The U.S. Federal Reserve released a document on Thursday explicitly stating that banks should treat tokenized securities the same as traditional securities when calculating regulatory capital. The document emphasizes that the current capital framework is “technologically neutral,” and that blockchain technology itself does not influence the method of regulatory capital recognition. This guidance represents the second major written directive from the leading U.S. financial regulators regarding on-chain tokenized assets, following the SEC’s confirmation in January that tokenized securities fall under federal securities laws.

Federal Reserve FAQ: Five Core Positions

(Source: Federal Reserve)

(Source: Federal Reserve)

This document clarifies the regulatory stance and provides clear compliance guidance for financial institutions:

Technology Neutrality Principle: The technology used to issue or transfer securities (including blockchain technology) does not affect how regulatory capital is treated; the legal nature and risk characteristics are the core criteria for capital treatment.

Equal Treatment Rule: Qualified tokenized securities should be subject to the same capital rules as non-tokenized securities.

Financial Collateral Eligibility: If tokenized securities meet the same legal and risk management standards as traditional securities, they can be used as financial collateral under existing rules.

Blockchain Type Irrelevance: Capital rules do not differentiate between permissioned and permissionless blockchains.

Existing Framework Applies: There is no need to wait for new legislation; banks can directly operate tokenized securities businesses under the current capital framework.

SEC and Federal Reserve Double Confirmation: Formalizing a Complete Regulatory Loop

The Federal Reserve’s guidance is not an isolated event but part of a systematic effort by U.S. regulators to clarify the legal status of blockchain assets. In January, the SEC first confirmed that tokenized securities are subject to federal securities laws, requiring registration, disclosure, and investor protection measures similar to those for traditional securities. The recent confirmation by the Federal Reserve that tokenized securities hold an equivalent status in bank capital calculations further completes the regulatory loop, covering both legal and capital treatment frameworks.

For large financial institutions actively exploring tokenization, such as BlackRock and Fidelity, regulatory uncertainty has long been a major obstacle to advancing tokenized products. This double confirmation significantly reduces compliance friction and provides a more solid policy foundation for scaling tokenization activities.

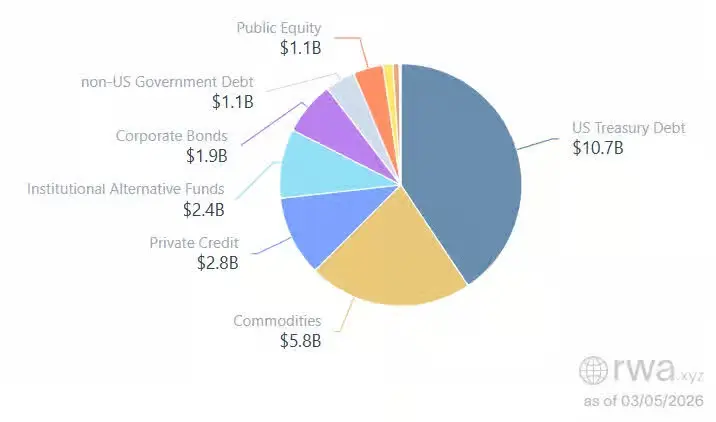

RWA Market Status: Policy Benefits for a $26 Billion Market

(Source: RWA.xyz)

(Source: RWA.xyz)

This guidance coincides with rapid growth in the real-world asset (RWA) tokenization market. According to the latest data from RWA.xyz, the market value of publicly traded tokenized stocks is approximately $1.1 billion, with the broader tokenized RWA market reaching $26 billion, predominantly led by tokenized U.S. Treasury products.

The Federal Reserve’s clarification of capital rules expands the application scope for tokenized RWAs from a banking capital management perspective: banks holding tokenized Treasuries or stocks no longer face additional capital deductions and can consider including them as financial collateral, further aligning tokenized assets with traditional financial instruments.

Frequently Asked Questions

Q: What practical impact does the Federal Reserve’s “technology neutral” principle have on banks?

A: Banks evaluating regulatory capital requirements for tokenized securities do not need to adopt conservative measures solely because of the “tokenized” technology form. As long as the legal nature and risk profile are the same as traditional securities, the same capital rules apply. This allows banks to directly apply existing capital frameworks to tokenized activities, reducing compliance uncertainty.

Q: How can tokenized securities qualify as financial collateral?

A: To qualify as financial collateral, tokenized securities must meet legal requirements (including SEC registration compliance) and risk management standards (such as liquidity and credit ratings). These standards are identical to those for traditional securities. If these are met, banks can use them as collateral under current capital rules without waiting for new specific regulations.

Q: What is the difference and connection between this Federal Reserve guidance and the SEC’s January clarification?

A: The SEC’s clarification focuses on the legal aspect, confirming that issuance and trading of tokenized securities must comply with federal securities laws. The Federal Reserve’s guidance focuses on capital management, confirming that banks should treat tokenized and non-tokenized securities equally in capital calculations. Together, they cover different regulatory dimensions, forming a comprehensive policy framework for institutional applications of tokenized traditional assets.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.