Summary

-

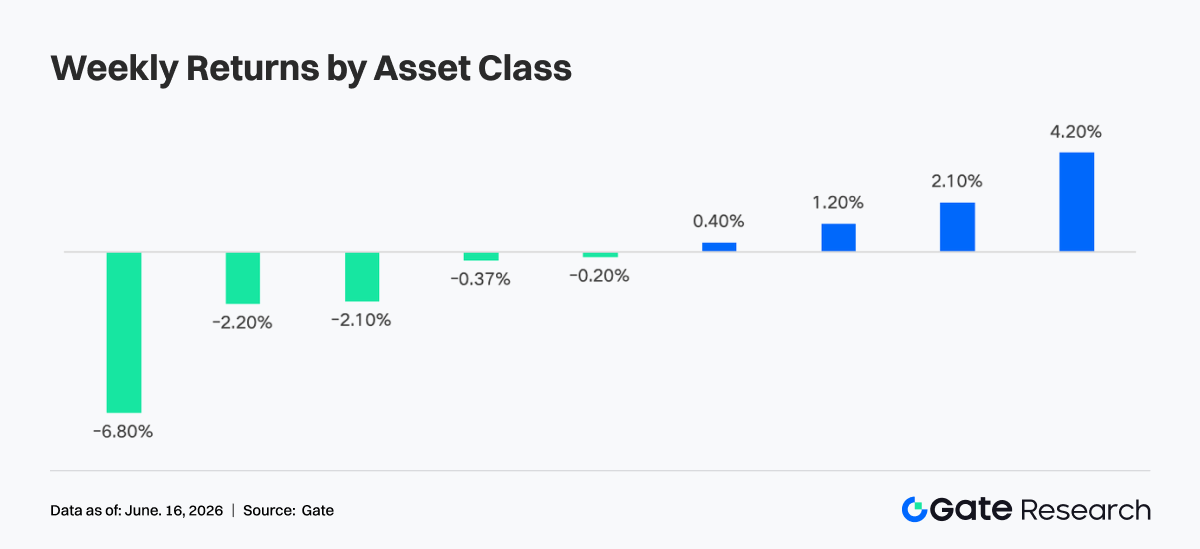

Last week, the market briefly turned risk-off due to higher-than-expected CPI data and Middle East geopolitical tensions. As risk assets rebounded, BTC, ETH, and the broader crypto market reversed higher, while ETF flows improved noticeably.

-

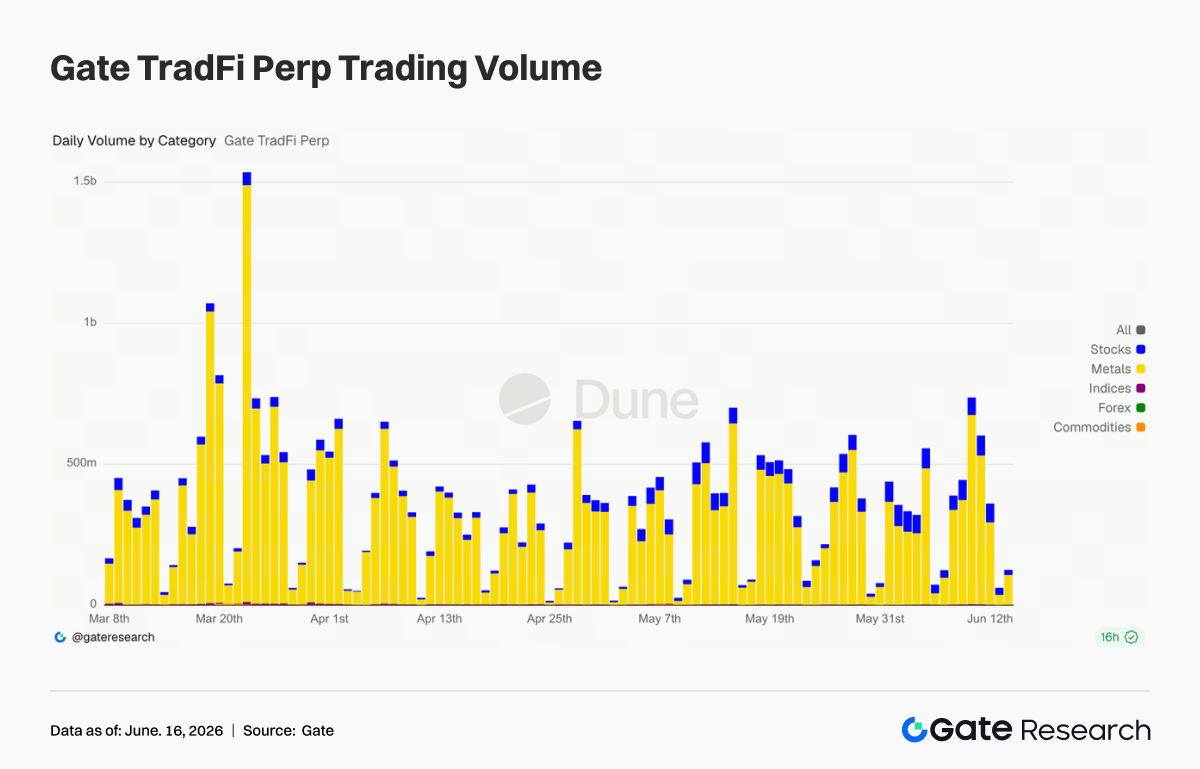

Gate TradFi Perp daily volume surpassed USD 500 million multiple times, peaking near USD 700 million around June 11. Trading activity shifted toward tech stocks, pre-IPO assets, and popular U.S. equities.

-

DEX volumes generally declined week-over-week, with major protocols such as Uniswap and PancakeSwap cooling from recent highs. Stablecoin supply continued to contract, suggesting the rebound was driven mainly by existing capital rotation rather than new inflows.

-

The LST sector recovered alongside ETH and SOL, with Solana-based staking assets outperforming. Aave lending activity also rebounded, with growth concentrated in Ethereum’s core market.

-

Aave borrowing rates remained low and USDC funding pressure eased, indicating limited leverage expansion. Protocol revenues normalized as the temporary boost from derivatives, MEV, and on-chain trading faded.

-

Derivatives markets recovered with BTC’s rebound. Leverage returned, hedging demand weakened, and both options volume and implied volatility declined, pointing to a more stable, lower-volatility environment.

-

Gate's institutional trading volume share increased by 7.5% month-over-month. BTC and ETH spot trading outperformed the broader market, with their combined market share across the platform rising 9.62% month-over-month. CrossEx trading volume grew 22.6% week-over-week, with support added for 37 new trading pairs.

1. Market Focus Analysis

Last week’s key macro event was the release of May CPI data on Wednesday. Headline CPI rose 4.2% YoY and core CPI increased 2.9% YoY, marking a third consecutive month of acceleration and reflecting the lagged impact of earlier energy price increases. The data triggered a sharp sell-off in U.S. equities, while Middle East tensions further boosted risk-off sentiment before gradually fading as markets stabilized.

