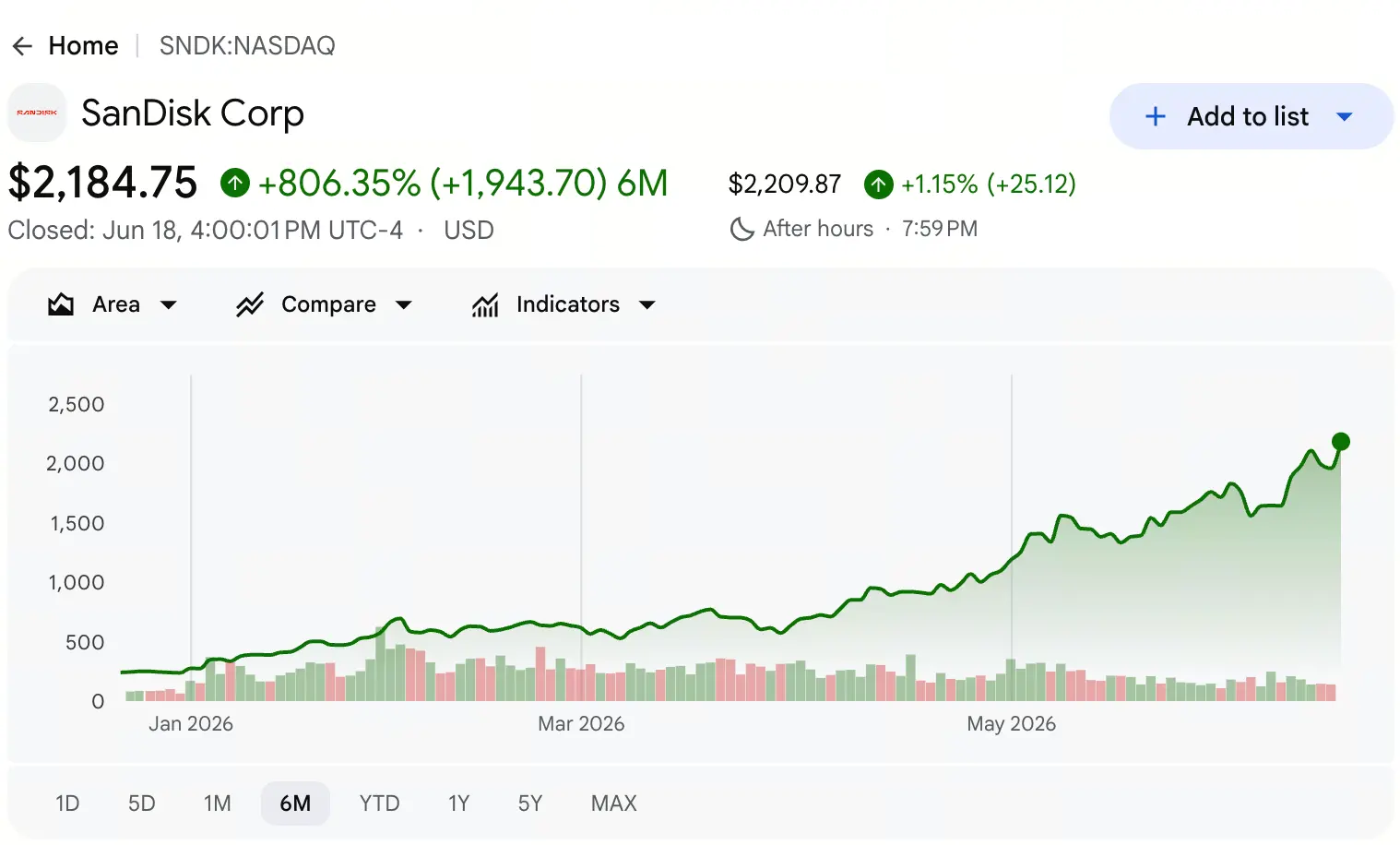

In June 2026, global capital markets’ spotlight continued to focus on the storage chip sector. According to Gate stock quote data, SanDisk (SNDK) closed last Friday at $2,183, up 11.3% during the trading session; the intraday high reached $2,191 again, setting a new all-time high.

