We use large models to "divine" the tokenization/Web3 landscape of 2026.

Author: Frank, MaiTong MSX Researcher

With the same data, do you believe in human interpretation or AI “divination”?

It sounds like a cyberpunk joke, but in today’s world of abundant opinions and high emotionality, what the market truly lacks are those unembellished, real sample signals that haven’t yet been sanitized.

After all, positions really do lie.

At year’s end and beginning, to get as close as possible to the truth of tokenization / Web3 at the turning point of 2025-2026, we conducted an anonymous sampling of frontline builders via MaiTong MSX, focusing on three main questions:

- Keywords in your view of 2025 US stocks / tokenization;

- Your actual holdings in 2025 (not limited to US stocks / Web3);

- The directions you are most willing to allocate to in 2026 (not limited to US stocks / Web3);

Under some “coercion and inducement,” we gathered a reasonably satisfactory sample size, which was then compressed into three word clouds with minimal subjective judgment. Considering that human interpretation inevitably involves bias, we decided to invite “pure” AI models—ChatGPT, Gemini, and DeepSeek—to “divine” these three word clouds under completely consistent prompts.

Perhaps, AI might actually understand this generation of builders better than we do, and through these fragments, piece together the fate puzzle of the US stock market, Web3, and tokenization in 2026.

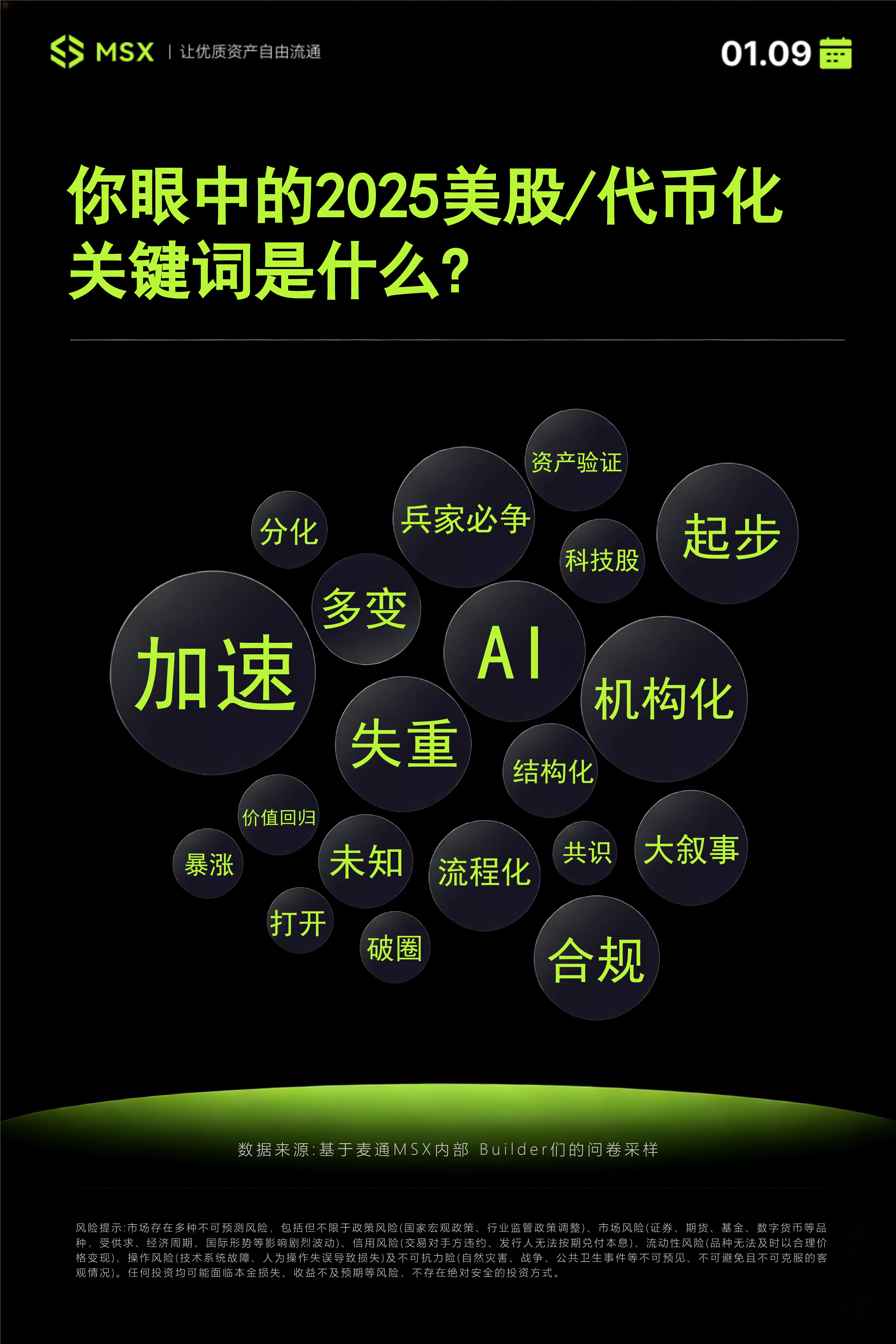

1. What are the keywords in your view of 2025 US stocks / tokenization?

Prompt: You will see a set of keywords sampled from frontline practitioners in US stock tokenization / Web3, answering the same question: “What does the 2025 US stock / tokenization landscape look like in your view?” Do not judge correctness, nor introduce external market info. Only interpret these keywords based on their data structure and language features, focusing on:

- Which keywords have the highest / lowest / most abrupt frequency? What structural states might they reflect?

- Are there keywords or semantic directions showing clear consensus? Are there near-synonyms, opposing terms, or tension-filled combinations?

- What overall stage characteristics do these keywords suggest for the sector?

- If only based on these keywords, without external info, how would you interpret the 2025 and 2026 in this sector?

Maintain a descriptive, restrained tone—avoid investment advice or definitive judgments. Limit your reply to 1000 words.

Note: Responses are lightly edited for readability but retain the original intent and reasoning.

