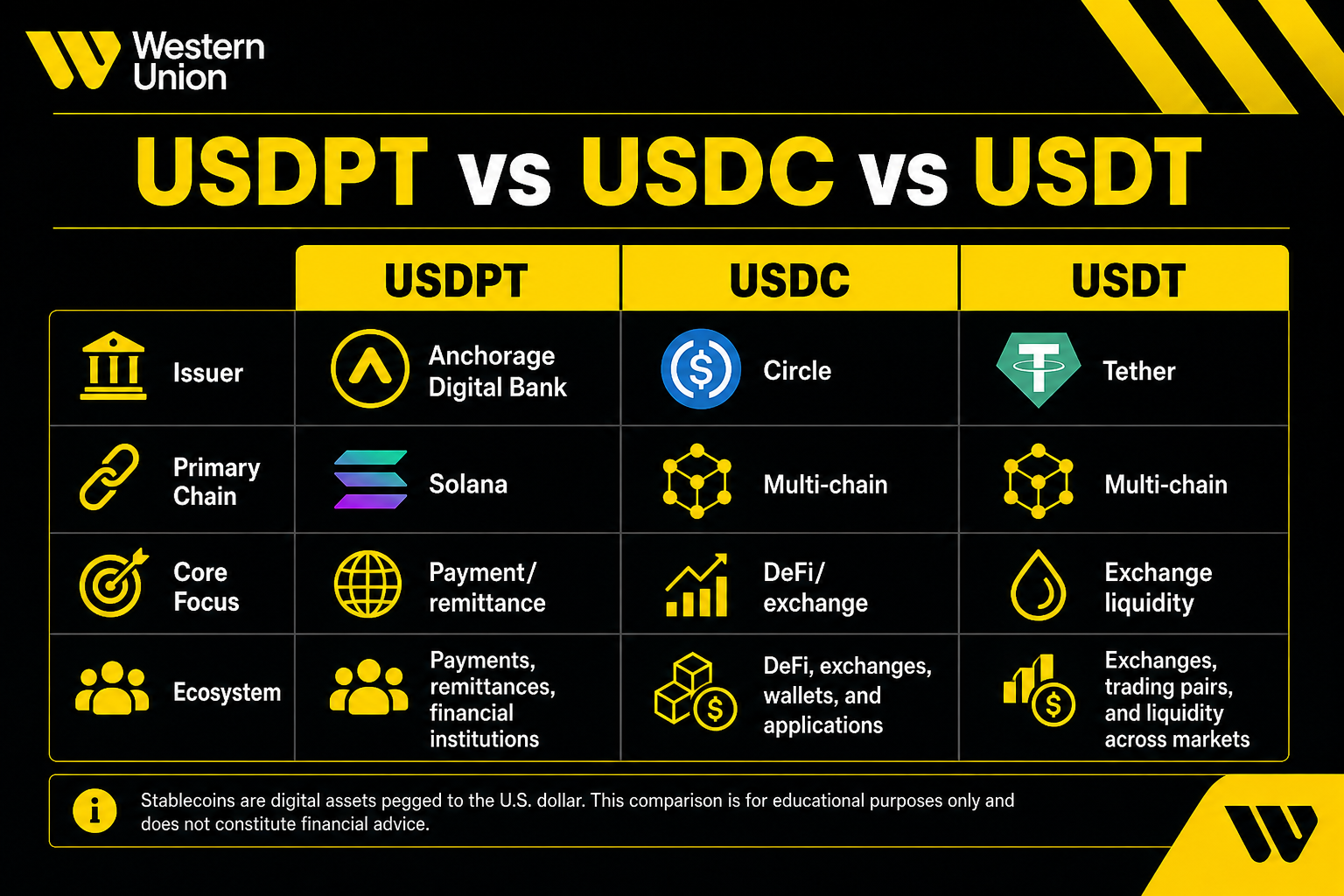

The core difference between USDPT, USDC, and USDT comes down to their issuers and ecosystem direction. USDPT is issued by federally chartered Anchorage Digital Bank on Solana and deeply integrated with Western Union’s global cash-out network. USDC is natively issued across multiple chains by Circle’s regulated entities, emphasizing institutional-grade compliance and cross-chain liquidity. USDT is issued by Tether and widely circulated across multiple chains, prioritizing exchange and OTC settlement liquidity. USDPT outlines the overall framework from three angles: issuance roles, Solana standards, and the Digital Asset Network.

