Stay ahead of the market with our Weekly Crypto Report, covering macro trends, a full crypto markets overview, and the key crypto highlights.

TL;DR

Rising geopolitical tensions involving Iran are creating material risks for global trade, with potential impacts including supply-chain disruptions, higher commodity prices, and shifts in global capital allocation.

This week’s key macroeconomic releases include ISM Manufacturing and Services PMIs, trade balance data, export and import price indices, and the U.S. employment report.

BTC (-1.73%) and ETH (-0.91%) edged lower last week, but spot ETF flows remained strong with record inflows of 787M(BTC)and80M (ETH).

Among the top 30 market cap tokens, prices rose ~2.1% on average, led by HYPE (+16.9%) as Hyperliquid’s oil perps jumped on Iran-related supply risk and gained mainstream visibility on Bloomberg.

Fabric Foundation (ROBO) token launched, focused on governance and coordination infrastructure for human–AI collaboration. ROBO debuted at 0.022andisnowaround0.039, listed on Gate, Bybit, and Bitget.

Morgan Stanley wants an OCC trust charter for crypto custody; Barclays is exploring blockchain rails for payments/deposits; big banks are gearing up for regulated, 24/7 onchain finance.

Hyperliquid-based “SuperApp” Based raises $11.5M Series A led by Pantera Capital.

Macro Overview

The impact of Iran tensions on global trade highlights significant disruptions to supply chains, rising prices, and shifts in global capital allocation.

The escalation of tensions in Iran not only directly impacts oil supply, drives up gold prices, and increases demand in the military-industrial chain, but also causes significant disruptions to the global supply of commodities, chemical products, and shipping capacity. Iran is located at the geopolitical core of Eurasia and Africa and possesses abundant energy and mineral reserves. As of 2024, Iran accounts for 4.5% and 6.4% of global crude oil and natural gas production, respectively, and the MENA region accounts for 33.6% and 21.3%, respectively. Iran’s industry is primarily centered around oil and petrochemicals, and it is a major global exporter of methanol, urea, and propane, accounting for approximately 9%, 5%, and 6–7% of global production capacity, respectively. If the U.S. and Israel launch attacks on Iran’s industrial facilities, it could significantly drive up global prices for related chemical products. Furthermore, if Iran were to block the Strait of Hormuz for an extended period, it would cause a major disruption to global energy trade.

Since the beginning of the year, the Trump administration in the United States has further implemented the “Donroe Doctrine,” which focuses on aggressive, spectacle-driven actions like securing regional resources, addressing migration, and potential territorial expansion, introducing greater uncertainty to the global order. This has led to an increasing number of countries, including NATO allies, placing greater emphasis on utilizing more domestic resources to support their national defense systems and reindustrialization efforts, which may result in the flow of global capital away from U.S. dollar assets and back toward domestic investments.

This week’s incoming data includes ISM Manufacturing & Service PMI, trade data, export & import prices, employment report, etc. The full complement of worldwide manufacturing and services PMIs will provide updates on economic conditions in February. Friday there will be the publication of US non-farm payrolls and unemployment data. January’s payroll count surprised to the upside at 130K, its highest for just over a year, while unemployment ticked lower to 4.3%. The data caused a pull-back in US rate cut expectations, adding to the prevailing view that the FOMC will remain on hold in the next few months while it weighs the influx of new data. (1)

The US dollar index generally maintained its position between 97.4—97.9 last week, staying resilient against other major currencies. (2)

The bond yields of U.S. treasuries nearly touched 6-month low last week, as the tensions continue to escalate between U.S./Israel and Iran, and the bond yield for U.S. 10-year bonds has dropped below 4%. (3)

Last week the gold price gained significant upward momentum following the geopolitical tensions in the Middle East, as investors seek safe-haven assets during the time of significant volatilities. (4)

Crypto Markets Overview

1. Main Assets

Last week, BTC fell 1.73% while ETH slipped 0.91%. BTC spot ETFs saw a record 787.31Mnetinflow,andETHspotETFspostedarecord80.46M net inflow. (5)

Sentiment remained fragile, with the Fear & Greed Index at 10, firmly in Extreme Fear territory. Meanwhile, the ETH/BTC ratio staged a modest rebound, climbing 1.9% to 0.029. (6)

BTC experienced extreme volatility following the U.S.-Israeli strikes on Iran, plunging to 63,000beforerapidlyreboundingtoward67,000.

2. Total Market Cap

Last week, the total crypto market cap fell 1.87%. Market cap excluding BTC and ETH declined 0.55%, while the altcoin market dropped 1.09%.

3. Top 30 Crypto Assets Performance

Among the top 30 assets, prices rose ~2.1% on average, led by HYPE, LEO, and XMR.