ChatGPT: The most frequent keywords cluster around “acceleration” and “institutionalization,” indicating the sector is experiencing a significant pace change but has not yet stabilized; mid-frequency keywords include “AI,” “compliance,” “differentiation,” reflecting a background normalization; low-frequency or isolated words like “weightlessness,” “unknown,” “battlefield,” “initiation,” carry strong subjective or emotional metaphors, possibly mirroring individual discomfort with structural shifts, competition, or uncertainty.

Overall, the corpus exhibits language features characteristic of a “preliminary—structural building” phase, with high-frequency verbs outnumbering nouns, emphasizing process and change rather than stable forms; multiple keywords point to rules, verification, and procedures rather than specific products or models; emotional words exist but are not dominant, indicating perceived uncertainty but not yet out of control.

Based solely on these keywords, one could interpret 2025 as a transitional year marked by acceleration but not yet formation, with consensus emerging amid divergence.

Gemini: High-frequency words include “accelerate,” “institutionalize,” indicating strong consensus on growth driven by professional participation; mid-frequency terms like “AI,” “compliance,” “differentiation” sketch a landscape of technological methods, regulatory frameworks, and uneven market performance; abrupt low-frequency words such as “weightless,” “process,” “asset verification” reflect underlying anxieties beneath apparent prosperity, shifting from narrative to implementation perspectives.

The overall data shows a “high-energy, low-center” state, where “institutionalization” and “compliance” coexist—this acceleration is not reckless expansion but constrained by rules, forming a deterministic tone for the industry.

From the overall features, this sector appears to be in a “transitional explosive period,” combining the chaos of early stages (weightless, unknown) with the rigor of pre-maturity (compliance, process). The market is no longer monolithic but shows clear “differentiation,” indicating tokenization is no longer an isolated asset experiment but increasingly integrated with mainstream finance and cutting-edge tech.

In summary, from 2025 to 2026, this is a period of frantic pursuit amid rule reshaping, heavily reliant on technological validation, and marked by professional entry.

DeepSeek: “Acceleration” dominates absolutely, with “institutionalization,” “differentiation,” “compliance,” and “AI” forming the second tier; most words appear only once, showing a dispersed long tail—e.g., “weightless” appears somewhat abruptly amid generally dynamic, positive contexts (like acceleration, opening, breaking barriers), possibly metaphorical of losing traditional reference points amid rapid change.

