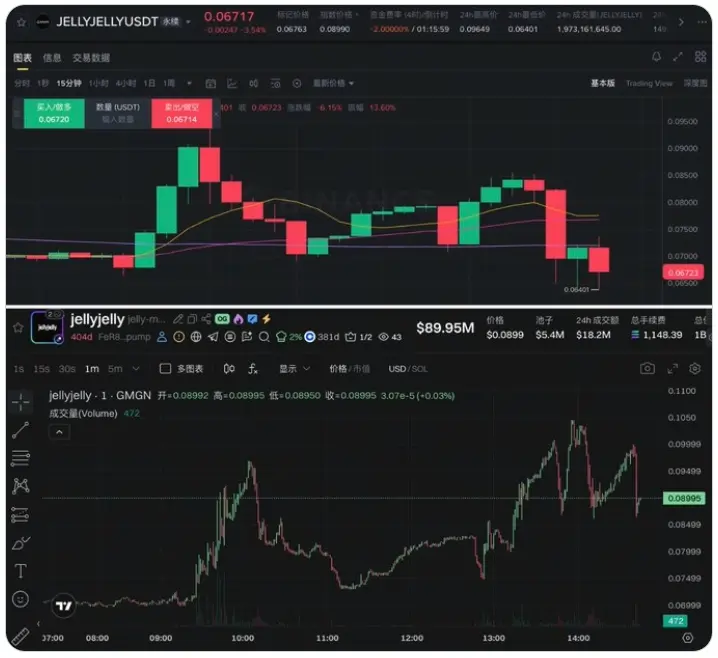

On March 10, JELLYJELLY tokens experienced an extreme divergence between the perpetual contract mark price on mainstream trading platforms and the on-chain spot price: the perpetual contract mark price was $0.067, while the on-chain spot price was $0.092, with the maximum spread reaching approximately 34%. Analyst Ai Yi pointed out that open interest surged around 1 PM, with a trend highly similar to previous similar incidents, suggesting possible repeated price manipulation.

34% Price Disparity Analysis: What Does the Extreme Divergence Between Contract and Spot Mean?

(Source: Ai Yi)

A significant deviation between the contract mark price and the spot price is one of the highest risk warning signals in the crypto derivatives market. Under normal market conditions, the perpetual contract mark price usually stays within a 1-2% reasonable deviation from the spot price; a deviation over 10% is abnormal, and a 34% divergence is almost impossible to explain through natural market behavior.

This divergence structure shows that the perpetual contract mark price ($0.067) is significantly lower than the on-chain spot price ($0.092), indicating that the contract side has been artificially suppressed, while the spot side has been relatively pushed higher. In this scenario, an extreme negative funding rate of -2% over 4 hours means short holders can collect 2% of their position every 4 hours from long holders—creating a strong short-term arbitrage incentive for shorts but imposing heavy holding costs on regular long positions.

Funding Rate -2% — A Crisis Signal: A Typical Precursor to Market Manipulation

Ai Yi warns of a manipulation pattern with a history in crypto markets:

- Surge in Open Interest: Open interest across the network skyrocketed from normal levels to $39.2 million, with the surge timing (around 1 PM) matching previous similar events.

- Extreme Negative Funding Rate: -2%/4 hours indicates a concentrated short position and dominance, which is difficult to sustain long-term.

- Discrepancy Between Spot and Contract Prices: Spot prices are significantly higher than contract mark prices, suggesting possible price suppression on the contract side while maintaining high levels on the spot side through dual operations.

- On-Chain Market Cap: The relatively small on-chain market cap of $9.3 million makes it easier for large funds to influence prices through limited liquidity.

Analysts warn investors that such extreme divergence between contract and spot prices often leads to forced liquidations and rapid price corrections, representing a high-risk window.

DEX Market Context: Structural Issues Reflected in the JELLYJELLY Incident

The abnormal divergence in JELLYJELLY also reflects structural risks in the ongoing integration of decentralized and centralized trading infrastructure. According to CoinGecko’s 2026 CEX and DEX trading report, DEX spot market share increased from 6.9% in January 2024 to 13.6% in January 2026, with DEX perpetual contract trading volume growing eightfold, and market share rising from 2.0% to 10.2%. Hyperliquid is the only DEX among the top ten perpetual platforms, holding a 3.3% share, surpassing some mid-sized CEXs.

In this context, when prices between on-chain spot and centralized exchange contracts diverge extremely, cross-platform arbitrage becomes more difficult due to factors like fund transfer speeds, gas fees, and liquidity depth differences. These barriers can extend the duration of the deviation, making manipulation more sustainable.

Frequently Asked Questions

What does the 34% inversion between JELLYJELLY contract and spot mean for traders?

For those holding long contract positions, a -2%/4 hours funding rate means paying about 2% of their position every 4 hours to shorts, making long-term holding very costly. For spot holders, such a large price gap might present arbitrage opportunities by selling spot and entering long contracts, but they also face risks of market volatility and liquidity shortages.

What level is a -2%/4 hours funding rate in the market?

-2%/4 hours translates to approximately -12% daily, which is extremely rare in crypto derivatives markets. Normal funding rates are usually between ±0.01% and ±0.1% per 8 hours; exceeding -0.5%/8 hours is abnormal. A rate of -2%/4 hours indicates a severely imbalanced and highly volatile market.

How does this JELLYJELLY incident compare to historical price manipulation?

Analyst Ai Yi notes that current features include: abnormal concentration of open positions at surge points, extreme negative funding rates, and large discrepancies between spot and contract prices. These characteristics closely resemble previous JELLYJELLY incidents, where manipulators often build large short positions on contracts and then trigger forced liquidations in the spot market to profit.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.