All three maintain a nominal 1:1 peg to the U.S. dollar, but they differ in issuer, regulatory approach, blockchain coverage, and downstream cash-out channels. Treating them as interchangeable “1:1 USD stablecoins” risks overlooking critical differences in redemption paths, on-chain availability, and offline fiat conversion.

When comparing USDPT, USDC, and USDT, start by identifying “who issues it,” “which chain is it on,” and “can I cash it out to local fiat or USD.” Then evaluate each token’s fit for cross-border payments, DeFi liquidity, or exchange settlement.

What Is USDPT?

U.S. Dollar Payment Token (USDPT) is a USD-pegged payment stablecoin issued by Anchorage Digital Bank, N.A. on the Solana blockchain. It follows the SPL Token standard, with the Solana contract address HVWf8JmLoHs99Lw8Psf3fyqAtA4crWxCPkrmSdNjhNH3. Western Union integrates USDPT into its Digital Asset Network, connecting global agent locations, compliance checks, and fiat cash-out capabilities.

USDPT is built for payment and settlement, not as a general DeFi governance or yield token. Issuer Anchorage Digital Bank is an OCC-chartered federal national trust bank responsible for minting, redemption, and U.S. dollar reserve management. Anchorage Digital Bank issuing USDPT details the mint/burn authority and reserve release mechanism that form the on-chain credit foundation. Western Union serves as the ecosystem integrator, handling distribution, risk control, and offline cash-out — without being the direct on-chain token issuer. USDPT’s edge isn’t in the peg formula but in the combined structure: federal bank issuance + Solana single chain + Western Union global cash-out network.

What Is USDC?

USDC (USD Coin) is a USD-pegged stablecoin issued by Circle and its regulated entities, natively deployable on over 30 blockchains. USDC operates a full-reserve model, with reserves primarily consisting of cash and short-term U.S. government bonds and other cash equivalents, subject to regular third-party audits and disclosures.

USDC acts as an institutional-grade digital dollar across multi-chain ecosystems. Circle’s Cross-Chain Transfer Protocol (CCTP) enables native burn-and-mint cross-chain transfers between supported chains, reducing reliance on wrapped tokens and liquidity pools. Circle holds licenses in multiple jurisdictions, and USDC is subject to disclosure requirements under frameworks like MiCA. USDC is not FDIC-insured; its value is backed by the issuer’s reserve assets and redemption mechanism.

What Is USDT?

USDT (Tether) is a USD-pegged stablecoin issued by Tether Limited. It has long held the largest circulating supply among stablecoins. USDT is deployed on multiple blockchains including Ethereum, Tron, Solana, and BSC, and is a common settlement and quote asset on exchanges, OTC desks, and DeFi protocols.

Tether’s reserve disclosure model relies on periodic reserve reports and third-party attestations, with reserve assets spanning cash, cash equivalents, secured loans, precious metals, and other investments. Issuance and redemption are mainly handled through Tether’s platform and partner institutions. The alignment between on-chain USDT and off-chain reserves depends on the issuer’s disclosures and audit process. USDT’s core strengths are circulation depth and multi-chain availability. USDT on Tron is widely used for low-fee transfers. USDT is also not FDIC-insured, and assessing reserve transparency requires looking at disclosure frequency, asset composition, and redemption paths.

