AIG (American International Group) is a globally recognized insurance group. Its revenue comes not only from the sale of insurance products, but also from the returns generated by its large investment portfolio. For AIG, the key to keeping its business model stable over the long term lies in balancing underwriting profit and investment returns, while controlling claims risk and capital costs.

Understanding AIG’s revenue structure and profit logic helps investors see how the insurance industry operates. It also makes clear why risk management is one of the most important competitive capabilities for insurance companies.

AIG is the stock ticker for American International Group, which is listed on the New York Stock Exchange (NYSE). The company is headquartered in New York, United States, and is one of the world’s larger insurance and risk management groups.

From an industry classification perspective, AIG belongs to the insurance segment of the financial services industry. Its core businesses cover property insurance, liability insurance, commercial insurance, and specialized risk management services. Unlike traditional banks, which generate income through deposits and loans, an insurance company’s profit model is mainly built on premium income and investment returns.

AIG serves large enterprises, small and medium-sized businesses, and some individual clients. Its business spans many countries and regions. Because the insurance industry is closely tied to economic activity, AIG’s development is often affected by business investment, corporate operating conditions, and changes in global risk.

For investors following the insurance sector, AIG represents not only an insurance company, but also the broader development trend of the global corporate risk management market.

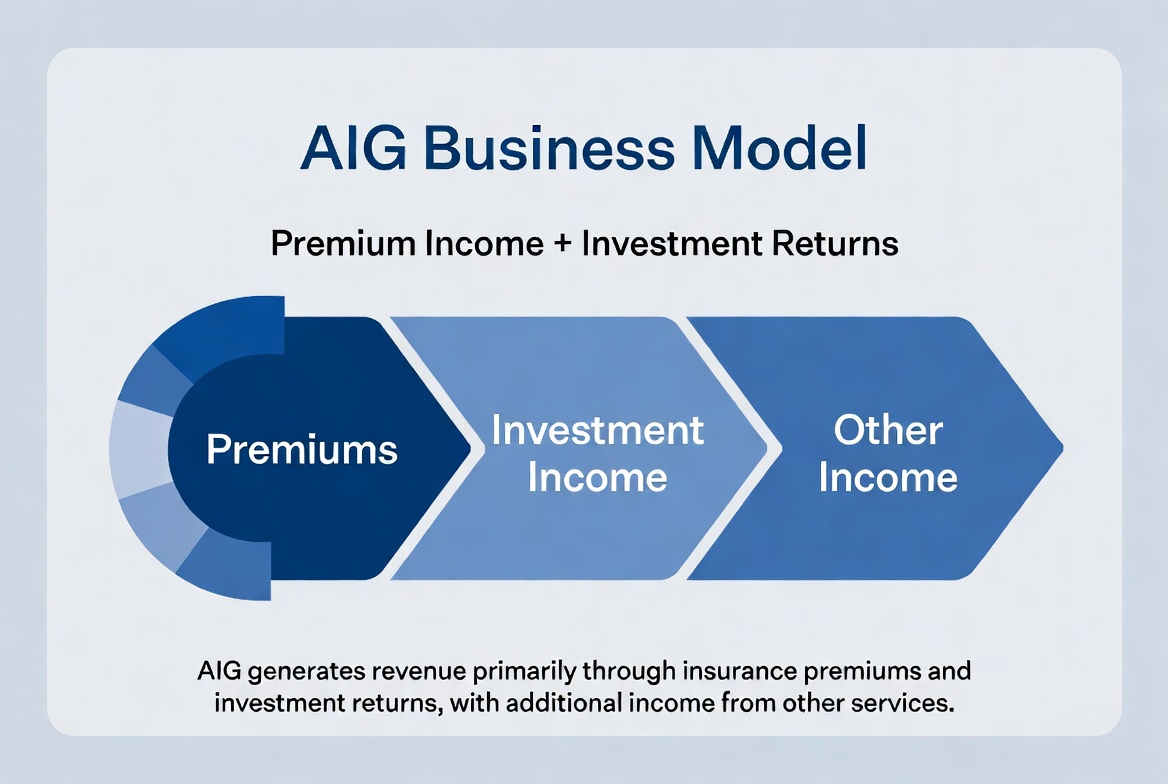

AIG’s Sources of Revenue

AIG’s revenue structure mainly consists of two parts: underwriting revenue and investment income.

The first source of revenue comes from selling insurance products. After customers purchase insurance, they pay premiums, and the insurance company underwrites the policy based on the results of its risk assessment. If claims expenses are lower than the premiums collected and operating costs, the company can generate underwriting profit.

The second source of revenue comes from investment income. After collecting premiums, insurance companies often do not pay claims immediately, which creates a large pool of investable funds. These funds are usually allocated to bonds, cash instruments, and other relatively stable financial assets, generating steady returns.

For large insurance groups, investment income can often have a significant impact on overall profitability. In this sense, insurance companies combine the roles of insurance operator and asset manager, and AIG is a typical example of this business model.

