BloFin Research has published the latest whale research report, providing an in-depth analysis of Circle. It points out that the company’s profit model can be summarized into three core drivers: “interest rates, USDC scale, and distribution economics.” However, the recent interpretation of the “GENIUS Act” by the U.S. Office of the Comptroller of the Currency (OCC) is creating significant uncertainty for Circle’s critical distribution partnerships.

The Three Main Drivers: Interest Rates, Scale, and Distribution

BloFin Research breaks down Circle’s core business model into three interconnected layers:

Interest Rates: In Q4, Circle’s reserve earnings reached $733 million, up 69% year-over-year, accounting for the vast majority of total revenue. However, the reserve return rate has fallen from its peak to 3.8%, down 68 basis points from the previous year, reflecting the direct impact of the Federal Reserve’s rate cuts on reserve income. The expansion of USDC’s scale currently offsets the decline in per-unit yields.

USDC Scale: The scale determines the reserve base and acts as a multiplier to amplify or reduce the impact of interest rate changes. Management expects USDC circulation to maintain a 40% compound annual growth rate (CAGR) over the next few years. This assumption underpins the continued growth of reserve income.

Distribution Economics: In Q4, distribution, trading, and other related costs totaled $461 million, up 52% year-over-year, indicating that USDC distribution still heavily relies on partnerships, especially the unique arrangement with Coinbase. The report also notes that Circle’s “Other Income” (non-reserve sources) reached $110 million in 2025, exceeding expectations, showing that payment infrastructure businesses like Circle Payment Network are gradually supplementing non-reserve income sources.

Stablecoin Breaks Through Crypto Bear Market for the First Time: Structural Resilience of USDC

