マイクロストラテジー「無限買幣」モード終了!MSCI フリーローン効果条項凍結

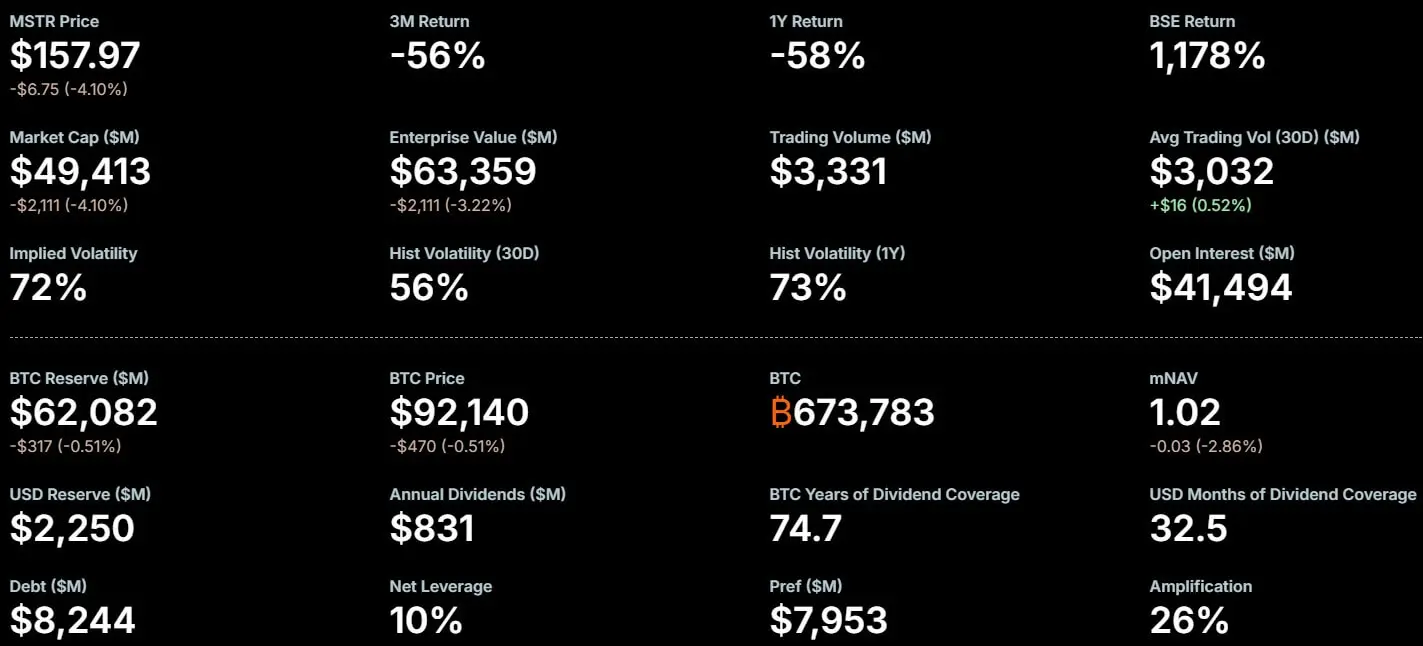

MSCI retained MicroStrategy but froze share count, severing the link between new issuances and passive purchases, ending the flywheel effect. Bull Theory quantification shows that every 20 million newly issued shares result in $600 million loss in passive buying pressure. MicroStrategy’s 2025 issuance of over $15 billion in new stock faces unsupported dilution effects under the new rules, increasing risk of price pullback.

The Fatal Hidden Clause in MSCI’s Freeze

The threat of massive forced selling pressure on cryptocurrency-related stocks has been averted. However, this reprieve comes with a structural defect that fundamentally alters the economics of “Bitcoin Treasury” trading. MSCI’s statement reads: “Currently, companies whose digital asset holdings represent 50% or more of total assets, as listed in MSCI’s preliminary announcement, will maintain their current treatment in the index.”

Following the announcement, MicroStrategy Executive Chairman Michael Saylor praised the company for successfully remaining in the benchmark index, with stock price surging over 6%. However, the market quickly discovered a fatal clause hidden in the fine print. MSCI simultaneously implemented a technical freeze on the share count of these entities: “MSCI will not increase the number of shares (NOS), foreign inclusion factor (FIF), or domestic inclusion factor (DIF) of these securities. MSCI will postpone any new additions or size tier adjustments for all securities on the preliminary list.”