“Institutionalization” and “compliance” are tightly linked, both pointing to deep involvement of traditional financial systems; “differentiation” hints at internal stratification or divergence within the sector.

The sector’s dynamic (accelerating, volatile, oscillating) and institutionalization (institutional, compliant, structured) form two dominant semantic directions, paralleling a field seeking rules and structure amid rapid change.

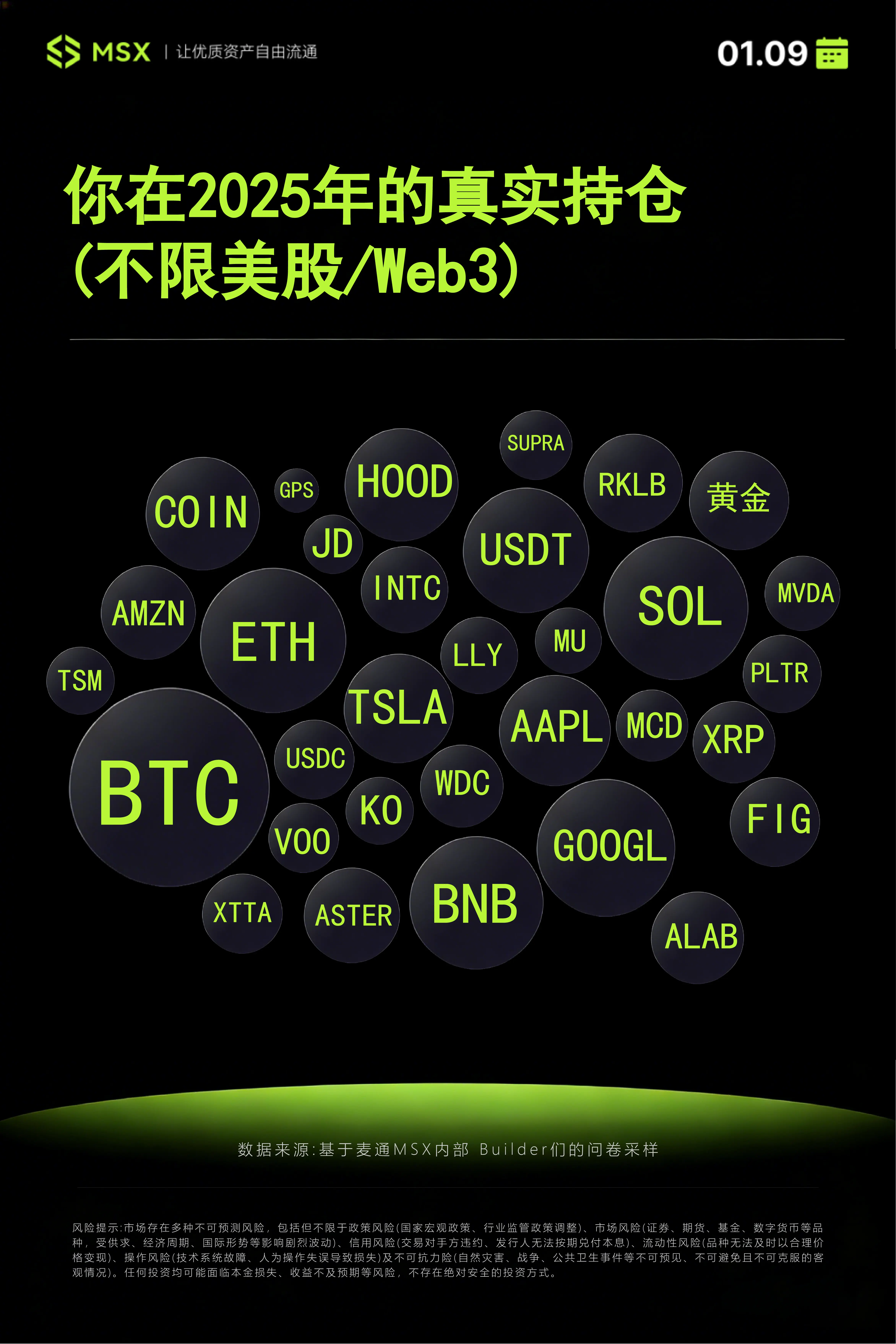

2. What are your actual holdings in 2025 (not limited to US stocks / Web3)?

Prompt: You will see a set of keywords sampled from frontline practitioners in US stock tokenization / Web3, answering: “Your actual holdings in 2025.” Do not judge correctness or external info; only analyze the composition:

- Classify the assets / sectors involved;

- Are there core assets repeatedly allocated?