From Thursday onward, sentiment recovered rapidly and risk assets staged a strong rebound. Crypto markets followed a similar pattern: BTC gained about 4.2% for the week, rebounding from a midweek low near $60,000 to finish above $65,000, while ETH rose roughly 2.1%, recovering from $1,604 to close near $1,726. Altcoins also rebounded, though performance varied. Total crypto market capitalization largely recovered its midweek losses, while the Fear & Greed Index rebounded from “Extreme Fear” territory but remained relatively weak.

On the Fed front, the policy outlook remains largely unchanged. Elevated inflation and resilient labor market data continue to support a higher-for-longer stance. However, Brent crude has fallen sharply over the past month, and softer core inflation suggests energy-driven inflationary pressures may be easing. The federal funds rate remains at 3.50%–3.75%, with markets assigning nearly a 99% probability that the Fed will leave rates unchanged at its June 16–17 meeting. While expectations for additional tightening later this year remain elevated, continued declines in energy prices and broader inflation could alter that outlook.

2. Liquidity Analysis

2.1 Market Sentiment Rebounds, BTC and ETH ETFs Reverse Outflow Trend

Last week, spot Bitcoin ETFs underwent a clear shift from early-week outflows to renewed inflows. On Monday, BlackRock’s IBIT recorded net outflows of approximately $233 million, contributing to total net outflows of about $91 million across Bitcoin ETFs and extending the previous week’s negative momentum. The turning point came on Wednesday, when IBIT posted its first net inflow of the week. As CPI-related concerns faded and market sentiment improved, Bitcoin ETFs attracted roughly $86 million in net inflows on Thursday, with all 12 U.S. spot Bitcoin ETFs reporting no net outflows for the day.

BlackRock’s IBIT remains the dominant product with over $70 billion in AUM, followed by Fidelity’s FBTC at roughly $17.7 billion. While ETF flows showed resilience after the sell-off, it remains unclear whether sustained inflows will develop into a longer-term trend.

Spot Ethereum ETFs outperformed Bitcoin ETFs over the week. While BTC ETFs experienced significant outflows early in the week, ETH ETFs attracted net inflows, highlighting a rotation of institutional capital rather than broad-based withdrawal from crypto markets. On Monday alone, Ethereum ETFs recorded approximately $82 million in net inflows, led by Fidelity’s FETH and BlackRock’s staking-enabled ETHB product.

Overall, Ethereum ETF flows remained positive throughout the week. Combined AUM across spot ETH ETFs now stands at approximately $21.5 billion, with staking-enabled products attracting particularly strong demand, reflecting growing institutional interest in Ethereum and its yield-generating ecosystem.

2.2 TradFi Liquidity

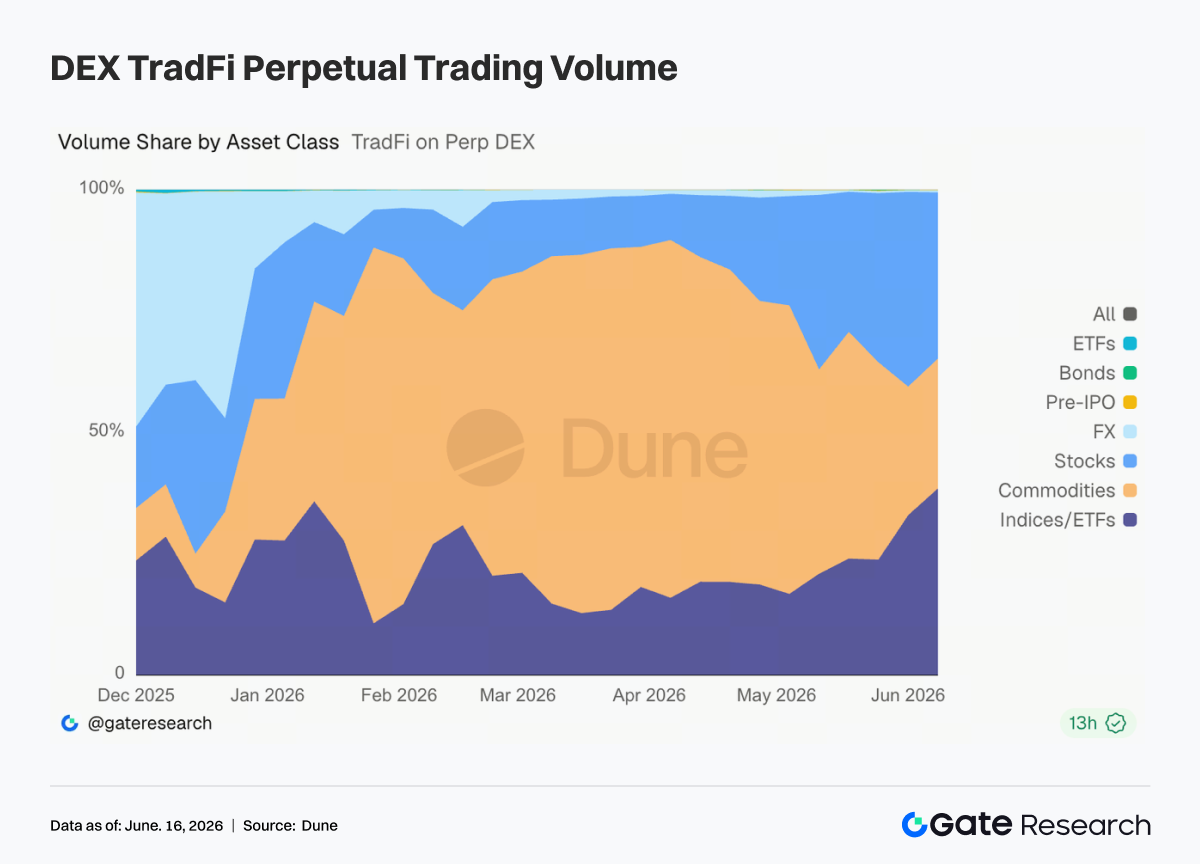

- TradFi Perp DEX: Trading activity continued to rotate away from commodities and toward equities and index/ETF products. Since mid-May, the commodity share of trading volume has fallen from nearly 70% to around 25%–35%, while equities have recovered to roughly 30% and index/ETF products have increased to 35%–40%, becoming the primary source of volume growth. This shift reflects changing market dynamics. Safe-haven demand linked to Middle East tensions pushed gold and other commodities higher before trading activity cooled, while continued enthusiasm around AI, semiconductor stocks, and major events such as SpaceX’s listing attracted capital back into U.S. equities and related index products. As a result, user demand on TradFi Perp platforms is expanding beyond gold trading toward a broader range of assets, including stocks, ETFs, and Pre-IPO opportunities.

- Gate TradFi Perp Volume: Trading activity remained strong over the past week, with daily volume exceeding $500 million on multiple occasions and peaking near $700 million around June 11. Precious metals continued to dominate overall trading volume, with gold-related products accounting for the majority of activity. Meanwhile, the share of stock trading increased, reflecting growing interest in technology stocks, Pre-IPO assets, and popular U.S. equities. Notably, despite cautious sentiment across the broader crypto market, TradFi Perp activity remained resilient, suggesting that some speculative capital is rotating from native crypto assets into traditional financial instruments such as gold, equities, and indices.