Through this decision, MSCI effectively severed the link between new stock issuances and automatic passive purchases. This means that while the “downside risk” of forced liquidation has been eliminated, the “upside” mechanism of index trading has been dismantled. The market reacted immediately. JPMorgan had previously stated that complete exclusion could trigger $3-9 billion in passive selling for MSTR. Such large transaction volumes would likely cause stock price to plummet and force MicroStrategy to sell bitcoin. While this worst-case scenario was indeed avoided, the cost is the loss of a more important growth engine.

How the Flywheel Effect Was Completely Destroyed

(Source: MicroStrategy)

Historically, when MicroStrategy issued new shares to fund bitcoin acquisitions, index providers would eventually update share counts. Therefore, passive funds tracking the index were mathematically forced to proportionally purchase newly issued shares to minimize tracking error. This created a guaranteed, price-insensitive source of demand that helped absorb dilution. This was MicroStrategy’s “flywheel effect”: issue new shares → index updates weights → passive funds forced to buy → stock price supported → MicroStrategy continues issuing → cycle repeats.

Under the new “freeze” policy, this cycle is broken. Even if MicroStrategy significantly expands its outstanding share base to raise capital, MSCI will effectively ignore these new shares in index calculations. The company’s index weight will not increase, and therefore, ETFs and index funds will not be forced to buy new shares. Market analysts point out that this transformation forces the market back to fundamentals. Without support from benchmark index tracking demand, MicroStrategy and its peers must now rely on active fund managers, hedge funds, and retail investors to absorb new supply.

Cryptocurrency research firm Bull Theory quantified this liquidity gap in a report to clients. The firm modeled a treasury company with 200 million outstanding shares, of which approximately 10% are typically held by passive index-tracking funds. In Bull Theory’s model, if a company issues 20 million new shares to raise capital, then the old index mechanism would ultimately force passive funds to purchase 2 million of them.

Quantified Analysis of the Liquidity Gap

Passive buying under old mechanism: Per 20 million shares issued, passive funds forced to buy 2 million shares (10% proportion)

Assumed price per share: $300

Scale of automatic buying: $600 million in price-insensitive purchasing pressure

Passive buying under new rules: Zero

Bull Theory notes that under MSCI’s latest freeze policy, the $600 million bid would drop to zero. “Now MicroStrategy must seek private buyers, offer discounts, or reduce financing.” This means that forced demand from index funds has been eliminated. This represents a major obstacle for MicroStrategy, which issued over $15 billion in new shares in 2025 to aggressively accumulate bitcoin.

If the company attempts to replicate such large-scale offerings in 2026, it would do so in a market environment lacking passive support. Without this structural support, the risk of price pullback during dilution events would increase significantly. Investors may sell on every new issuance announcement, anticipating prices will decline due to lack of passive buying pressure. This expectation becomes self-fulfilling, creating a negative feedback loop.

Spot ETFs Emerge as Biggest Winners

MSCI’s decision to restrict these companies’ index weights rather than expel or leave them alone has also significantly altered competitive dynamics in the asset management industry. Over the past year, US spot bitcoin ETFs as an asset class have matured and attracted intense institutional investor interest. From this perspective, MicroStrategy competes with these fee-charging bitcoin ETFs, offering investors a way to gain passive bitcoin exposure through an operating company structure.

The new rules froze digital asset companies’ index weights, weakening their ability to expand effectively through stock markets. If MicroStrategy’s ability to raise cheap capital is curtailed, large asset allocators may redirect funds from corporate stock to spot ETFs, as spot ETFs do not carry the company’s operational risk or volatility in premium relative to net asset value. This fund flow would directly benefit spot ETF issuers, including major Wall Street banks, effectively capturing the fees previously reflected in stock premiums.

By weakening MicroStrategy’s “flywheel” effect, index providers may have intentionally or unintentionally created a more favorable competitive environment for traditional asset management products. This is a zero-sum game: the passive buying pressure MicroStrategy lost is precisely the incremental capital spot ETFs gain. For ETF issuers like BlackRock and Fidelity, MSCI’s decision is a windfall.

関連記事