In May 2026, prediction market platform Polymarket launched a series of contracts targeting valuations of private AI companies, and the question “What valuation will Anthropic reach by December 31?” quickly became one of the platform’s most popular contracts. As of May 20, 2026, the contract’s total trading volume had already surpassed $180k, and market funds were especially concentrated on betting on higher valuation ranges.

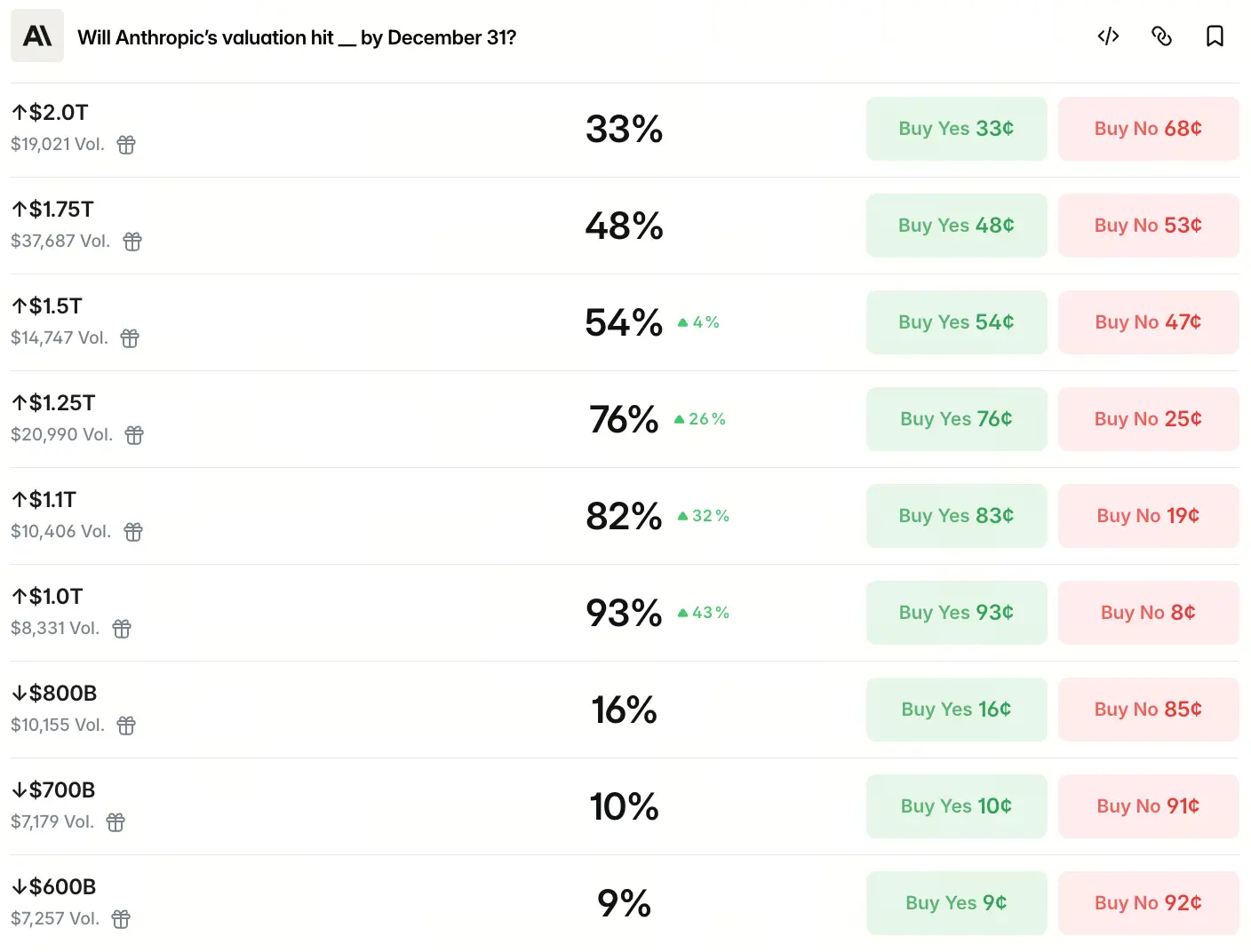

Polymarket divides valuation ranges into multiple tiers. Based on the data, the probability that the funds are betting decreases in a stepwise manner as the target valuation increases. The data shows the market assigns a 93% probability that Anthropic’s year-end valuation will exceed $1 trillion, an 82% probability of exceeding $1.1 trillion, a 76% probability of reaching $1.25 trillion, a 54% probability of reaching $1.5 trillion, a 48% probability of reaching $1.75 trillion, and a 33% probability of reaching $2 trillion. In the sub-$1 trillion tiers, the probability is only 16% for $800 billion, 10% for $700 billion, and 9% for $600 billion.

This probability distribution exhibits a typical “high-confidence concentration above the trillion-dollar mark” trait. The market’s mainstream expectation is not moderate growth; instead, it directly assumes that Anthropic will cross the $1 trillion threshold before year-end. So, where does this judgment come from?

What probability distribution is revealed by Polymarket’s betting data

From a 93% probability of betting on $1 trillion and above, down to 33% once it breaks $2 trillion, this probability curve outlines the market’s expected boundary for the upper end of Anthropic’s valuation. The key takeaway is that the market is almost uninterested in the lower valuation ranges (below $1 trillion), while expectations are most concentrated in the $1 trillion to $1.5 trillion range, with all three tiers having probabilities above 50%.

Source: Polymarket

What’s notable is that the funds betting on higher valuation ranges have not dropped to zero as the target increases. At $2.5 trillion, 16% probability remains; above $3 trillion, it stays at 13%, indicating that some traders still believe extreme overvaluation is possible. In effect, this kind of probability distribution reflects two perceptions of the AI race in the market: the mainstream view points to steady growth at the trillion-dollar scale, while the tail view points to more imaginative upside.

