyer uses digital assets for payment;

(3) Entities accepting digital assets as compensation for brokerage services;

(4) Owners or operators of one or more digital asset vending machines; or

(5) Digital Asset Payment Processors (PDAP).

- Exclusions:*

(1) Entities solely engaged in proof-of-work (PoW) or proof-of-stake (PoS) distributed ledger validation services (staking/mining) without additional functions; or

(2) Entities providing hardware or software (via sale, licensing, or other means) that allow users to control private keys to access digital assets on distributed ledgers (e.g., non-custodial wallets), without other services.

In summary, digital asset middlemen include not only traditional centralized exchanges (CEXs) but also custodial wallet providers, payment processors (PDAP), and operators of digital asset vending machines (kiosks).

To better understand the uniqueness of 1099-DA, the following table compares it with traditional financial and payment reporting forms.

2.2 Core Content

The structure of 1099-DA mirrors that of the traditional 1099-B for securities but adds several detailed fields tailored for crypto features:

- Box 1a & 1b (Digital Asset Code and Name): Mandatory inclusion of DTIF codes; if a token lacks a DTIF code, “999999999” (alphanumeric identifier) must be used. For the optional aggregate reporting method for specified NFTs, Box 1a also requires “999999999,” and Box 1b should specify “Specified NFTs.” For qualifying stablecoins using the optional method, Box 1a records the stablecoin’s DTIF identifier, and Box 1b records the stablecoin name.

- Box 1f (Gross Proceeds): Can include cash, fair value of services, digital assets, or other property received.

- Box 1g (Cost Basis): Voluntary in 2025 but will become central for profit/loss calculation in the future.

- Box 11a & 11b (Aggregate Reporting Flags): Special fields for stablecoins and specified NFTs, indicating whether the optional reporting method was used and the number of transactions covered.

- Box 11c (Primary Market Sales): Specifically captures the original minting proceeds of specified NFTs, differentiating from secondary transfers.

2.3 Background of Form 1099-DA

2.3.1 Domestic (U.S.)

In August 2021, the Infrastructure Investment and Jobs Act (IIJA) was passed by the Senate and signed into law in November of the same year. It amended Section 6045 of the Internal Revenue Code to explicitly include “digital assets” within the scope of “broker” reporting, aiming to improve tax transparency through a third-party automatic reporting system.

After two years of expert consultations and public policy discussions, on July 9, 2024, the U.S. Treasury and IRS issued Treasury Decision 10000 (TD 10000), titled “Gross Proceeds and Basis Reporting by Brokers and Determination of Amount Realized and Basis for Digital Asset Transactions.” Effective September 9, 2024, TD 10000 precisely defines broker criteria, specifies reportable transaction types, and details cost basis calculation methods.

TD 10000 states that 1099-DA will be implemented starting in 2026, with each field supported by legal provisions from TD 10000, requiring brokers to report digital asset gains and cost basis information from January 1, 2025.

2.3.2 International (Overseas)

The 1099-DA’s issuance is not only a unilateral domestic regulatory upgrade but also aligns with the global trend toward tax transparency. At the end of 2022, OECD released the Crypto-Asset Reporting Framework (CARF), aiming to establish a global standard for automatic exchange of crypto tax information. On November 10, 2023, the U.S. and over 40 countries issued a joint statement committing to accelerate CARF implementation. On July 30, 2025, the U.S. proposed a “Digital Asset Disclosure” to implement CARF. On November 14, 2025, the IRS submitted a proposal titled “US Broker Digital Transaction Reporting” to the White House, seeking to adopt CARF. The White House is currently reviewing this proposal. If implemented, CARF would enable the IRS to access key information on overseas crypto accounts of U.S. taxpayers and conduct tax enforcement accordingly.

Although the U.S. has not yet signed a multilateral CARF agreement or initiated automatic exchange of crypto tax data with other jurisdictions, the formal rollout of 1099-DA marks a pioneering step in establishing a mature underlying data collection system, laying the technical foundation for future international tax data exchanges.

3 Riding the Wave: Recent Policy Interpretations of U.S. 1099-DA

Recently, the IRS has accelerated its regulation of crypto assets. Its new detailed rules show that policy implementation is shifting from broad compliance requirements to specific, actionable standards that balance enforcement and efficiency.

3.1 De Minimis Exemptions and Aggregate Reporting Rules

While maintaining strict oversight, the IRS introduces flexibility through de minimis rules and optional reporting methods, creating a layered “relief” system to reduce regulatory burden.

The process is as follows: brokers first determine whether a transaction qualifies for the “optional reporting method” based on asset type. If they choose this method, the IRS assigns a de minimis threshold; transactions below this threshold are exempt from detailed reporting, while those exceeding it must comply with the reporting rules.

The optional reporting method determines “how to report”: for stablecoins with minimal value fluctuation (Qualifying Stablecoins) and specified NFTs with consumer use, brokers can opt for simplified or aggregate reporting instead of detailed transaction-by-transaction reporting.

The de minimis rules determine “whether to report”: to prevent overwhelming the system with small retail transactions (e.g., buying coffee or small daily payments with crypto), the IRS sets different thresholds:

- Digital Asset Payment Processor (PDAP) sales threshold: $600

If a PDAP processes total payments or transactions for a client not exceeding $600 in a year, no 1099-DA is required.

- Qualifying Stablecoins optional reporting threshold: $10,000

For stablecoins using the optional method, if the client’s total annual sales (net of transaction costs) do not exceed $10,000, reporting can be waived.

- Specified NFTs optional reporting threshold: $600

For NFTs, if the client’s total annual sales (net of transaction costs) do not exceed $600, reporting can be waived.

3.2 Exclusion of Joint Filing Plans

Another recent development is that the IRS explicitly states that 2025 1099-DA reports will not participate in the “Federal/State Combined Filing” (CF/SF) program. This means brokers cannot submit a unified state and federal report via a single system and may need to file separately with local tax authorities according to each jurisdiction’s rules.

4 Conclusion

Faced with the multiple challenges posed by 1099-DA, high-net-worth investors, project teams, and Web3 institutions must adapt to the new reporting landscape. For Web3 practitioners, transaction data governance is not only about complying with IRS reporting and audits but also about building a clear financial picture. In the wave of increased transparency, those who can quickly upgrade from “chaotic bookkeeping” to “tax compliance” will be better positioned to succeed in the increasingly competitive global Web3 environment.