-

Gate TradFi U.S. Equities Offering: Gate officially launched its U.S. equities trading service on June 2. Supported by real underlying assets, USDT settlement, zero overnight holding fees, and deep liquidity, the product has gained steady market traction and trading volume growth since launch. Gate currently supports seven asset categories—ADRCs, stocks, ETFs, ETNs, ETSs, ETVs, and PFDs—and continues to expand its product coverage. The total number of tradable instruments has doubled since launch, with stocks showing the strongest growth and increasing from roughly 70% to 85% of all listed assets. Going forward, Gate plans to expand market access, integrate global liquidity, and enhance cross-market trading capabilities, further strengthening its position as a global multi-asset trading platform.

-

TradFi Order Book Depth: We analyzed order book depth (Delta) for XAUT, the most actively traded TradFi asset on the platform. Liquidity conditions showed a “weak-then-recover” pattern over the past week. Between June 10 and 12, escalating Middle East tensions and rising safe-haven demand led to a sharp contraction in order book depth, with Delta repeatedly falling below -$1 million, indicating significant order cancellations and tighter liquidity. As gold stabilized around $4,050 and rebounded, liquidity quickly returned after June 13. On June 14, Delta surged above +$2 million, reflecting a strong recovery in market-making activity. Overall, XAUT order book depth has improved significantly, providing stronger liquidity support for gold prices at elevated levels.

3. On-Chain Data Insights

3.1 DEX Volumes Cool Despite Market Rebound

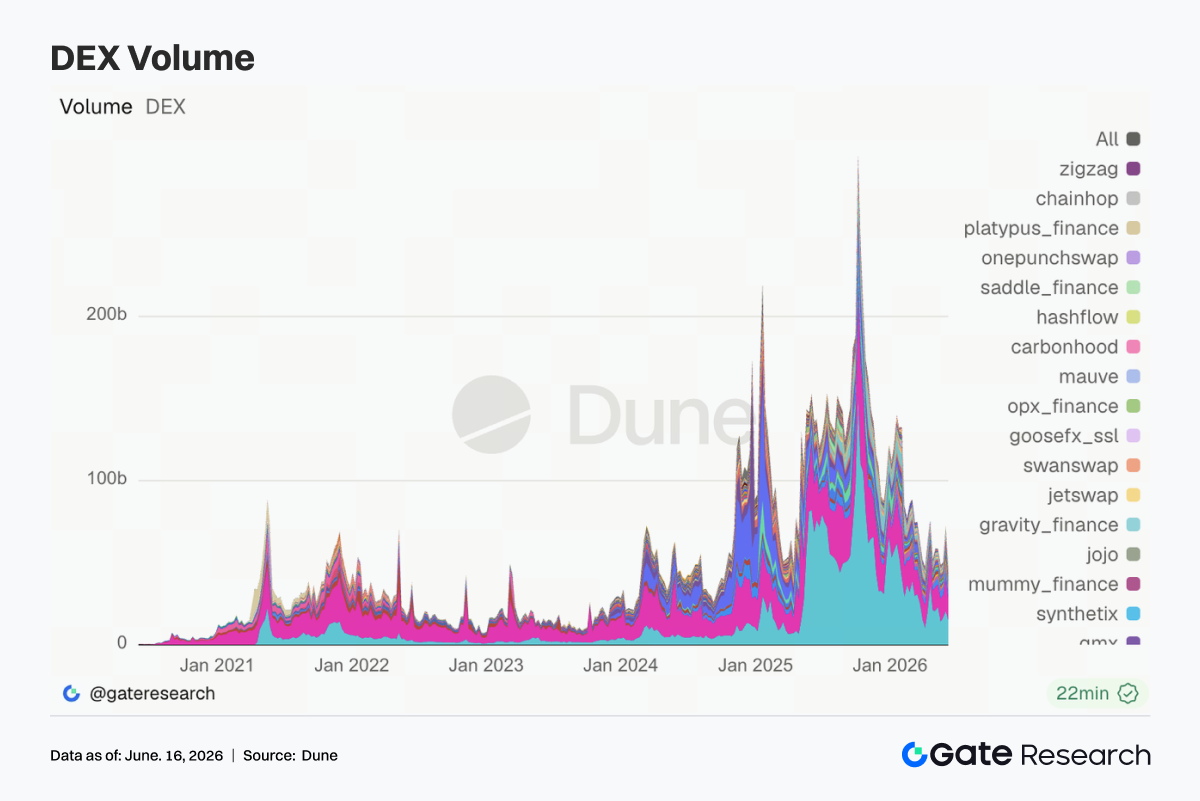

DEX trading activity declined noticeably from the previous week, with major protocols including Uniswap, PancakeSwap, Aerodrome, and Curve retreating from recent highs. While the market rebound initially boosted trading activity, momentum failed to sustain throughout the week. PancakeSwap regained the top position ahead of Uniswap, though the gap remained narrow, with liquidity concentrated in the BNB Chain and Ethereum ecosystems.

On Solana, Meteora, Raydium, and Whirlpool also saw lower volumes. Although PumpSwap maintained strong user activity, trading size did not grow proportionally, suggesting retail-driven, low-value transactions. Meanwhile, speculative capital increasingly rotated into technology IPOs, oil-related products, and on-chain equity perpetuals, reducing crypto’s dominance as the primary destination for risk-taking capital.