- Is the overall portfolio more concentrated or diversified? What risk appetite does it suggest?

- Can you observe behavioral traits from these holdings?

Maintain a descriptive, restrained tone—limit to 1000 words.

ChatGPT: Structurally, the holdings can be clearly grouped into several asset clusters:

- Native crypto assets: high-frequency mentions of BTC, ETH, SOL, BNB, USDT, USDC; secondary or peripheral mentions include XRP, DOGE, ASTER, SUPRA, XTTA. This category dominates in quantity and repetition, including both mainstream and exploratory allocations.

- US tech and financial stocks: including giants like GOOGL, AAPL, AMZN, NVDA, TSLA, PLTR, INTC, TSM, MU, WDC; and financial/trading platforms like COIN, HOOD. Reflects a preference for infrastructure, platforms, and tech capabilities.

- Consumer and traditional defensive stocks: MCD, KO, LLY, JD, fewer in number but serving as hedges or stabilizers.

- Indices and cash-like assets: VOO, gold, USDT, USDC—providing liquidity and volatility buffers.

Repetition frequency reveals clear core assets:

- BTC is the most frequently mentioned single asset, with dense multiple mentions.

- GOOGL dominates among US stocks, with high recurrence.

- ETH, SOL, BNB form a secondary layer of crypto assets.

- USDT appears multiple times, indicating a non-trivial role for stablecoins.

This suggests respondents favor a “few high-confidence core assets” approach, stacking on key holdings while maintaining diversification around them.

Interpreted solely from these keywords, the portfolio resembles a structure anchored on a small set of core assets, with parallel allocations across multiple asset classes, and a significant portion of liquidity and exploration space.

Gemini: Initial analysis indicates these holdings can be categorized into five major groups:

The data shows a strong consensus core: BTC is mentioned over half the time, the only asset with universal agreement; TSLA and RKLB/space stocks follow, indicating an increased focus on hardcore tech and space exploration compared to 2025, suggesting a shift from purely digital to physical frontier investments.

The structure resembles a “dumbbell”: one extreme is highly concentrated BTC, the other is a highly dispersed set of tech-related assets (space, semiconductors, storage).

Risk appetite appears to be “extreme—both aggressive and defensive,” with high-volatility assets like MEME tokens, RKLB, and high-correlation hedges like SQQQ, gold, silver, copper, oil. This indicates expectations of not just steady growth but significant volatility, with a strategic balance between growth and risk management.

Overall, the increased presence of commodities (gold, silver, copper, oil) and storage/space assets reflects a shift from purely digital (Web3) focus toward tangible assets and fundamental resources.

Industry deep-diving is evident: respondents are not just holding top chip stocks like NVDA but also extending into storage hardware (MU, WDC, SNDK), showing a professional, industry-based deep understanding.

If 2025 is about “building roads” (compliance, infrastructure), then 2026 is about “expeditions” (space, hardware, global resources).

DeepSeek: Keyword frequency shows BTC at the top, accounting for 20.4% of mentions, with TSLA (9.3%) close behind; together, they comprise about 30%, indicating a concentrated top preference. NVDA, RKLB, GOOGL, HOOD, stablecoins, and precious metals are also mentioned multiple times but remain dispersed across many assets and themes, forming a “core-periphery” structure—core highly concentrated, periphery broadly spread.

Crypto (especially BTC) and tech stocks (TSLA, NVDA) dominate, with thematic sectors like space (RKLB), chips, storage, and safe-haven assets like precious metals and stablecoins also prominent.

Notably, stablecoins, precious metals, oil, and SQQQ allocations are more prominent than in 2025, indicating a defensive stance against macroeconomic uncertainty or market downturns.

Compared to 2025, BTC’s consensus strength further solidifies its core position; meanwhile, GOOGL, ETH, SOL’s prominence diminishes, while TSLA and NVDA gain, reflecting a shift from diversified crypto and large tech to more focused, leading assets.