HYPE surged 16.9%. The key catalyst was a 5% spike in Hyperliquid’s oil-linked perps after coordinated U.S.-Israeli strikes on Iran reignited supply-shock fears and Strait of Hormuz risk, driving haven flows into gold/silver perps as well. The move also drew mainstream attention, with on-chain oil pricing on Hyperliquid cited in Bloomberg for the Iran risk coverage. (7)

4. New Token Launched

Fabric Foundation (ROBO) is a non-profit organization formed in partnership with smart-machine infrastructure company OpenMind. The Foundation is building the governance, economic, and coordination infrastructure to enable humans and intelligent machines to collaborate. OpenMind is developing the OM1 operating system for intelligent machines and the FABRIC collaboration network. (8)

The token began trading at 0.022andiscurrentlyhoveringaround0.039, reflecting steady post-listing momentum. FAB is listed on major centralized exchanges including Gate, Bybit, and Bitget.

The Key Crypto Highlights

1. Morgan Stanley applies for OCC bank charter to custody crypto

Morgan Stanley has filed for a national trust bank charter with the U.S. Office of the Comptroller of the Currency under the name “Morgan Stanley Digital Trust, National Association,” aiming to custody digital assets and execute crypto transactions, including purchases, sales, swaps, transfers and staking, on behalf of clients. The move formalizes its expansion into digital asset infrastructure and follows a wave of crypto-focused trust charter applications and approvals, including Ripple, BitGo, Fidelity Digital Assets, Paxos, Bridge and Crypto.com. (9)

2. Barclays explores blockchain for payments and deposits

Barclays is evaluating blockchain infrastructure for core banking functions, including payments, deposits and crypto-related applications such as stablecoins and tokenized deposits, and has issued requests for information to potential technology partners, with a vendor decision possible as early as April. The initiative follows the bank’s recent stablecoin-related investment in Ubyx and reflects a broader industry shift as banks and Big Tech assess onchain settlement systems that enable faster, lower-cost and 24/7 payment flows. (10)

3. PayPal, MoonPay and M0 launch PYUSDx for app-specific stablecoins

PayPal, MoonPay and M0 have announced PYUSDx, a tokenization and issuance framework that lets developers quickly launch app-specific, USD-pegged stablecoins backed by PayPal USD, with features including cross-chain support, branded token options, reserve transparency and flexible economics, with rollout targeted for next month. PYUSDx is positioned as “application-layer” stablecoin infrastructure that abstracts away technical and operational overhead by combining M0’s stablecoin platform with MoonPay’s issuance rails, as competition heats up from both fintechs and Big Tech exploring stablecoin payments. The first developer to build on PYUSDx is USD.ai, which plans to issue an application-specific stablecoin for AI infrastructure. (11)

Key Ventures Deals

**1. Ripple, Franklin Templeton back 5MseedroundforAIagenttruststartupt54Labs∗∗t54Labshasraised5 million in a seed round co-led by Anagram and PL Capital and Franklin Templeton, with participation from Ripple, Virtuals Ventures and Blockchain Coinvestors, to build a “trust layer” for autonomous AI agents that transact on behalf of users and institutions. The San Francisco–based startup is developing identity verification (“know your agent”), real-time risk monitoring, agent-native credit underwriting and integrated settlement tooling, designed to be rail-agnostic while leveraging blockchains as programmable settlement and accountability layers; it’s already live on networks including XRP Ledger, Solana and Base and has built x402-secure for the Coinbase-incubated x402 agent payment protocol. (12)

**2. Hyperliquid-based “SuperApp” Based raises 11.5MSeriesAledbyPantera∗∗Based,aconsumer−facingweb3tradingandpaymentsappbuiltonHyperliquid’stradinginfrastructure,raised11.5M Series A led by Pantera with participation from Coinbase Ventures, Wintermute Ventures and Karatage, structured as equity with token warrants. Based positions itself as a mobile-first “SuperApp” that bundles wallet, on/off-ramps, a crypto-linked Visa card, perpetuals and prediction markets on top of Hyperliquid as the underlying engine; it claims 100k+ registered users, 30k MAUs and ~40Bcumulativevolume,with14M revenue largely from builder code fees plus card fees. (13)

**3. STS Digital closes 30Mstrategicroundtoscaleinstitutionalcryptooptionsmarket−making∗∗STSDigitalhascloseda30 million strategic funding round led by CMT Digital, with participation from Payward, Strobe Ventures, Arrington Capital, F-Prime and BitRock Capital, to expand its regulated, institutional-grade crypto options business and deepen its role as a liquidity provider for sophisticated counterparties. Operating as a licensed principal trading firm, STS offers a unified trading interface across UI, API and voice for spot, vanilla and exotic options, and structured products across 400+ tokens, positioning execution quality, disciplined risk management and balance-sheet strength as core differentiators for banks, asset managers and intermediaries. (14)