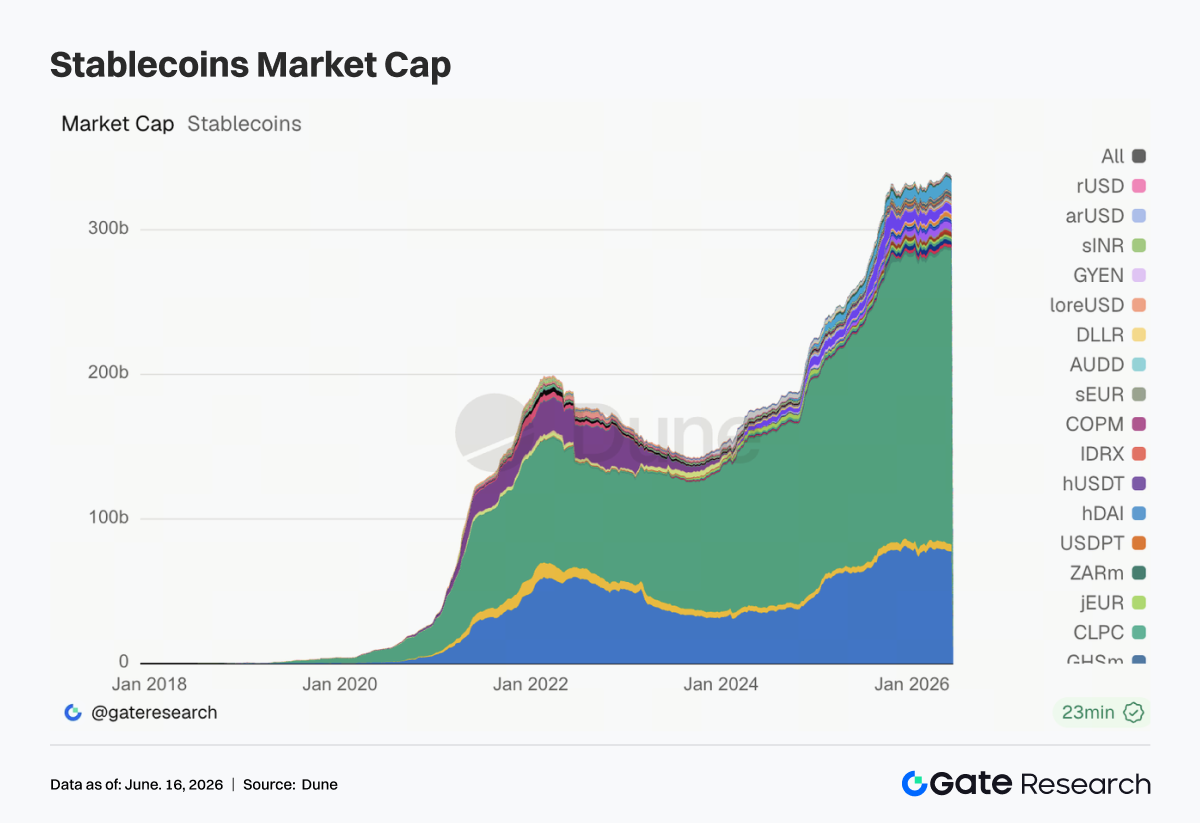

3.2 Stablecoin Supply Continues to Contract

Major stablecoin supplies generally declined this week. USDT and USDC recorded modest decreases, while USDS, USD1, DAI, and PYUSD saw more notable contractions. USDe remained broadly stable, while GHO was one of the few stablecoins to expand, supported by growing adoption of Aave’s native stablecoin.

The contraction in stablecoin supply aligns with weaker DEX trading activity, suggesting that recent market gains were largely driven by capital rotation rather than fresh liquidity entering the ecosystem. Notably, World Liberty Financial’s USD1 received significant publicity through a UFC fighter bonus program, but supply data has yet to reflect any meaningful growth. This highlights the market’s continued focus on utility, transparency, and liquidity rather than marketing exposure alone.

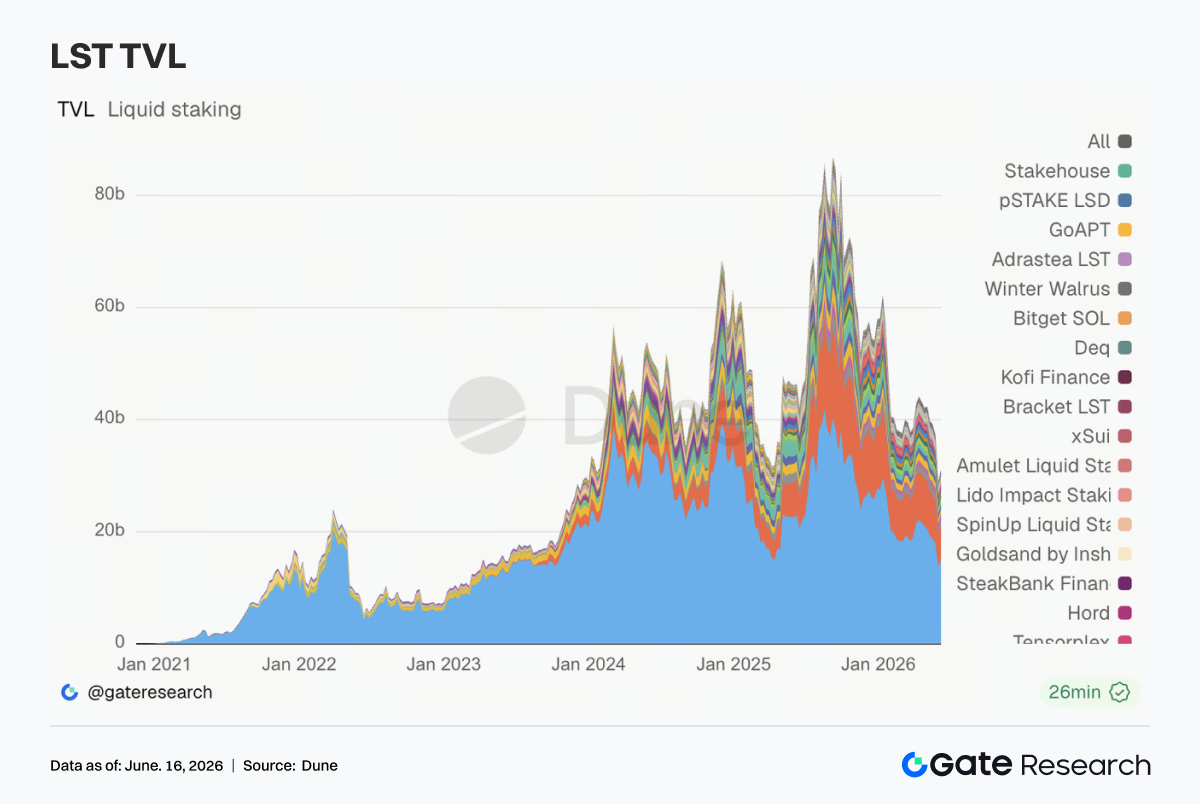

The LST sector rebounded this week after last week’s broad decline. Ethereum-based protocols such as Lido, Rocket Pool, and StakeWise posted modest recoveries, while staking capital remained largely stable.

Solana staking protocols showed stronger momentum, with Sanctum, Jito, and Jupiter Staked SOL recording larger TVL gains than their Ethereum counterparts. Sanctum was the strongest performer among major LST platforms. However, much of the TVL recovery was driven by higher ETH and SOL prices rather than substantial net inflows. The impact of the KelpDAO cross-chain incident continues to influence market sentiment, and institutions remain increasingly selective when evaluating standard LSTs, restaking products, and cross-chain staking assets. For now, the rebound appears to be more of a valuation recovery than the start of a new staking expansion cycle.