What does this price mean? Take the timeline back to April 2025, when SanDisk’s stock price once fell to a low of $27.89. From $27.89 to $2,191, over a 14-month span, the cumulative gain exceeded 77 times. As of June 18, SanDisk’s total market cap has already surpassed $32 billion, with a dynamic P/E ratio of about 69x.

When a stock makes a price leap of this magnitude in such a short time, the market will inevitably ask the same question: where is SanDisk’s ceiling?

There is no simple answer. To answer it, you need to look through the surface of the stock price into the storage chip industry’s structural underlying drivers—from institutional benefits unleashed by asset carve-outs, to AI-driven supply-demand imbalances, and then to a fundamental change in financials and extreme divergence in market sentiment.

How did the independent split trigger a re-rating of SanDisk’s value?

SanDisk is not a startup. Its predecessor was a global flash memory technology pioneer founded in 1988, which was fully acquired by Western Digital in 2016 for about $19 billion. Over the following more than eight years, SanDisk existed as Western Digital’s flash business segment, and its value was buried in the financial statements of the integrated company. In 2022, Elliott Management publicly proposed separating the HDD and NAND flash businesses, arguing that the valuation logic for the two types of assets is fundamentally different, and that mixed operations led to both sides’ market values being undervalued.

On February 21, 2025, the split was officially completed. Western Digital distributed about 80.1% of SanDisk’s outstanding shares to shareholders in a 3:1 ratio, and SanDisk listed independently on Nasdaq under the ticker SNDK. Later that same year, in November, SanDisk was added to the S&P 500 index.

The core value-release mechanism of the split is that once the flash business is separated from the HDD business’ income statement structure, the market can value it using a pure NAND supplier’s pricing model, no longer dragged down by the discount applied to integrated enterprises. About one year after the split, SanDisk’s market value overtook Western Digital by more than $4 billion.

This structural shift forms the asset-pricing premise at the very bottom of this round of gains. SanDisk’s rally is not a zero-to-one entrepreneurial story; it is a process of value returning after years of mispricing of a mature asset, achieved through institutional restructuring.

Why does the AI era make “storage power” surpass “computing power”?

If the split is the valve that releases value, then the AI demand boom is the engine pushing prices sharply higher.

One key shift in the market’s understanding is that AI bottlenecks are moving from “computing power” to “storage power.” While market attention remains highly focused on compute chips like GPUs, a deeper industrial logic is taking shape—during the AI inference era, storage scarcity is beginning to outstrip computation.

On the demand side, AI servers’ need for storage capacity far exceeds that of traditional architectures. The amount of NAND flash used in a single AI server is more than 3 times that of a traditional server. More importantly, the demand mix has fundamentally changed: leading cloud providers such as Amazon, Microsoft, and Google have already locked in full-year storage capacity for 2027, and even started planning allocations for 2028 supply. Enterprise customers no longer adjust procurement schedules based on price fluctuations; instead, they prioritize locking in capacity to ensure compute delivery—fundamentally breaking the previous cycle of “price increases leading to expansion, and oversupply leading to falling prices.”

On the supply side, there are multiple hard constraints. Expanding NAND flash capacity requires massive capital expenditures and long construction cycles. A research report from Mizuho Securities shows that wafer starts are expected to shrink by 5% in 2026 and only grow by 3% in 2027. The report expects that before 2028 or 2029, the market will not have any significant new supply capacity coming online. On the demand side, enterprise SSDs have become the key driver of demand; overall NAND demand is expected to grow by 18% in 2026 to 2027, respectively.

The “scissor gap” formed by demand growth and supply contraction is the most solid fundamental support for SanDisk’s sustained rise. Goldman Sachs defined this rally as a “multi-year AI memory supercycle” and predicted that AI-driven shortages will last at least until 2028.