At a Glance: Where Are the Core Differences?

| Dimension |

USDPT |

USDC |

USDT |

| Issuer |

Anchorage Digital Bank, N.A. (OCC-chartered bank) |

Circle regulated entities |

Tether Limited |

| Regulatory Approach |

U.S. federal bank regulation |

Multi-country licenses + U.S. stablecoin rules alignment |

Offshore entity + reserve disclosures |

| Primary Blockchain |

Solana (single-chain launch) |

30+ chains native issuance |

Multi-chain (Ethereum, Tron, etc.) |

| Cross-Chain Capability |

Limited to Solana ecosystem |

CCTP native burn-and-mint |

Independent deployment per chain |

| Ecosystem Integration |

Western Union Digital Asset Network |

Circle institutional network, DeFi protocols |

Exchanges, OTC, DeFi |

| Offline Fiat Cash-Out |

Western Union agent locations planned |

Relies on partner institutions and bank channels |

Usually requires exchange or OTC conversion |

| Reserve Composition |

Bank demand deposits, Treasury bills, cash equivalents |

Cash, short-term U.S. government bonds |

Cash, equivalents, loans, other assets |

| FDIC Insurance |

Not protected |

Not protected |

Not protected |

The table above compares three stablecoins across eight dimensions. All three claim a 1:1 USD peg and lack FDIC protection. The differences lie in issuer type, chain coverage breadth, cross-chain mechanisms, and offline cash-out paths. USDPT reserves and 1:1 peg further explains USDPT’s reserve categories and on-chain supply verification. USDPT vs. Western Union traditional remittance compares the structural differences between Western Union’s traditional remittance and USDPT’s on-chain path.

Figure 1. Core differences between USDPT, USDC, and USDT: issuer, blockchain focus, ecosystem positioning, and primary use cases all differ.

Figure 1. Core differences between USDPT, USDC, and USDT: issuer, blockchain focus, ecosystem positioning, and primary use cases all differ.