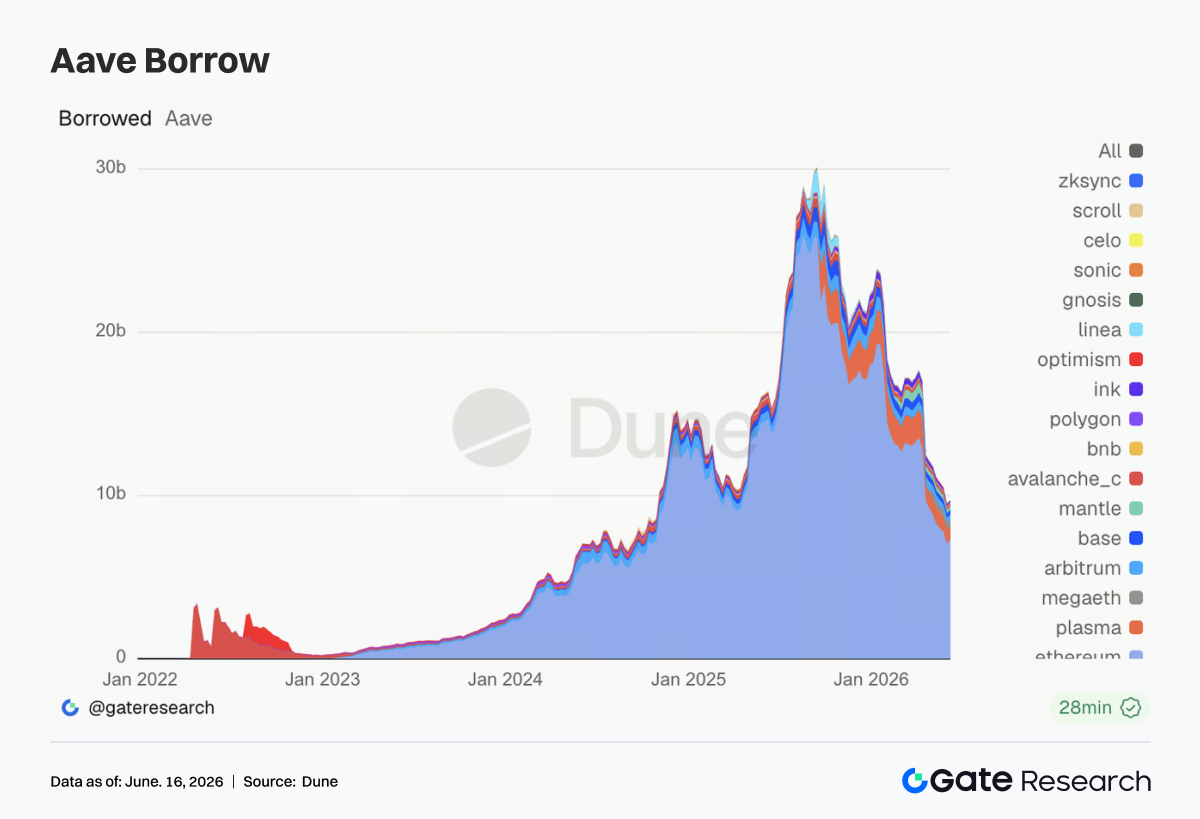

3.4 Ethereum Drives Aave Recovery While Multi-Chain Growth Remains Weak

Aave’s lending market stabilized after several weeks of contraction, with Ethereum accounting for most of the recovery. Base, Mantle, and BNB Chain saw modest improvements, while Plasma, MegaETH, Avalanche, and Ink continued to decline, with Ink experiencing the largest contraction.

Capital appears to be rotating back toward Ethereum, where collateral depth, liquidation liquidity, and risk parameters remain more predictable. Caution following the rsETH/KelpDAO incident has not fully faded, and the market continues to monitor risk mitigation measures and collateral management updates. In this context, Aave V4’s Hub-and-Spoke architecture becomes increasingly relevant by helping isolate risk across markets. While lending activity has likely reached a short-term bottom, current growth remains concentrated in core Ethereum markets.

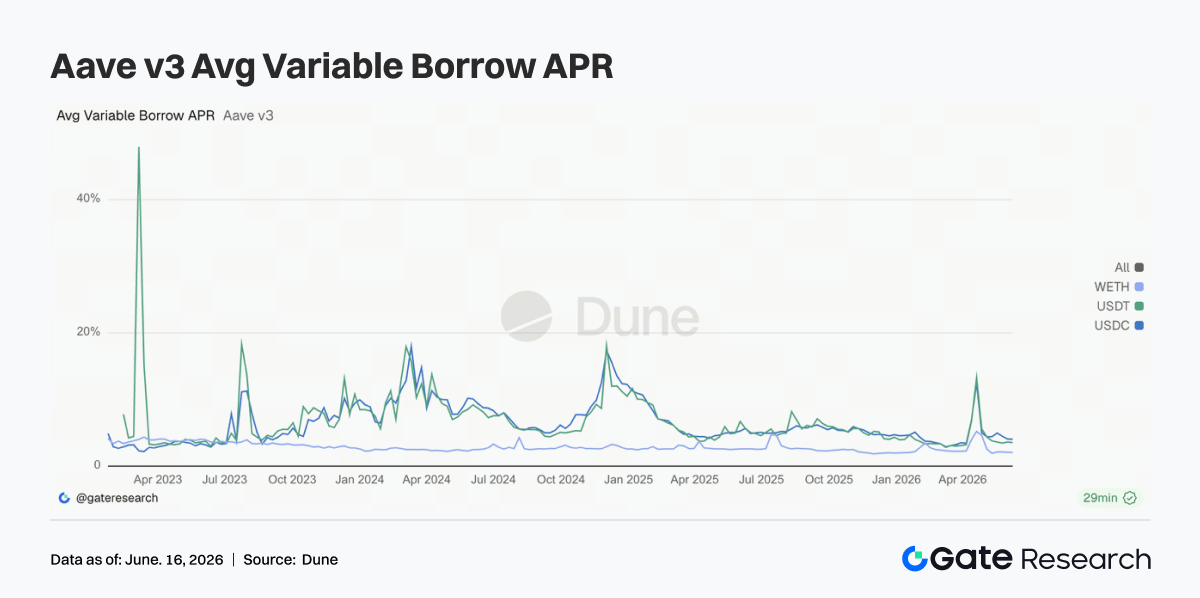

3.5 Borrowing Rates Remain Stable, USDC Funding Pressure Eases

Average borrowing rates for USDC, USDT, and WETH remained largely stable throughout the week. USDC and WETH rates edged lower, while USDT traded within a narrow range. Peak USDC borrowing costs also declined compared with the previous week, indicating easing liquidity stress and fewer episodes of extreme utilization.

WETH borrowing costs remained subdued despite a recovery in lending balances, suggesting that leveraged ETH positioning remains relatively conservative. Although USDC borrowing costs continue to exceed those of USDT, demand remains concentrated in highly liquid, institutionally accepted assets. Current market conditions remain supportive for liquidity management, carry trades, and market-neutral strategies, but do not yet indicate aggressive leverage expansion. Overall, rate dynamics suggest that Aave has moved beyond its post-incident stress phase, although broader risk appetite remains subdued.