Ventures Market Metrics

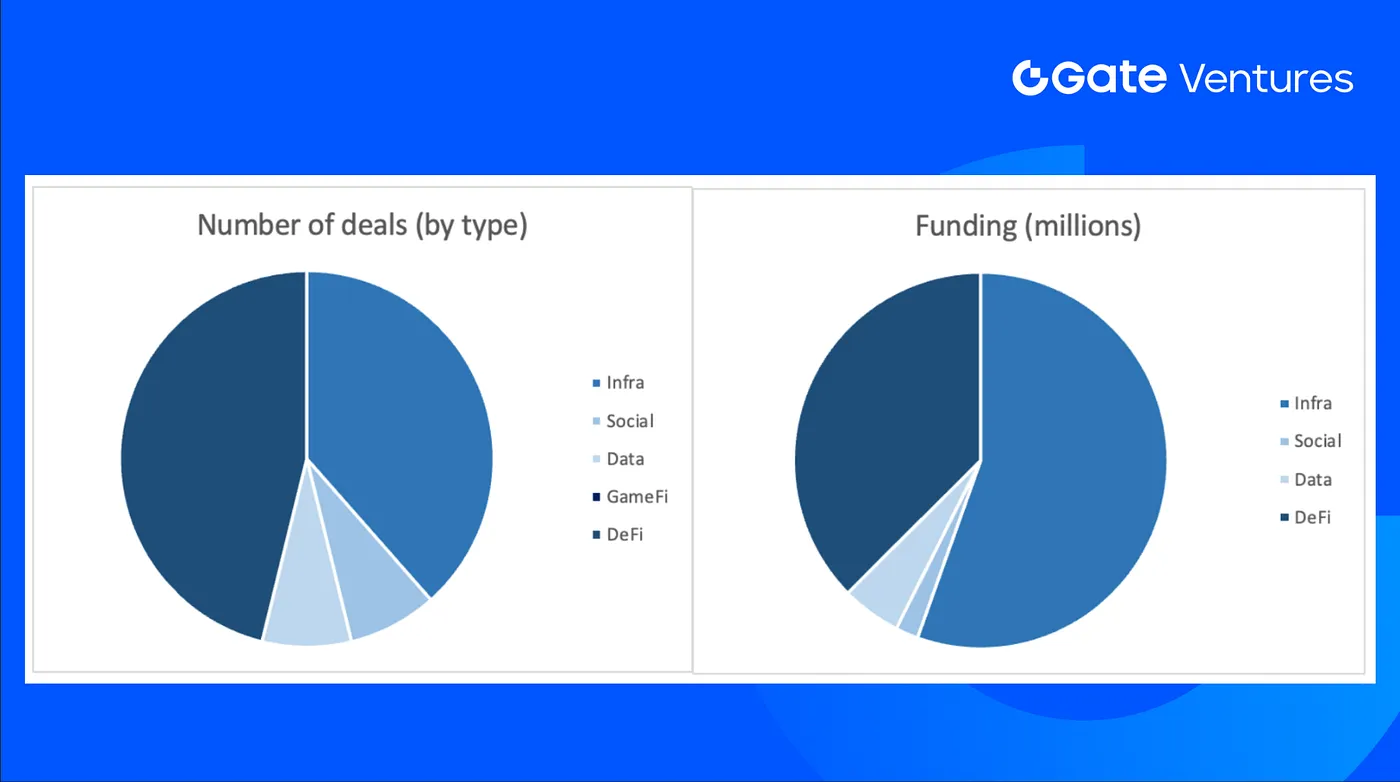

The number of deals closed in the previous week was 13, with DeFi having 6 deals, representing 46% of the total number of deals. Meanwhile, Infra had 5 deals (38%), Social had 1 deal (8%), and Data had 1 deal (8%).

The total amount of disclosed funding raised in the previous week was 76.15M,3dealsinthepreviousweekdidn’tannouncetheraisedamount.ThetopfundingcamefromtheInfrasectorwith42.25M. Most funded deals: STS Digital ($30M).