Below is a simplified structure of AIG’s revenue sources:

| Revenue Source |

Main Content |

| Premium income |

Property insurance, liability insurance, commercial insurance, etc. |

| Underwriting profit |

Premiums minus claims and operating costs |

| Investment income |

Returns from bonds, cash, and other investment assets |

| Other income |

Risk management and related service revenue |

How the Property Insurance Business Generates Revenue

Property insurance is one of AIG’s most important business segments and a major source of premium income.

Property insurance mainly protects buildings, factories, warehouses, equipment, and other assets. After a customer buys insurance, AIG calculates the premium based on the risk level, coverage scope, and historical loss experience, while assuming the corresponding claims obligations.

The core of this model is risk pricing capability. If an insurance company can accurately assess risk and set premiums reasonably, the premiums collected over the long term will usually exceed claims expenses and operating costs, creating underwriting profit.

For AIG, the property insurance business covers not only ordinary commercial assets, but also large industrial facilities, energy projects, and assets owned by multinational companies. Because these insurance projects are large in scale, they can generate considerable premium income for the company. At the same time, they also require stronger risk management capabilities.

As corporate asset scale grows and global risks become more complex, property insurance remains one of AIG’s core businesses for long-term development.

How Commercial Insurance Services Contribute to Growth

Compared with personal insurance, commercial insurance often involves larger premiums and more complex risk structures, making it an important source of growth for AIG.

Commercial insurance covers a very wide range of products, including liability insurance, cyber insurance, professional liability insurance, aviation insurance, and industry-specific insurance solutions. When companies conduct business operations, they often need these insurance products to reduce potential risks.

For example, a large manufacturing company may need to purchase property insurance, product liability insurance, and employee-related insurance at the same time. A technology company may pay more attention to cybersecurity and data risk protection. Together, these needs continue to drive expansion in the commercial insurance market.

AIG has long focused on the corporate client market, giving it strong advantages in risk assessment, underwriting capability, and international service networks. As corporate demand for risk management grows and global business activity increases, commercial insurance has also become an important driver of AIG’s revenue growth.

Why the Investment Portfolio Affects Profitability

Unlike many service companies, an insurer’s profitability depends not only on business sales, but also closely on investment management.

After customers pay premiums, an insurance company forms a large pool of funds that will be used for future claims. Before claims are paid, this pool is usually called insurance float. Insurance companies use these funds to invest in bonds, government bonds, and other low-risk assets to generate additional returns.

For AIG, the investment portfolio is very large, so the interest rate environment and financial market performance directly affect profitability. When market interest rates are higher, newly invested assets can usually generate higher returns. In a low-interest-rate environment, however, investment returns may be compressed.

For this reason, investment management has become an important part of the insurance industry. AIG not only needs to operate its insurance business well, but also needs to maintain a prudent investment strategy to balance long-term returns with capital security.

Why Risk Control Determines Long-Term Stability

Risk control is one of the most important competitive capabilities in the insurance industry. Even with substantial premium income, an insurance company may still face pressure on profitability if it cannot effectively control claims risk.

For AIG, risk control runs through the entire business process. From pre-underwriting risk assessment to policy pricing, claims management, and capital allocation, every step affects final operating results.

For example, rising natural disaster frequency may increase claims pressure in property insurance. More frequent cyberattacks may raise compensation costs for cyber insurance. Global economic volatility may affect corporate insurance demand and investment returns. Because of this, insurance companies must continuously update risk models and improve underwriting strategies.

In the long run, competition in the insurance industry is not simply about sales scale, but about risk management capability. Companies that can assess risk more accurately and control claims costs more effectively are more likely to maintain stable profitability. This is also an important source of AIG’s long-term competitiveness.

Summary

AIG (American International Group)’s business model is built on two foundations: premium income and investment returns. Through property insurance, commercial insurance, and specialized risk management services, the company generates steady premium income. Through investment management of insurance funds, it further creates investment returns. At the same time, risk control capability determines underwriting profit and long-term stability. For AIG, insurance is not merely a risk transfer business. It is also a business system built around risk assessment, capital management, and long-term asset operations.

FAQs

What does AIG mainly make money from?

AIG mainly earns revenue through premium income, underwriting profit, and investment returns.

What is premium income for an insurance company?

Premium income is the fee customers pay to an insurance company after purchasing insurance products. It is one of the most important sources of revenue for insurance companies.

Why is commercial insurance important to AIG?

Commercial insurance usually involves larger premiums and long-term customer relationships, making it one of AIG’s core growth businesses.

Where does an insurance company’s investment income come from?

It mainly comes from returns generated by bonds, government bonds, cash management instruments, and other investment assets.

What is insurance float?

Insurance float is the money an insurance company holds after collecting premiums and before paying claims. It can be used for investment management.

Why does risk control affect an insurance company’s profitability?

If claims expenses remain higher than premium income, the insurance company’s profitability will decline. That is why risk control is a core capability in insurance operations.