Summary

- Among various LLM trading frameworks, the Multi-Agent architecture is closer to the research and trading workflow of real financial institutions than using a single LLM to directly generate buy and sell signals.

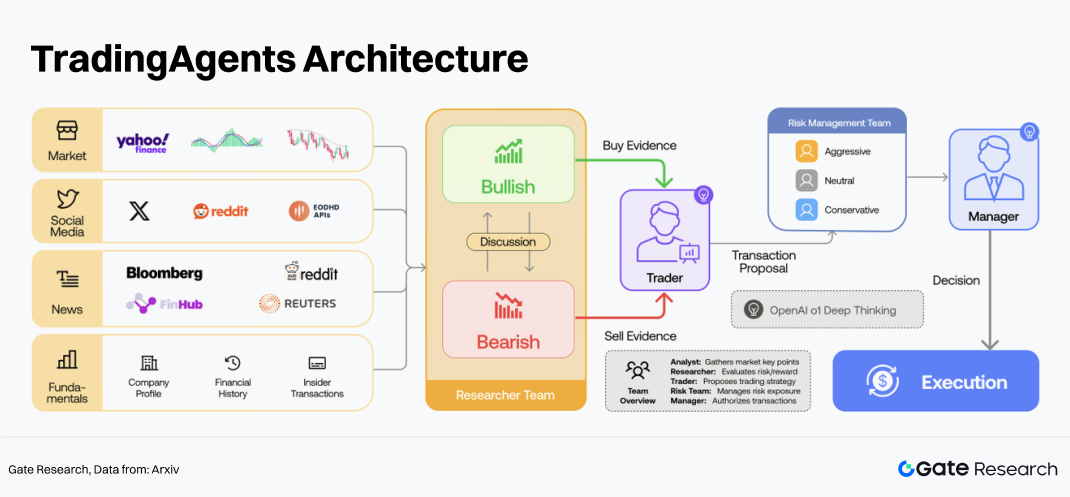

- TradingAgents is a financial trading framework based on Multi-Agent LLMs. Its core idea is to simulate the organizational structure of a real trading firm and decompose complex trading decisions into collaboration among multiple specialized roles.

- Experiments in the original paper showed that TradingAgents outperformed multiple traditional baseline strategies in stock market backtesting, improving cumulative returns, Sharpe ratio, and maximum drawdown.

- TradingAgents-BTC achieved a total return of +20.25% during the testing period, significantly outperforming the contemporaneous Buy and Hold return of -7.89%, indicating that the framework possesses a certain degree of active market timing capability under specific market conditions.

- The current backtesting period only covers about three months, resulting in a relatively short sample period. In addition, 1-hour frequency trading may be affected by transaction fees, slippage, and signal delays. Future work should further validate the strategy’s stability under longer time periods and different market environments.

1. Introduction

In recent years, an increasing number of studies have explored how to apply LLMs to financial trading scenarios. Although related research has not yet formed mature standardized products, academia has already proposed multiple directions, including LLM-based financial analysis assistants, trading bots, trading agents with memory mechanisms, LLM trading models combined with reinforcement learning, and multi-agent collaborative trading frameworks.

Compared with using a single LLM to directly generate buy and sell signals, the Multi-Agent architecture is closer to the research and trading workflow of real financial institutions. It can decompose trading tasks into multiple roles, such as technical analysts, news analysts, sentiment analysts, researchers, traders, and risk managers. Different agents process different information sources and form final decisions through debate, summarization, and risk review. This structure helps reduce the cognitive burden on a single model while also improving the transparency and interpretability of the decision-making process.

TradingAgents, proposed by Yijia Xiao et al., is a representative work in this direction. The framework simulates the organizational structure of a real trading company and establishes multiple roles. The system first has analysts collect and analyze market information, then researchers conduct bullish and bearish debates, after which traders generate trading decisions, and finally the risk management team and fund manager perform risk review and execution confirmation. Experiments in the original paper showed that TradingAgents outperformed multiple traditional baseline strategies in stock market backtesting, improving cumulative returns, Sharpe ratio, and maximum drawdown.