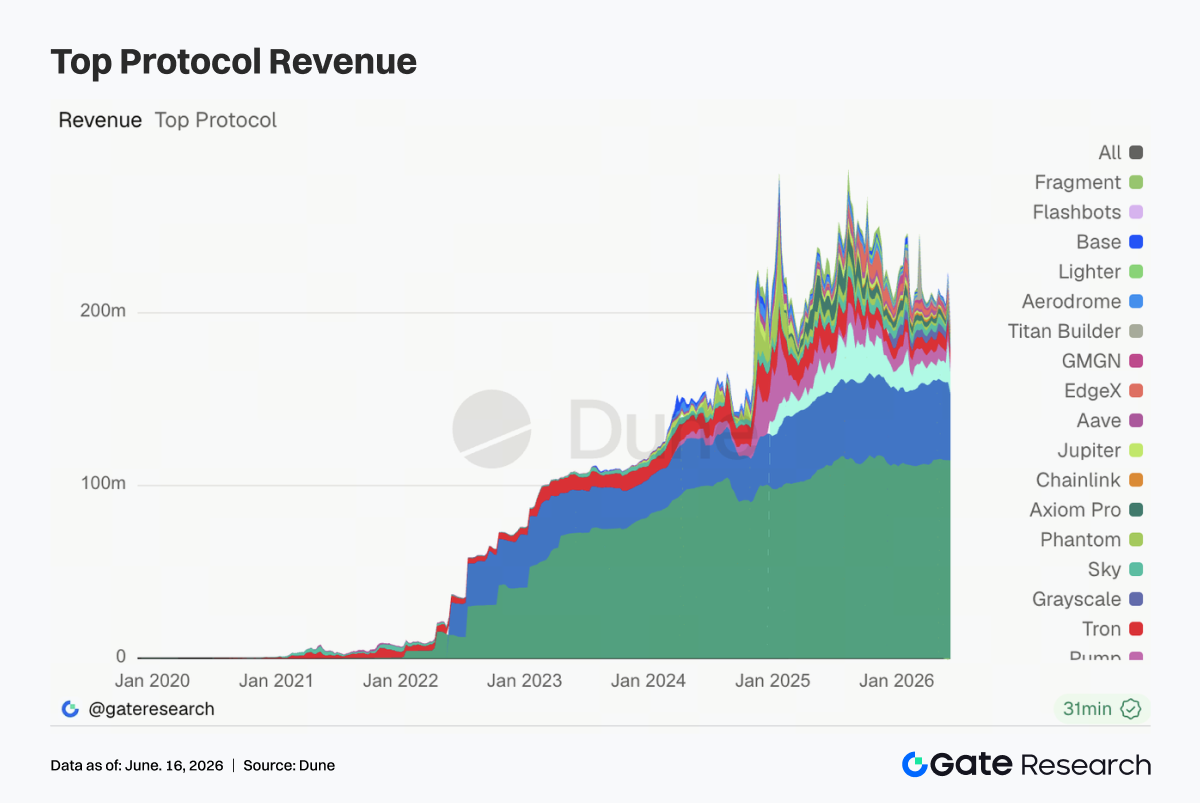

3.6 Protocol Revenues Normalize as Trading Frenzy Fades

Most major protocols generated lower revenues this week, reflecting a broad normalization after last week’s surge in activity. Tether and Circle remained the largest revenue generators, supported by their scale and reserve-based business models, although reserve income also softened.

Hyperliquid Perps experienced a significant revenue decline from the previous week’s peak but remained the highest-earning on-chain trading protocol. The slowdown coincided with fading enthusiasm around equity index, oil, and Pre-IPO perpetual contracts. Aave revenues also declined despite improving lending balances, as lower borrowing rates and moderate utilization limited revenue growth.

Revenue across infrastructure and trading-related protocols—including Titan Builder, Base, edgeX, and Aerodrome—also fell, indicating that the recent boost from order flow, MEV activity, and derivatives trading was temporary. Overall, the industry’s revenue mix has returned to a more typical structure: stablecoins providing a steady base, derivatives contributing cyclical upside, and lending protocols generating stable spread income.

4. Derivatives Tracking

4.1 BTC Price and Open Interest Recover Together

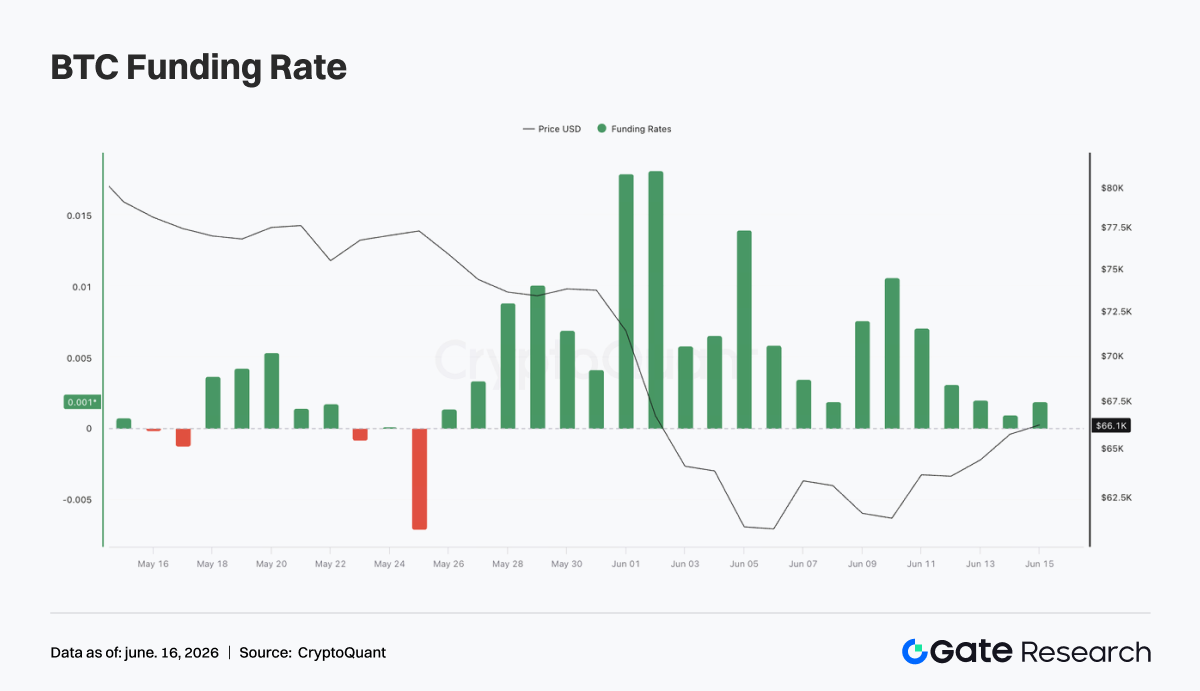

BTC briefly fell to around $62K early in the week before rebounding to the $65K–66K range. During the recovery, open interest (OI) increased from roughly $22B to above $23B, indicating that leveraged traders were re-entering the market and adding new positions.

Funding rates remained positive throughout the week, peaking around June 9–10 as long positioning accelerated during the initial rebound. Rates later moderated toward neutral-positive levels, suggesting reduced crowding on the long side. The combination of rising prices, increasing OI, and positive funding rates points to a shift from last week’s deleveraging phase toward a period of leverage rebuilding. While leverage remains below previous highs, continued increases in OI and funding without a decisive break above $66K could signal growing long-side positioning risks.