This betting distribution also mutually corroborates Polymarket’s other related contracts. On the same platform, data shows the probability that Anthropic’s 2026 valuation exceeds OpenAI’s is as high as 94%, and the probability that Anthropic enters the public market earlier than OpenAI is about 69%. Together, these cross-contract data point to a conclusion: the market is not only highly optimistic about Anthropic’s absolute valuation, but also believes it has an advantage in relative competition.

How massive funding rounds drive valuations to jump quickly

Behind the valuation expectations is first the size and pace of the funding rounds themselves. In February 2026, Anthropic completed a $30 billion Series G round, with a post-money valuation of $380 billion. Just three months later, according to a May 13 report by The New York Times, Anthropic was in discussions with investors for a new round of $30 billion to $50 billion; once completed, the post-money valuation would reach $950 billion, surpassing the $852 billion valuation of OpenAI after its March funding this year, becoming the AI company with the highest valuation globally.

If you extend the timeline, the acceleration in valuation growth looks even more pronounced: $61.5 billion valuation in the 2025 March E round, $183 billion in the 2025 September F round, $380 billion in the 2026 February G round, and then $950 billion reported in May—over 15x valuation growth in 14 months.

Citing insiders, Bloomberg reported that the earliest this funding could close is at the end of May 2026, with a target size potentially up to $50 billion. Using $44 billion ARR as the basis, this implies a price-to-sales multiple of about 21 to 23x. In the traditional SaaS industry, this valuation level is far above the average 8 to 12x range. But with annualized revenue doubling on a quarterly cycle, the market’s tolerance for premium pricing is significantly higher.

Can revenue growth support the trillion-dollar valuation expectations?

The core foundation of the high valuation is revenue growth pace. As of May 2026, Anthropic’s annualized revenue had risen to above $44 billion. That is nearly 5x growth from roughly $9 billion at the end of 2025. Over the past 12 months, annualized revenue added $35 billion, equivalent to about $96 million increase per day.