However, the original TradingAgents experiments mainly focused on the stock market, and its applicability to the crypto asset market still needs validation. Therefore, migrating TradingAgents to the BTC market has certain research value. This paper constructs a BTC trading backtesting experiment based on TradingAgents to explore the effectiveness of the Multi-Agent trading framework in the crypto market.

2. Overview of the TradingAgents Architecture

TradingAgents is a financial trading framework based on Multi-Agent LLMs. Inspired by the organizational structure of real companies, TradingAgents defines four categories of agent roles within a simulated trading company: analysts, researchers, traders, risk management, and fund managers. Each agent is assigned a specific name, role, objective, and constraint, while also possessing predefined context, skills, and tools matching its function.

2.1 Analyst Team

The original TradingAgents framework mainly includes four types of analysts:

- Fundamental Analyst: Responsible for analyzing corporate financial conditions, profitability, valuation levels, financial statements, earnings reports, and insider trading information. The objective is to determine the long-term investment value of an asset and identify whether it is undervalued or overvalued.

- Sentiment Analyst: Responsible for analyzing social media, investor comments, public discussions, and market sentiment indicators. The objective is to identify changes in investor sentiment and determine whether such sentiment may influence asset prices in the short term.

- News Analyst: Responsible for analyzing news events, corporate announcements, policy changes, and macroeconomic events. The objective is to identify important information that may affect market trends and assess its short-term or medium-term impact.

- Technical Analyst: Responsible for analyzing prices, trading volume, and technical indicators such as MACD, RSI, Bollinger Bands, moving averages, and volatility indicators. The objective is to determine market trends, momentum strength, overbought/oversold conditions, and potential trading points.

2.2 Research Team

The research team in TradingAgents usually consists of two agents with opposing views:

- Bullish Researcher: Interprets market information from a positive perspective, emphasizing bullish logic, growth potential, favorable factors, and reasons to buy.

- Bearish Researcher: Interprets market information from a cautious or negative perspective, emphasizing downside risks, valuation pressure, market uncertainty, and potential bearish factors.

The two researchers conduct multiple rounds of debate around analyst reports. After the debate ends, the system summarizes both sides’ opinions and forms a relatively balanced market judgment. The significance of this mechanism lies in introducing adversarial viewpoints.

2.3 Trader

The trader integrates structured reports from the analyst team, researcher viewpoints, and the current market state to generate preliminary trading decisions (Buy/Sell/Hold). At the same time, the trader also provides trading rationale, confidence level, and potential risks. Its output includes not only action signals but also natural language explanations. This makes TradingAgents easier to review and debug compared with traditional black-box models.

2.4 Risk Management Team

The risk management team usually contains three types of agents with different risk preferences:

- Aggressive Risk Manager: Focuses on high-return opportunities and tends to accept higher risks under favorable conditions.

- Neutral Risk Manager: Maintains balance between return and risk, focusing on whether the strategy has a reasonable risk-reward ratio.

- Conservative Risk Manager: Prioritizes controlling drawdowns and extreme risks, tending to reduce positions or avoid highly uncertain trades.

The risk management team discusses whether the trader’s decision is reasonable, including whether current positions are too large, whether market volatility is excessively high, whether there are event risks, and whether trading size should be reduced. After risk review, the system may maintain the original recommendation or adjust positions and trading actions.

2.5 Fund Manager and Final Decision

The fund manager serves as the final decision confirmation role in TradingAgents. The fund manager reviews the discussions from the risk management team and determines whether to approve the trader’s recommendation. Its role is similar to the final approver in real trading institutions, responsible for making the final trade-off between profit opportunities and risk control.