4.2 Options Volume Cools as Monthly Contracts Remain Dominant

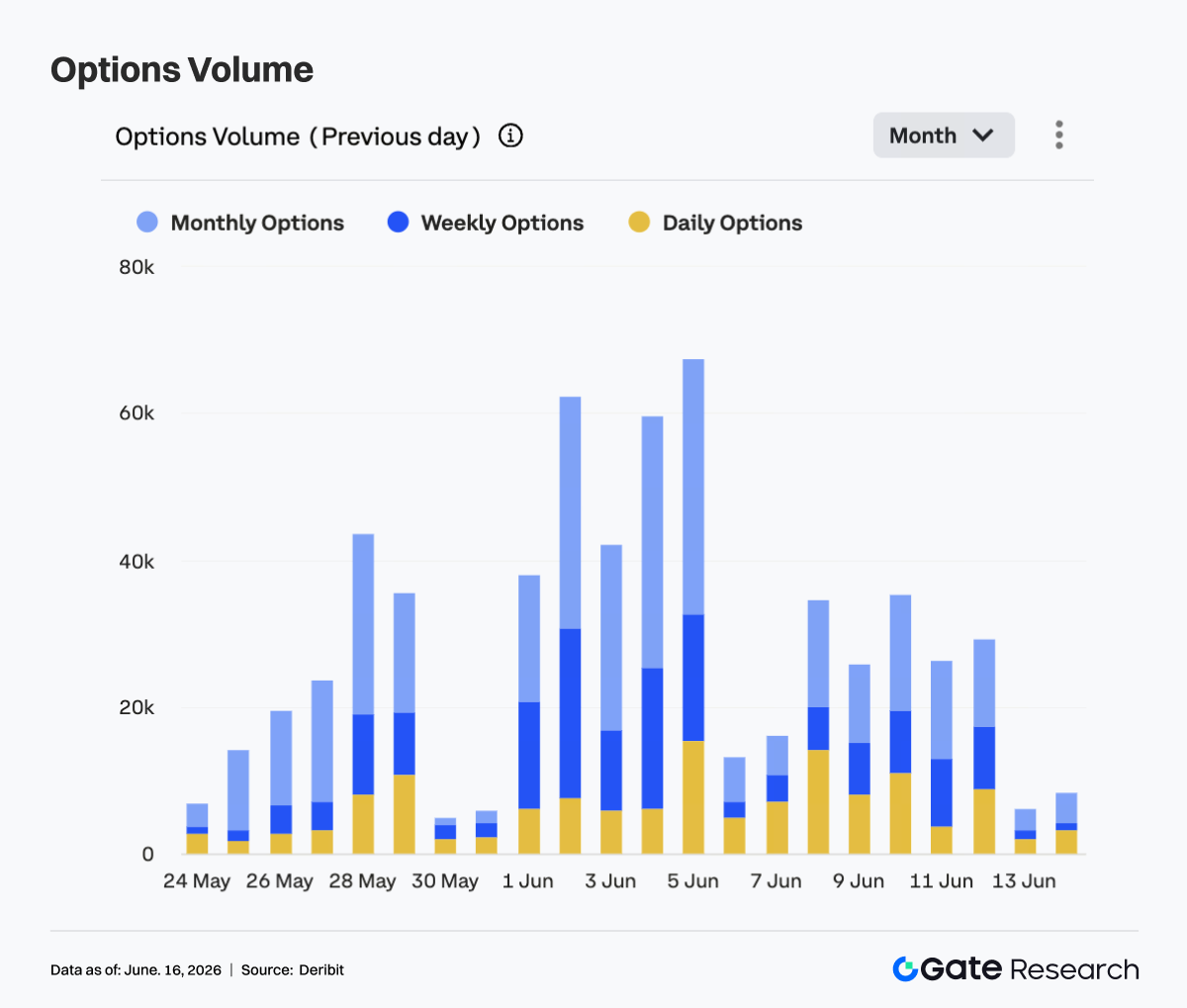

BTC options trading volume declined noticeably compared with the previous week. Daily volume peaked around 35K contracts on June 8 and June 10, while most trading days saw volumes in the 25K–30K range before dropping sharply over the weekend.

Monthly contracts continued to dominate activity, indicating that market participants remained focused on medium-term positioning and risk management rather than short-term speculation. The decline in options volume alongside BTC’s price stabilization suggests that panic hedging and large-scale portfolio repositioning have largely subsided. Overall, the market has shifted toward a “price recovery, lower activity, and medium-term positioning” environment. A sustained move above $66K would likely be required to reignite directional options trading.

4.3 25D Skew Rebounds as Demand for Downside Protection Fades

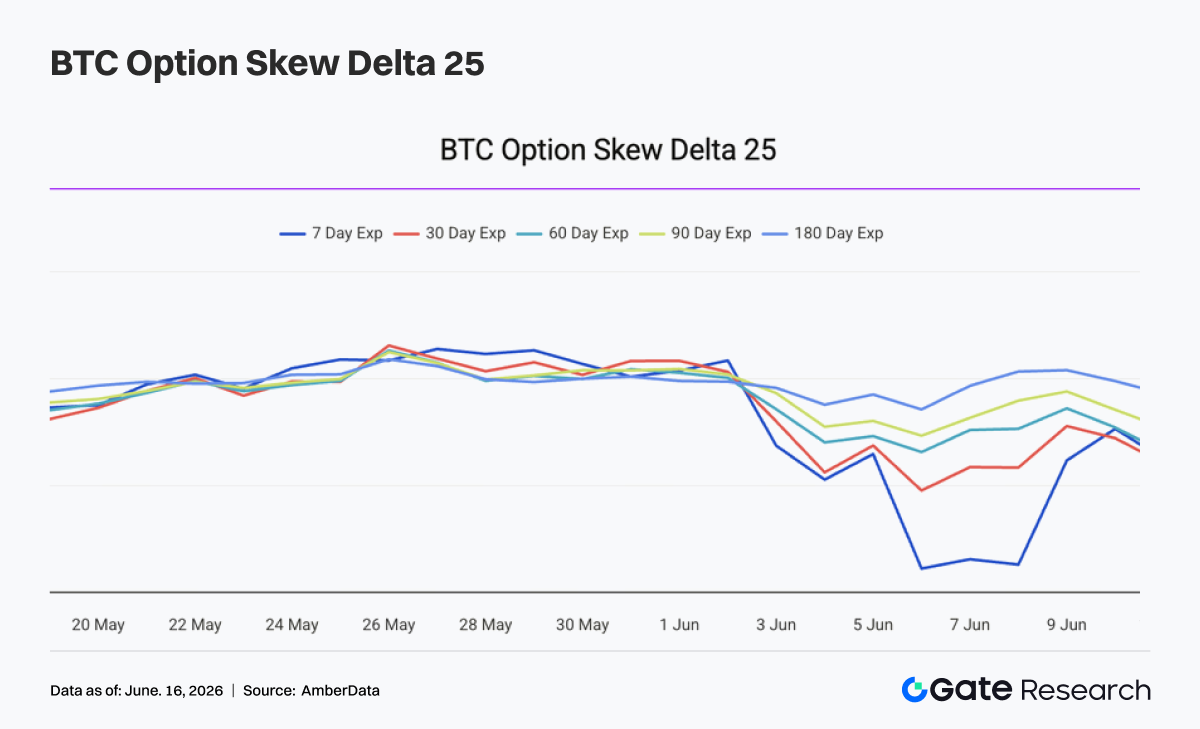

BTC 25D Skew recovered significantly across all maturities last week. Early in the week, the market remained defensive, with 7-day Skew approaching -14 and 30-day Skew near -9, reflecting elevated demand for put options and downside protection.