The acceleration in revenue growth shows a clear stepped pattern. From December 2024 to September 2025, ARR grew by about $4 billion; from September 2025 to February 2026, it added another about $5 billion; and the real surge came after February 2026—within just 3 months, ARR jumped from $14 billion to $44 billion. This growth curve suggests that the slope of revenue growth itself is accelerating, rather than progressing in a linear, steady manner.

The key engine driving revenue growth is the programming tool Claude Code. Since its release in May 2025, Claude Code’s annualized revenue has reached $2.5 billion, with a market share as high as 54% in the AI programming tools market, significantly outpacing major competitors. About 4% of GitHub public code submissions are done by Claude Code, and that share is still climbing rapidly.

On the profitability side, Anthropic’s inference gross margin has risen from roughly 38% in the early stage to over 70%. Unit economics have improved significantly, indicating that revenue growth is not relying purely on large-scale Hashrate subsidies, but is accompanied by optimization of the cost structure. However, on the other hand, Anthropic plans to spend about $19 billion in 2026 on training and inference compute. Inference costs are about 23% higher than expected, so gross margin is compressed to about 40%. The company expects to reach break-even only by 2028.

Wall Street investment banks’ view on valuation upside space is also based on the sustainability of revenue growth. If you assume that ARR at the end of 2026 approaches $60 billion, then using a 23x ARR multiple, the valuation would land in the $1.2 trillion to $1.3 trillion range. This aligns closely with Polymarket’s current main betting range of $1 trillion to $1.5 trillion.

Why prediction markets are concentrating bets on the trillion-dollar threshold

Polymarket’s high concentration on that threshold is driven by four overlapping logics: positive feedback from funding rounds, strategic games among cloud providers, the timing window of IPO expectations, and the narrative structure inherent to the AI sector itself.

From the perspective of funding rounds, Anthropic’s financing cadence shows an acceleration pattern where valuation doubles every 3 to 5 months. If the target valuation of $950 billion is delivered as scheduled by the end of May, then within a 7-month window from May to December, combined with another round of financing or price discovery in the secondary market, it is mathematically unnecessary for valuation growth to reach an extraordinary pace to move into the $1 trillion to $1.2 trillion range.

From the viewpoint of strategic investors, in April 2026 both Amazon and Google announced major investment plans for Anthropic. Amazon committed to spending over $100 billion over the next 10 years for AWS technology procurement, and additionally will invest $25 billion. Google announced it would provide $10 billion in cash and also promised to add up to $30 billion after performance milestones are met, with a total cap of $40 billion. Deep binding with multiple cloud vendors provides stable channel support for long-term penetration with enterprise customers.

IPO expectations are also a key variable for driving valuations. As reported by Bloomberg, Anthropic expects to initiate an IPO as early as October 2026, with fundraising potentially exceeding $60 billion. This timing window means that Polymarket’s contract deadline of December 31 falls right within the overlapping period of IPO execution and the first round of price discovery after listing.

More fundamentally, the AI sector’s valuation logic itself is different from traditional SaaS. Instead of being treated like conventional software companies, top large-model enterprises are assigned a “next-generation computing platform” narrative. Chen Yu, managing partner at Cloud Rise Capital, previously said that if large models can handle part of knowledge work at one-tenth the cost, “a trillion-dollar valuation is not necessarily expensive,” corresponding to a potential market on the order of ten trillion. This logic is directly reflected in the funds behind Polymarket’s bets.

Factors that could cause the actual valuation to deviate from expectations

Despite strong market consensus, there are still several key variables that could pull actual valuations down during the execution of the valuation.

The first major variable is disagreement in how revenue is recognized. OpenAI previously publicly questioned that Anthropic’s $180k in annualized revenue uses the gross revenue recognition method—when customers use its models via platforms such as Amazon Cloud and Google Cloud, Anthropic records all end-user spending as revenue, and then records the share paid to the cloud platform as expense. OpenAI estimates that after deducting these revenue shares, Anthropic’s real annual revenue is closer to $22 billion. This roughly $8 billion difference is not an accounting technical issue; it will become a focus of scrutiny by regulators and the market at the time of the IPO.