3. Crypto Trading Framework Based on TradingAgents

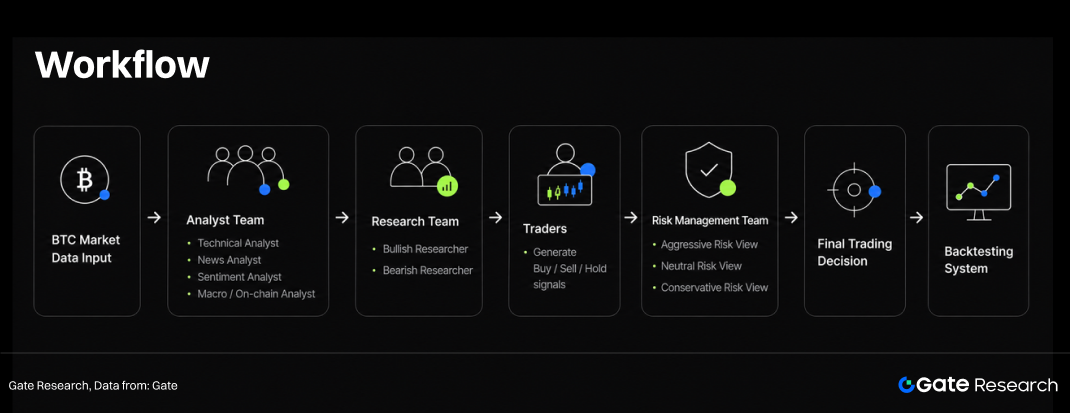

The crypto market is also influenced by multiple information sources, including price trends, trading volume, news, macro policies, on-chain fund flows, and market sentiment. Therefore, while retaining the core workflow of TradingAgents, this paper modifies the analyst roles into technical analysts, news analysts, sentiment analysts, and macro/on-chain analysts that are more suitable for the crypto market, and evaluates the framework’s performance in BTC backtesting.

3.1 Overall Framework

The framework first inputs crypto market data. The analyst team then conducts analysis from technical, news, sentiment, and macro/on-chain perspectives. Subsequently, the research team carries out bullish and bearish discussions based on the analysis results. The trader synthesizes all viewpoints to generate Buy, Sell, or Hold signals. Afterwards, the risk management team reviews the trading recommendation from aggressive, neutral, and conservative risk perspectives. Finally, the trading decision is entered into the backtesting system to evaluate strategy performance.

3.2 Agent Role Design

Technical Analyst: Analyzes token price trends, trading volume, and technical indicators including MA, EMA, MACD, RSI, Bollinger Bands, ATR, and ADX. Outputs include trend judgment, momentum strength, volatility level, overbought/oversold conditions, and key support/resistance levels.

News Analyst: Analyzes news events related to the token, such as ETF fund flows, regulatory policies, exchange incidents, institutional holdings changes, macroeconomic data, and geopolitical risks. Outputs include news summaries, bullish/bearish judgments, and potential impact duration.

Sentiment Analyst: Analyzes market sentiment, including social media discussions, news sentiment, Fear & Greed Index, and community popularity. The focus is determining whether the market is in a FOMO, panic, overheated, or neutral state.

Macro + On-Chain Analyst: Focuses on active addresses, exchange net inflows/outflows, long-term holder behavior, miner balances, stablecoin supply, BTC dominance, the US Dollar Index, and US Treasury yields. The objective is to capture changes in token capital flows and macro liquidity.

Researchers: The bullish researcher builds bullish logic based on all analyst reports, emphasizing favorable factors and potential breakout opportunities. The bearish researcher builds bearish logic, emphasizing drawdown risks, market overheating, macro pressure, or on-chain selling pressure. The two form a more balanced market judgment through debate. The trader integrates analyst reports and researcher debate results to output final trading signals, including Buy, Sell, or Hold, together with confidence level, position suggestions, and trading rationale.

Risk Management Team: Reviews trader decisions. The aggressive perspective focuses on profit opportunities, the neutral perspective balances return and risk, and the conservative perspective prioritizes drawdown control. Final decisions are adjusted by the risk team before entering backtesting execution.