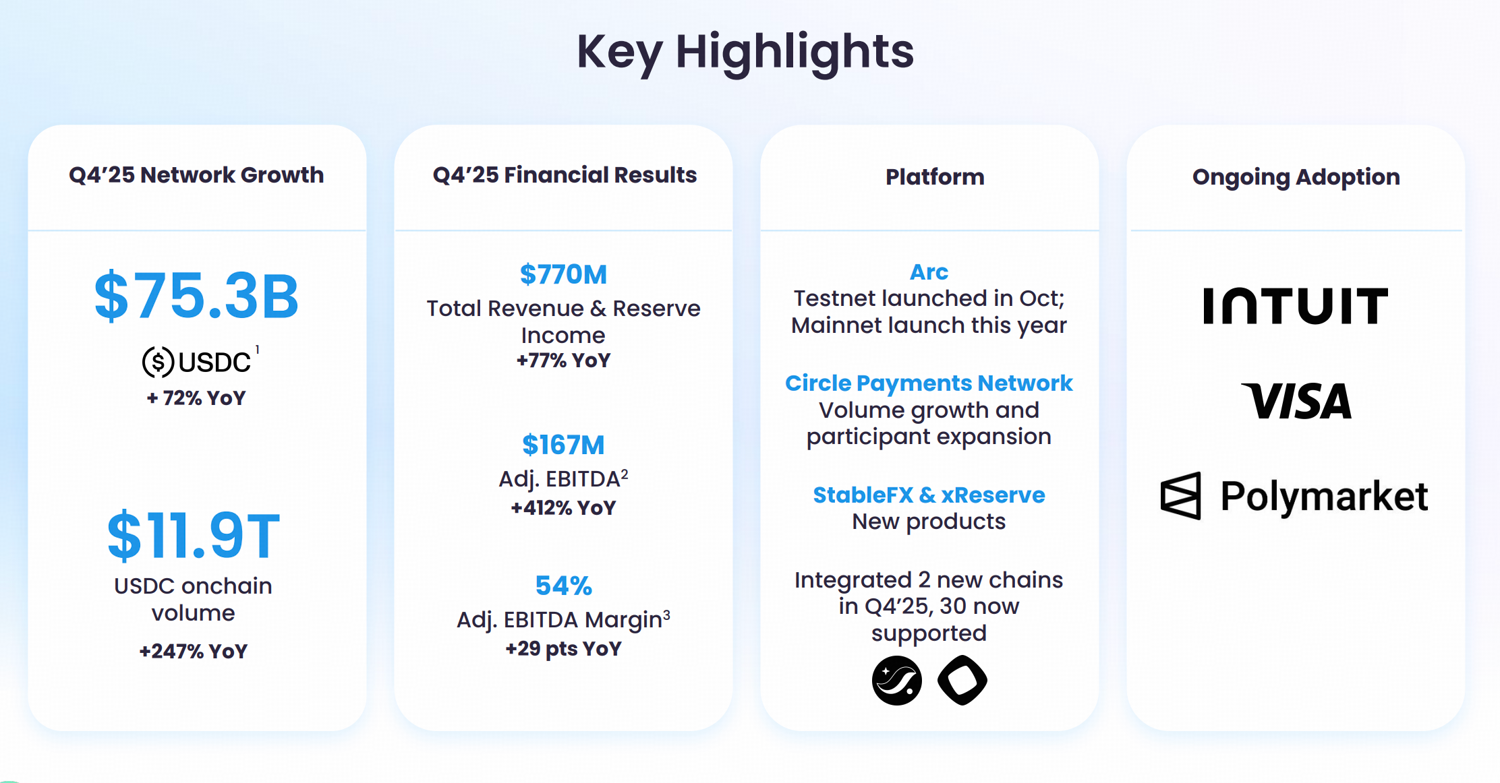

(Source: Circle)

The most strategically significant observation in the BloFin Research report is the historic decoupling of stablecoin supply from crypto market price volatility. Despite Bitcoin falling nearly 50% from its 2025 peak, the total market cap of stablecoins remains near a record high of approximately $310 billion. Unlike previous bear markets, notable points include:

February 2026: During a period of “extreme fear” in crypto market sentiment index, stablecoin monthly trading volume still hit a record $1.73 trillion (Data source: Visa On-Chain Analytics).

Past Bear Markets: Similar declines typically involved massive stablecoin redemptions, decoupling events, and significant outflows of ecosystem funds.

The report attributes this structural shift to two key factors: First, stablecoin use cases have expanded from crypto trading pairs to cross-border settlements, on-chain payments, and institutional fund management, greatly reducing the direct link to speculative risk appetite. Second, market infrastructure has matured, with increased transparency of reserves, strengthened issuer regulation, and deeper integration with traditional finance, collectively reducing the risk of disorderly redemptions during market volatility.

For Circle, this means that the stability of stablecoin supply translates into a more stable reserve base, which is the engine of Circle’s reserve income. This, in turn, gradually decouples its revenue cycle from crypto market price cycles.

Major Risk: OCC Regulatory Interpretation Threatening Coinbase Distribution Model

BloFin Research highlights the most significant current risk for Circle. The OCC’s recent interpretation of the “GENIUS Act” suggests that if stablecoin issuers share reserve income with distribution partners, and those partners provide user rewards based on stablecoin balances, regulators might consider this arrangement as an impermissible “indirect transfer of earnings.”

This interpretation directly impacts the longstanding core business arrangement between Circle and Coinbase—under their distribution agreement, most of Circle’s reserve income is shared with Coinbase to incentivize the promotion of USDC and reward users based on stablecoin balances. If such arrangements are deemed illegal, USDC’s distribution efficiency among Coinbase’s large retail and institutional customer base could face fundamental challenges.

BloFin Research concludes that until the OCC finalizes rules and legislative negotiations clarify third-party reward handling, the Circle-Coinbase distribution structure remains the biggest short-term uncertainty for Circle’s profit outlook.

FAQs

Q: What are the “three drivers” of Circle according to BloFin Research?

A: BloFin Research summarizes Circle’s core business model into three layers: interest rates (affecting reserve yields), USDC scale (determining reserve size), and distribution economics (governing revenue sharing with partners). Together, they form the foundation of Circle’s profit framework; changes in any single factor can have multiplier effects on overall performance.

Q: Why is OCC’s interpretation of the “GENIUS Act” a major risk for Circle?

A: The “GENIUS Act” prohibits stablecoin issuers from directly paying earnings. The OCC’s new proposal suggests that if issuers share reserve income with distribution partners, and those partners provide user rewards linked to stablecoin balances, such arrangements are “highly likely” to constitute prohibited indirect earnings transfer. This could directly impact Circle’s current distribution agreement with Coinbase, weakening USDC’s promotion via Coinbase channels.

Q: What does the decoupling of stablecoin supply from the crypto bear market mean for Circle long-term?

A: The decoupling indicates that Circle’s reserve base no longer shrinks significantly during bear markets, making its reserve income more predictable and stable. BloFin Research notes that as stablecoin applications deepen, Circle’s revenue system will increasingly detach from crypto price cycles, potentially supporting a long-term revaluation of its stock from speculative to fundamentals-based pricing.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.