Can the fundamental change in financial data support the current price level?

The sustainability of price moves ultimately depends on a real improvement in fundamentals. SanDisk’s 2026 earnings data shows an extremely steep growth trajectory.

For fiscal year 2026, first quarter (as of October 2025), SanDisk’s revenue was $2.308 billion. In the second quarter (as of January 2026), revenue rose to $3.025 billion, up about 31% quarter-over-quarter. But the real inflection point appears in fiscal year 2026 third quarter (as of April 2026)—single-quarter revenue jumped to $5.95 billion, up 97% quarter-over-quarter and 251% year-over-year. GAAP net profit was $3.615 billion (diluted earnings per share of $23.03).

Even more值得 attention is the jump in gross margin. SanDisk’s gross margin rose from the 2023 fiscal year low of 7.1% to 50.9% in the second quarter of fiscal year 2026; in the third quarter it climbed further to 78.4%. A non-GAAP gross margin of 78.4% far exceeds the industry’s average level of 30% to 40%, making it one of the steepest climbs in semiconductor history.

The improvement in the balance sheet is also significant. Management repaid $1.35 billion of $2.0 billion split debt in just 10 months, flipping net debt from $419 million to net cash of $889 million. On a trailing 12-month basis, revenue growth was 83%, and free cash flow reached $4.5 billion.

The company’s revenue guidance for fiscal year 2026 fourth quarter is $7.75 billion to $8.25 billion, and its non-GAAP EPS guidance is $30 to $33. If this guidance is met, SanDisk’s full-year revenue will be close to or even exceed the market consensus of $19.42 billion.

The shift from “financial distress” to “cash cow” provides micro-level justification for SanDisk’s price re-rating.

What do the different rally magnitudes between focused NAND and all-around DRAM imply?

In the collective rise of storage chips, SanDisk’s gains have significantly outpaced its peers. As of June 18, SanDisk’s year-to-date gain is about 730%, while Micron is about 260%. The core reason for this gap is not relative fundamentals, but differences in business structure that lead to different profit elasticity.

SanDisk is a pure-play NAND flash company. NAND flash is the core component of enterprise SSDs in AI data centers, and demand elasticity is extremely high. When supply-demand gaps emerge, pure NAND players’ revenue and profit growth rates often exceed those of integrated semiconductor companies. Micron’s business spans both DRAM and NAND, and DRAM (including HBM) contributes a larger portion of revenue. Differences in DRAM supply-demand structure and pricing cycles versus NAND make Micron’s overall profit elasticity relatively more moderate.

The two paths are not a matter of better or worse; they reflect differing adaptability to different market environments. In a cycle where NAND supply-demand gaps continue to widen, SanDisk’s focused model amplifies upside gains; in an environment where DRAM and NAND are simultaneously booming, an all-around layout provides a more balanced growth curve. The current market environment clearly favors the former.

From market share, global NAND market revenue in the first quarter of 2026 reached $46 billion, up 90% quarter-over-quarter. Samsung led with 29% share, SK hynix had 18%, and Kioxia, Micron, SanDisk, and Yangtze Memory are all competing for roughly 13% share for the global third spot. SanDisk gains stronger pricing power in a tight NAND supply environment through capacity coordination with its joint-venture partner Kioxia.

How do extremes in bullish-bear disagreement amplify the rally via a short squeeze effect?

As SanDisk kept setting new highs, market sentiment indicators showed extreme divergence.

SanDisk’s short positions reached a historical high at the end of May 2026. This means bullish-bear disagreement in the market is very intense—some investors believe the current price has severely deviated from fundamentals and choose to short; but the concentration of short positions also creates the potential for a short squeeze effect, which further increases buying pressure during short covering. This structure of bull-bear games, in an uptrend, often forms a positive feedback loop of “the more it rises, the more shorts; the more shorts, the more it rises.”