4. Data and Experimental Design

Base Model: ChatGPT 5.5

Research Object: BTC/USDT

Backtesting Period: February 1, 2026 to May 1, 2026, consistent with the three-month backtesting setup in the original TradingAgents paper.

Data Frequency: 1-hour data

Data Source: Experimental data was obtained through Gate MCP, including BTC/USDT price data, technical indicator data, news data, social media or sentiment data, Fear & Greed Index, ETF inflows and outflows, nonfarm payroll data, US Treasury yields, CPI, and interest rate decisions. To avoid look-ahead bias, only data publicly available before each trading day could be used.

Trading Rules: The system generates one trading decision per day. Basic trading rules are as follows:

- Trading Type: Market orders, with three possible actions: Buy/Sell/Hold

- Positioning: No leverage is used; positions are either 0% or 100%

- Transaction Fee: 0.1%

- Slippage: 0.05%–0.1%

- Baseline Strategy: Buy and Hold, holding BTC throughout the entire period.

5. Backtesting Results

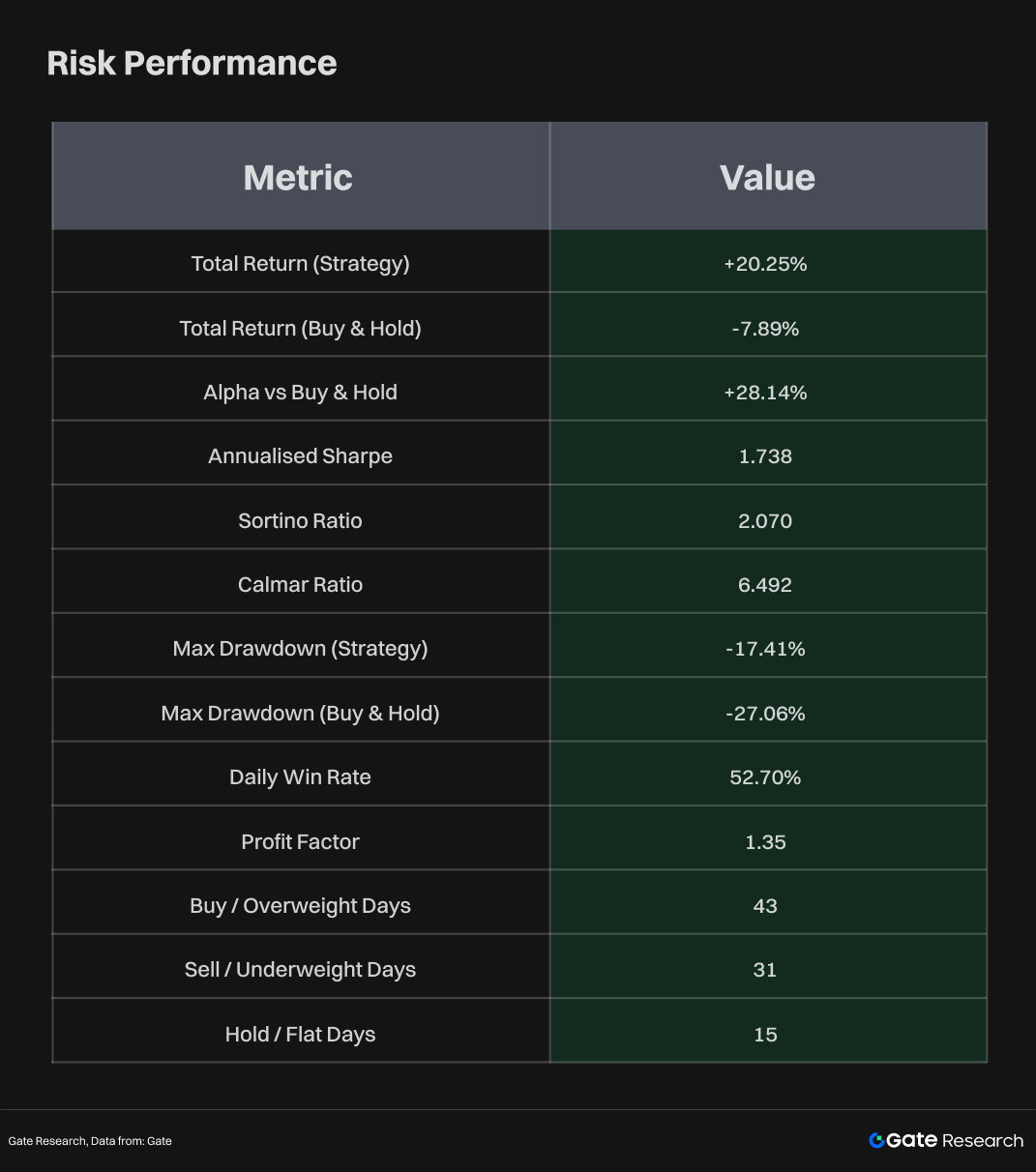

From the backtesting results, the strategy achieved a total return of +20.25%, while the Buy and Hold return during the same period was -7.89%, generating +28.14% alpha relative to Buy & Hold. This indicates that during the testing period, the strategy not only avoided losses suffered by simply holding BTC during declining and sideways markets, but also captured part of the rebound profits through switching between bullish and bearish positions.

From the equity curve, Buy & Hold remained in negative return territory throughout most of the period, especially experiencing significant drawdowns from late February to early April. In contrast, the TradingAgents strategy significantly widened the performance gap after early March and continued expanding returns during BTC’s rebound phase in late April. This suggests that during sideways and declining markets, the strategy did not passively bear risks, but instead reduced part of the losses through Sell/Underweight and Flat states, while re-entering long positions during rebounds.

From the position distribution, the strategy was not permanently long, but frequently switched between Long, Flat, and Sell/Underweight. During the backtesting period, there were 43 Buy/Overweight days, 31 Sell/Underweight days, and 15 Hold/Flat days. This indicates that TradingAgents-BTC behaves more like an active timing strategy rather than a trend-following holding strategy. Its Daily Win Rate was 52.70%, which is not particularly high, but the Profit Factor reached 1.35, indicating that total profits from winning trades were sufficient to cover total losses from losing trades. The strategy’s advantage mainly comes from its profit-loss structure rather than an extremely high win rate.