Sector-wise, allocations expand into thematic sectors (space, chips, storage) and commodities, with a broader consensus across multiple assets.

Overall, the data shows a transition from broad crypto and tech stock holdings in 2025 to a more concentrated core of Bitcoin, with increased focus on specific tech leaders and thematic investments, balancing growth and risk mitigation amid uncertainty.

3. Which directions are you most willing to allocate to in 2026 (not limited to US stocks / Web3)?

Prompt: You will see a set of keywords sampled from frontline practitioners in US stock tokenization / Web3, answering: “Your preferred directions for 2026.” Do not judge correctness or external info; interpret based on data structure:

- Classify involved assets/sectors;

- Which sectors/assets are favored? Are there core assets repeatedly allocated?

- Is the overall portfolio more concentrated or diversified? What risk approach does it suggest?

- Any observable behavioral traits?

- What are the assets/sectors with highest consensus in 2025 vs. 2026? How do they change?

Maintain a descriptive, restrained tone—limit to 1000 words.

ChatGPT: Compared to 2025, 2026’s keywords show a clear shift: specific assets and abstract sectors are now juxtaposed, indicating respondents emphasize directionality and structural judgment rather than single assets.

The sample roughly falls into these categories:

- Crypto native assets: BTC, ETH, SOL are high-frequency, with stablecoins and meme coins still central but with clearer stratification.

- US tech and high-tech sectors: stocks like TSLA, GOOGL, NVDA, AMZN, PLTR, HOOD; sectors like tech, semiconductors, aerospace—transitioning from stock picking to industry-oriented views.

- Commodities and physical assets: Gold, silver, copper, oil—more prominent in 2026, reflecting macro considerations.

- Indices and hedging tools: S&P 500, SQQQ—indicating macro market concern.

Core assets in 2026 are highly concentrated: BTC remains the most mentioned, far surpassing others; TSLA and NVDA are also repeatedly cited, more so than in 2025.

This suggests a strategic focus on a few highly consensus assets and sectors, with thematic and resource-based investments, aiming for a structured approach amid uncertainty.

Gemini: The 2026 sample shows a broader span, summarized into four categories:

BTC is mentioned over half the time, the only asset with universal consensus; TSLA and RKLB/space stocks follow, indicating a notable increase in physical frontier investments, extending from digital to space exploration.

The holdings resemble a “dumbbell”: one pole is a highly concentrated BTC, the other a dispersed set of tech and space assets (semiconductors, storage, aerospace).

Risk appetite is “extreme—both aggressive and defensive,” with allocations to high-volatility assets like MEME tokens, RKLB, and hedges like SQQQ, gold, silver, copper, oil. This indicates expectations of significant volatility, balancing growth with risk management.

Overall, the increased presence of commodities and space assets reflects a shift from purely digital Web3 focus toward tangible assets and fundamental resources.

Industry deep-diving is evident: respondents are not just holding top chip stocks but also extending into storage hardware (MU, WDC, SNDK), showing professional industry-level understanding.

If 2025 is about “building roads” (regulation, infrastructure), then 2026 is about “expeditions” (space, hardware, global resources).

DeepSeek: BTC leads with 20.4% mention rate, TSLA at 9.3%, together about 30%, indicating a highly concentrated top preference. NVDA, RKLB, GOOGL, HOOD, stablecoins, and precious metals are also frequently mentioned but dispersed, forming a “core-periphery” structure—core assets highly concentrated, periphery more diversified.

Crypto (especially BTC) and tech stocks (TSLA, NVDA) dominate, with thematic sectors like space, chips, storage, and safe assets like metals and stablecoins also prominent.

Compared to 2025, allocations to stablecoins, precious metals, oil, and SQQQ are more prominent, indicating a defensive macro stance.

The consensus on core assets shifts: BTC remains dominant, while GOOGL, ETH, SOL’s prominence diminishes; TSLA and NVDA’s prominence increases, reflecting a move toward specific leading assets.

Sector-wise, the focus broadens into thematic sectors and commodities, with a more diversified asset set.

In sum, the evolution from 2025 to 2026 shows a move from broad crypto and tech stock holdings toward a core of Bitcoin, with increased emphasis on specific tech leaders, thematic investments, and risk hedging—balancing growth and protection amid macro uncertainties.