As BTC rebounded from roughly $62K to $65K–66K, Skew levels recovered rapidly. By June 12, 7-day Skew had improved to around -3.5, while 30-day, 60-day, and 90-day Skew rose into the -5 to -6 range. The sharper recovery in short-dated Skew suggests that near-term fear dissipated quickly as prices stabilized.

Although Skew remains negative across maturities, indicating ongoing demand for protection, the options market has clearly moved away from the extreme defensive positioning seen earlier. Further stabilization above $66K could push Skew closer to neutral levels, while a move back below $63K may revive hedging demand.

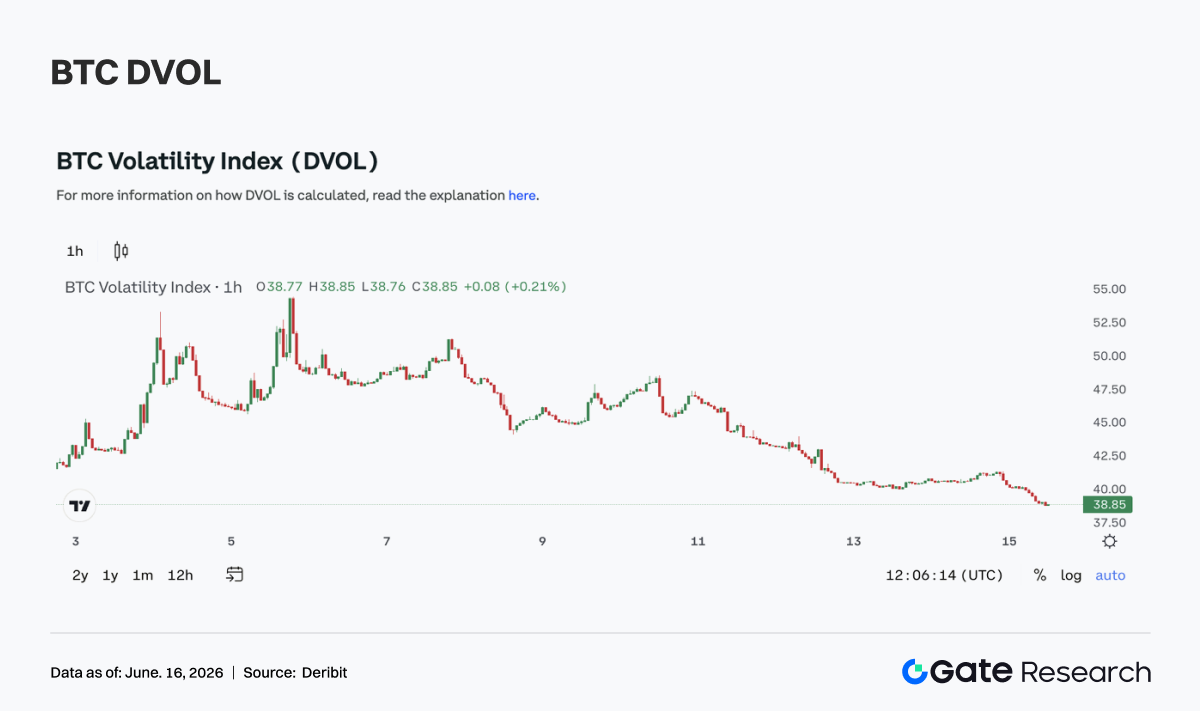

4.4 DVOL Declines as Volatility Expectations Normalize

BTC’s volatility index (DVOL) trended lower throughout the week. The index began in the 47–49 range, reflecting lingering risk premiums from the previous week’s sharp sell-off. As BTC stabilized and recovered, implied volatility steadily compressed.

Although DVOL briefly rebounded to around 48 on June 10, the move proved short-lived. The index subsequently fell to roughly 41 by June 12 and approached 40 by the weekend. The decline in DVOL coincided with lower options volume, improving Skew, and BTC’s price recovery, all pointing to a significant reduction in expectations for near-term market turbulence.

Overall, the derivatives market has transitioned from a high-volatility, defensive environment toward a more stable phase characterized by price recovery and volatility compression. If BTC continues trading within the $63K–66K range, volatility is likely to remain subdued, though a breakout from this range could trigger renewed volatility expansion.

5. Outlook

6. Gate Institutional Updates

Strong Trading Performance, Consistently Outperforming the Market

-

Spot and derivatives trading performance continued to outperform the broader market, with the share of institutional trading volume increasing by 7.5% month-over-month.

-

BTC and ETH spot trading outperformed the market, with their combined share of total platform spot volume rising 9.62% month-over-month.

-

Trading activity in long-tail altcoins remained robust, continuing to contribute to market share growth.

-

The institutional client mix continued to improve, with multiple quantitative trading firms and market makers steadily increasing their trading volumes.

Continued Growth of the CrossEx Ecosystem

-

CrossEx trading volume increased 22.6% week-over-week, reflecting sustained growth in cross-exchange trading demand.

-

The new CrossEx Colo Service was launched, further reducing latency for cross-venue trading.

-

Support for 37 additional trading pairs was added, bringing coverage to 6 major exchanges and 5,836 trading pairs.

Ongoing Optimization of Technology and Infrastructure

-

Official launch of the Delta-Neutral Strategy Mode, designed specifically for traders running funding-rate arbitrage, basis trading, and other delta-neutral strategies.

-

Continued enhancements to order-processing capabilities and system stability, with the latest version delivering a 30% performance improvement.

Data Sources:

- Investing, https://investing.com/currencies/xau-usd-historical-data

- Gate, https://www.gate.com/trade/BTC_USDT

- CMC, https://coinmarketcap.com/real-world-assets/?type=all-tokens

- Coinglass, https://www.coinglass.com/pro/depth-delta

- Dune, https://dune.com/gateresearch/gate-tradfi#weekly-volume

- Dune, https://dune.com/gateresearch/gate-institutional-weekly-report

- Bybit, https://www.bybit.com/future-activity/en/tradfi

- Bitget, https://www.bitgettradfi.com/tradfi/XAUUSD

- CryptoQuant, https://cryptoquant.com/asset/btc/chart/derivatives

- Amberdata, https://pro.amberdata.io/options/deribit/btc/current/

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.