In terms of risk control, the strategy’s maximum drawdown was -17.41%, lower than Buy & Hold’s -27.06%, indicating that the trading judgment and risk management mechanisms in the multi-agent framework provided a certain defensive effect during this period. The strategy’s Calmar Ratio was 6.492, showing relatively strong performance and indicating significantly better return efficiency per unit of drawdown compared with simple holding. The Annualised Sharpe Ratio was 1.738 and the Sortino Ratio was 2.070, indicating that the strategy possessed certain advantages in risk-adjusted returns, especially in controlling downside volatility.

6. Conclusion

Based on the TradingAgents multi-agent LLM financial trading framework, this paper explores its application to the BTC crypto market. By modifying the original stock trading workflow into a structure more suitable for the crypto market, the system introduces roles such as technical analysis, news analysis, sentiment analysis, and macro/on-chain analysis. Through bullish/bearish researcher debate, trader decision-making, and risk management review, the framework generates final trading signals. This design demonstrates the advantages of the Multi-Agent architecture in multi-source information integration, adversarial viewpoints, and risk control, while also providing an interpretable research framework for applying LLM trading systems to the crypto market.

Backtesting results show that TradingAgents-BTC achieved better return and risk performance than Buy & Hold during the testing period, indicating that the multi-agent LLM framework has certain application potential in BTC trading scenarios. However, these results should still be interpreted cautiously: the backtesting period only covered about three months, resulting in a relatively short sample period, and 1-hour trading may be affected by transaction fees, slippage, and signal delays. Future work should further validate strategy stability under longer periods and different market conditions, while also evaluating the specific contribution of on-chain data, macro variables, and risk management modules to overall strategy performance.

References:

Gate Research](https://www.gate.com/learn/category/research?)) is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.