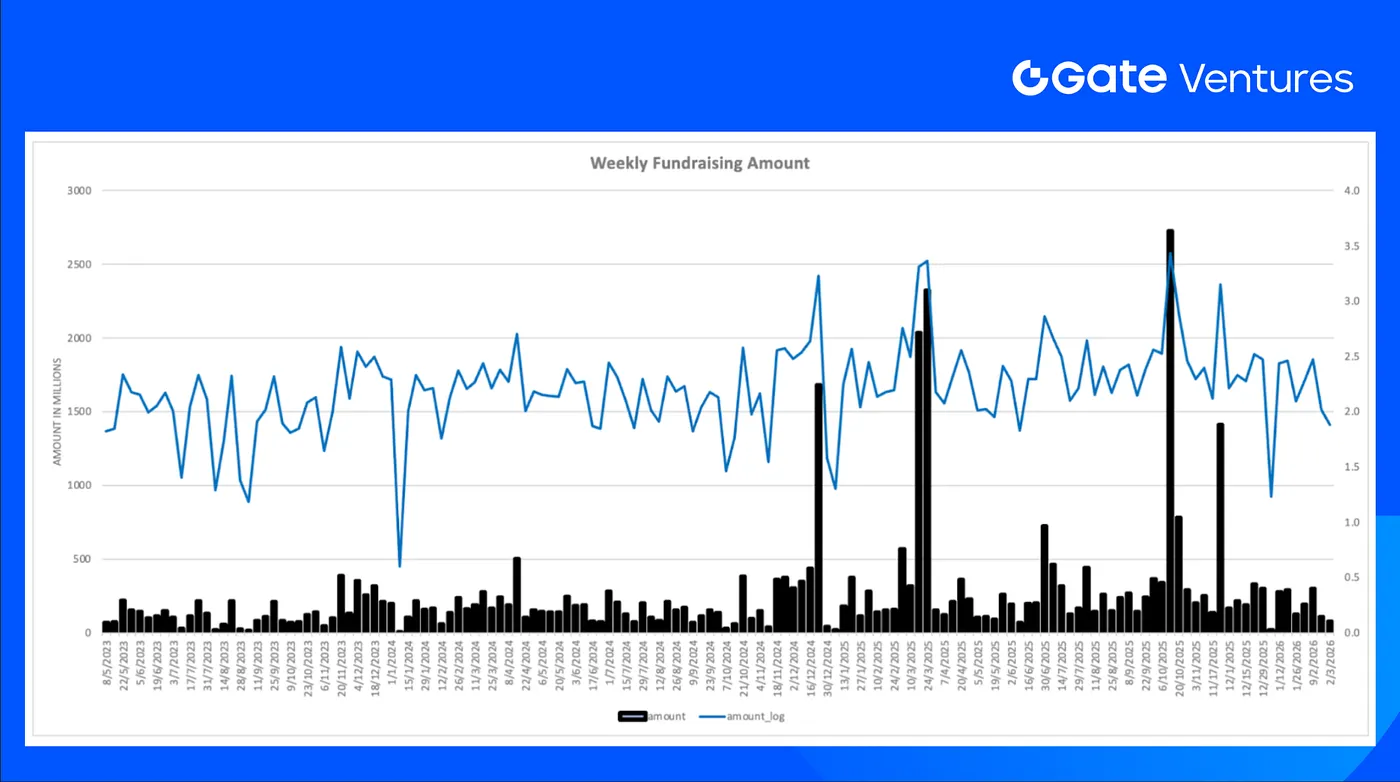

Total weekly fundraising declined to $76.15M for the first week of Mar-2026, a decrease of 27% compared to the week prior.

About Gate Ventures

Gate Ventures, the venture capital arm of Gate.com, is focused on investments in decentralized infrastructure, middleware, and applications that will reshape the world in the Web 3.0 age. Working with industry leaders across the globe, Gate Ventures helps promising teams and startups that possess the ideas a

Website: https://www.gate.com/ventures

The content herein does not constitute any offer, solicitation, or recommendation. You should always seek independent professional advice before making any investment decisions. Please note that Gate Ventures may restrict or prohibit the use of all or a portion of the services from restricted locations. For more information, please read its applicable user agreement.

Trump attempted to fire Federal Reserve Governor Lisa Cook, further challenging the independence of the Federal Reserve and influencing its decision-making process.

Gain access to proprietary analysis, investment theses, and deep dives into the projects shaping the future of digital assets, featuring the latest frontier technology analysis and ecosystem developments.

AIX9 is a next-generation CFO AI agent revolutionizing enterprise financial decision-making in cryptocurrency markets through advanced blockchain analytics and institutional intelligence. Launched in 2025, AIX9 operates across 18+ EVM-compatible chains, offering real-time DeFi protocol analysis, smart money flow tracking, and decentralized treasury management solutions. With over 58,000 holders and deployment on Gate, the platform addresses inefficiencies in institutional fund management and market intelligence gathering. AIX9's innovative architecture combines multi-chain data aggregation with AI-driven analytics to provide comprehensive market surveillance and risk assessment. This guide explores its technical foundation, market performance, ecosystem applications, and strategic roadmap for institutional crypto adoption. Whether you are navigating complex DeFi landscapes or seeking data-driven financial intelligence, AIX9 represents a transformative solution in the evolving crypto ecosystem.