From a technical sentiment perspective, SanDisk’s relative strength index once broke above 99, and some market observers called it “the most overbought stock in history.” Divergence between trend-following indicators and oscillators is a classic risk signal: although the uptrend remains intact, the probability of a short-term pullback or consolidation before the next leg higher is rising.

However, disagreement by itself is not a sufficient condition for a trend reversal. In a backdrop where the storage supply-demand gap lasts far longer than the market’s initial expectations, the continued accumulation of short positions may instead provide more fuel for a subsequent short-squeeze rally.

What determines the valuation ceiling?

Returning to the core question of this article: where is SanDisk’s ceiling?

From institutional pricing, Wall Street analysts’ target price ranges are extremely broad. Morgan Stanley raised its target price from $1,100 to $1,750; Bank of America raised it from $1,550 to $2,100; Mizuho raised it from $1,825 to $2,200; and Cantor Fitzgerald set a target price of $2,900. Based on the latest ratings from 16 analysts, SanDisk’s average target price is about $1,843—yet the current price is already far above this average level.

But the upward revision of target prices is itself a dynamic process. In its latest report, Morgan Stanley noted that SanDisk’s current stock price implies an estimated P/E ratio for fiscal year 2027 that is still below 10x. Using the current forward P/E, the valuations of both companies are fairly reasonable; if you look at next year’s earnings forecasts, the valuation even appears somewhat low. This means that even if the price has already hit an all-time high, as long as earnings growth can keep up, there is still room for further valuation expansion.

The height of the ceiling ultimately depends on the evolution of three core variables:

First, the duration and depth of the supply-demand gap. If NAND oversupply-to-shortage dynamics remain tight through 2028 or even 2029, SanDisk’s earnings visibility will be greatly extended. Goldman Sachs expects 2027’s supply-demand conditions to be tighter than 2026’s—meaning upward pressure on prices has not yet peaked.

Second, the penetration rate of the new business model and pricing power. SanDisk has locked in more than one-third of fiscal year 2027 revenue through multi-year supply agreements. As a higher proportion of supply is included in this new model, earnings stability and predictability will improve further.

Third, the timeline for capacity expansion. If major manufacturers start large-scale capacity expansion early, the supply-demand gap could narrow earlier. But the current industry consensus is that before 2028 or 2029, the market will not have any significant new supply capacity coming online.

Overall, SanDisk’s ceiling is not a static number, but a range that evolves dynamically with the variables above. In a base case where the supply-demand gap continues to expand, the current price may not be the endpoint; but under conditions of extreme technical overbought signals and short positions at historical highs, short-term volatility risk cannot be ignored either.

Frequently Asked Questions (FAQ)

Q: What are the core drivers of SanDisk’s current rally?

The core drivers are the combination of three layers of logic: the pricing of pure NAND assets gained after the split from Western Digital, a surge in NAND demand driven by AI data centers, and the expansion of the supply-demand gap caused by hard constraints on capacity expansion on the supply side.

Q: Why did SanDisk’s gross margin jump from 7.1% to 78.4%?

Mainly due to a sharp rise in NAND product prices and a shift in product mix toward higher-value data center business. Data center business revenue grew 645% year-over-year in fiscal year 2026 third quarter; the increased share of high-margin products directly lifted overall gross margin.

Q: What is the biggest controversy around SanDisk in the market?

The biggest controversy centers on how well valuation matches fundamentals. Bears argue that the current price has severely deviated from fundamentals, while bulls believe the forward P/E is still within a reasonable range and that earnings growth will absorb the valuation.

Q: How long is the NAND supply-demand gap expected to last?

Mainstream institutions expect that before 2028 or 2029 there will be no significant new supply capacity coming online. Goldman Sachs predicts that AI-driven storage shortages will last at least until 2028.

Q: Why is the difference in gains between SanDisk and Micron so large?

SanDisk is a pure-play NAND flash company, and in the NAND upcycle its profit elasticity is higher. Micron’s business spans both DRAM and NAND, and its overall profit elasticity is relatively more moderate.