The second major variable is the dependence of valuation itself on growth rates. Based on a $950 billion target valuation and roughly $44 billion ARR, the implied price-to-sales multiple is about 20x, far above the 8 to 12x typical range in the SaaS industry. To support the current valuation, Anthropic needs to maintain at least 50% year-over-year growth for the next 3 years. If revenue growth slows in the second half of 2026, pressure for valuation adjustments will rise significantly.

The third major variable comes from market competition and policy risk. In both consumer and enterprise products, Anthropic is in fierce competition with OpenAI, Google, and xAI. In addition, prior contract disputes between Anthropic and the Pentagon, as well as the label by the U.S. government of “supply chain risk,” add uncertainty for both listing and business expansion.

Deriving the end-of-year valuation range from multi-dimensional logic

Combining the funding progress, revenue growth pace, IPO expectations, and competitive landscape, you can reason about the end-of-year valuation through multiple dimensions.

Anchoring on the probability distribution of Polymarket’s betting data, market expectations show a “core range of $1 trillion to $1.5 trillion, with the tail extending above $2 trillion” pattern. This distribution structure effectively establishes three layers of valuation reference: the $950 billion financing valuation as a baseline reference; a midpoint expectation of $1.1 trillion to $1.25 trillion; and a high-elasticity scenario of $1.75 trillion to $2 trillion. Looking at the 33% probability of betting on the $2 trillion tier, the market does not treat this target as an extremely unexpected outcome; instead, it assigns a substantial weight.

The reasonableness of this probability distribution needs to be evaluated against the broader valuation coordinate system for the AI industry. Today, OpenAI’s valuation is around $852 billion, with ARR around $24 billion to $25 billion; SpaceX’s valuation is around $1.4 trillion to $1.75 trillion. Anthropic’s $950 billion financing valuation sits between the two, but its roughly $44 billion ARR is already significantly higher than OpenAI’s level in the same period. Using price-to-sales as the valuation anchor: if OpenAI’s implied P/S multiple is about 34x to 35x, then $44 billion ARR corresponds to an estimated valuation of about $1.5 trillion—exactly overlapping with Polymarket’s 54% probability betting interval. This arithmetic relationship indicates that market pricing is not made out of thin air divorced from fundamentals; rather, it is a finely calibrated game built on an anchor set by the P/S multiple.

For those tracking Polymarket contracts, there are three core variables that need continuous monitoring:

- The actual valuation outcome after the funding closes by the end of May;

- Whether the ARR growth driven by Claude Code can continue the momentum of doubling each quarter;

- The pace of progress on key time nodes for the IPO.

Each time a funding announcement or financial data is released, it may trigger a repricing of market expectations, and the price movement of the Polymarket contracts themselves will also reflect the market’s collective updates to its view of the above variables.

FAQ

Q: How does Polymarket determine the result for its valuation contract?

Polymarket has signed an exclusive data collaboration agreement with the Nasdaq private market, which will serve as the exclusive settlement data provider. The final result will be determined based on its daily-updated private market valuation estimates. If Anthropic completes an IPO before the contract expires, settlement is based on publicly traded market transaction prices.

Q: Does the 93% probability shown by Polymarket data equal the real probability of the valuation?

Prediction market prices reflect participants’ collective expectations rather than objective probabilities. Their accuracy is affected by many factors, including liquidity, participant composition, and the ability to obtain information. When the contract’s total trading volume continues to expand, the market representativeness of the price signal improves.

Q: Could Anthropic be valued below $1 trillion by the end of 2026?

Polymarket data shows that the probability of being below $800 billion is only 16%, but constraints still exist for how valuations land in practice. These mainly include: disagreements in revenue recognition, which may face more stringent regulatory scrutiny at the IPO stage; the growth expectations implied by a high price-to-sales multiple—if they fail to materialize, valuation downgrade pressure will follow; and product iteration by competitors and the struggle over market share.