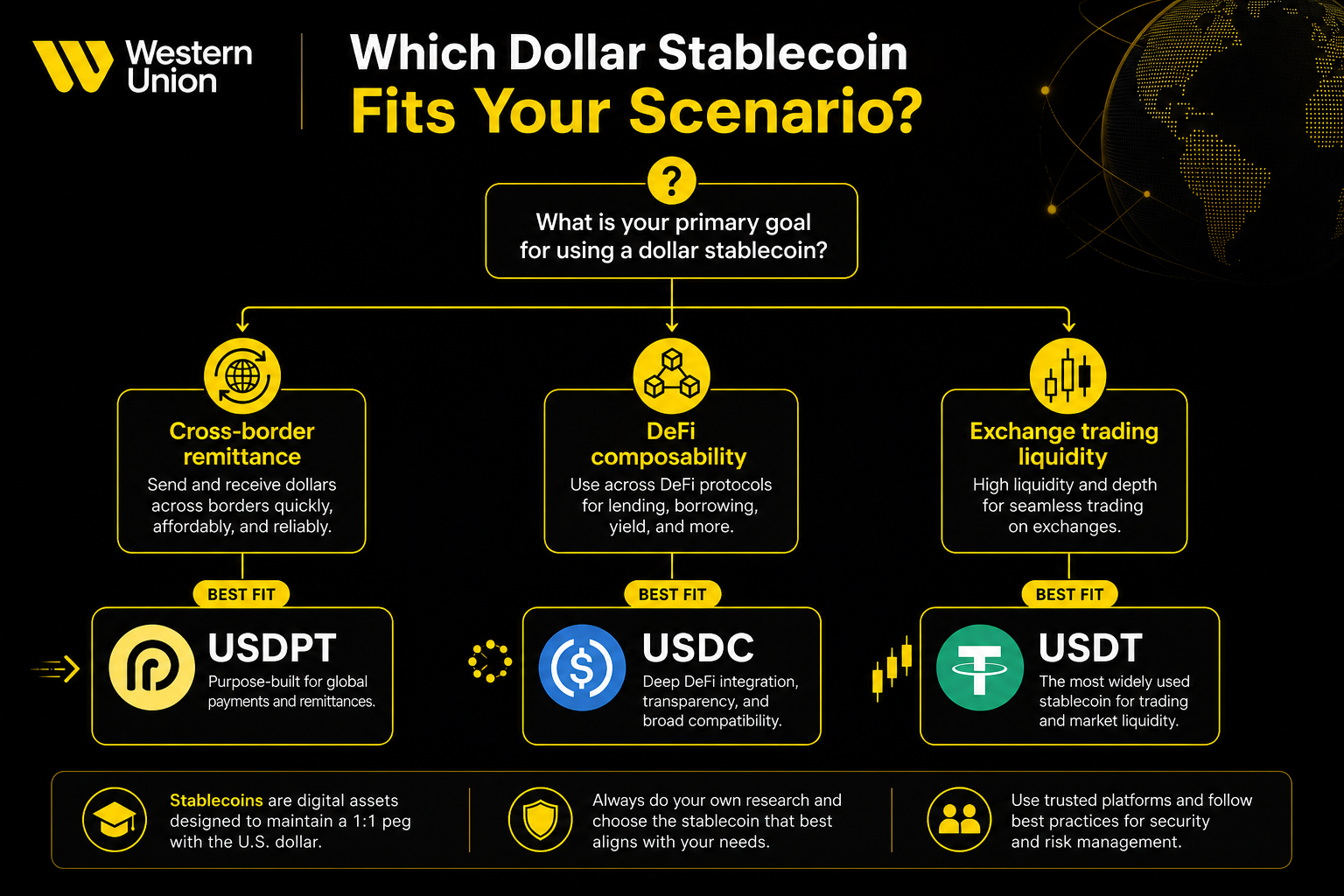

Cross-Border Remittance, DeFi, or Exchange: Which USD Stablecoin Should You Choose?

The right stablecoin depends on your use case. Choose based on “on-chain requirements + redemption/cash-out path + compliance needs,” not just circulating supply or brand recognition. USDPT mint-to-agent cash-out flow covers the four-step repeatable path from acquiring USDPT on an exchange to fiat delivery at a Western Union agent — ideal for evaluating cross-border payment and offline cash-out scenarios.

| Use Case |

Best Fit |

Why |

| Western Union cross-border remittance & agent cash-out |

USDPT |

Direct integration with Digital Asset Network and agent locations |

| Solana payment settlement |

USDPT or USDC |

Both on Solana; USDPT focused on payments, USDC on DeFi liquidity |

| Multi-chain DeFi interaction |

USDC or USDT |

Deeper liquidity and broader protocol support across multiple chains |

| Institutional treasury & compliance |

USDC |

Circle’s regulated entities and multi-jurisdiction licenses |

| Exchange trading & OTC settlement |

USDT or USDC |

Wide coverage in trading pairs on major exchanges |

| Tron low-fee transfers |

USDT |

Mature circulation and fee structure on Tron |

The table above lists six common scenarios with matching recommendations. Scenario matching isn’t a ranking — the same user may use different stablecoins at different stages. For example, you might hold USDC on Solana for DeFi while using USDPT for fiat cash-out at a Western Union agent.

Figure 2. USD stablecoin scenario selection: cross-border remittance, multi-chain DeFi, exchange liquidity, and Solana payments each map to different matching logic.

Figure 2. USD stablecoin scenario selection: cross-border remittance, multi-chain DeFi, exchange liquidity, and Solana payments each map to different matching logic.

What Are the Limitations of This Comparison?

Comparing these three stablecoins comes with structural limitations. Understanding these boundaries helps avoid oversimplification.

Similar peg, different ecosystem paths. All three claim a 1:1 USD peg, but reserve composition, audit frequency, and redemption liquidity vary. Relying on “they’re all stablecoins” doesn’t predict redemption performance under stress.

Chain coverage is not interchangeable. USDC is natively on 30+ chains, USDT is independently deployed, and USDPT launched on Solana only. In cross-chain scenarios, USDC can use CCTP for native transfer, USDT requires chain-specific contract operations, and USDPT’s cross-chain capability is limited by Solana.

Offline cash-out differs significantly. USDPT plans cash-out via Western Union’s Digital Asset Network agent locations. USDC and USDT typically rely on exchanges, OTC desks, or bank partners, with paths and fees varying by region.

Regulatory frameworks are evolving. Stablecoin legislation and enforcement are changing across countries, which may affect issuer compliance status and available markets.

Circulating supply ≠ scenario suitability. USDT has the largest supply, but that doesn’t make it optimal for every payment or cash-out scenario. USDPT has a smaller supply but offers unique agent cash-out potential within the Western Union ecosystem.

Summary

USDPT, USDC, and USDT are all USD-pegged stablecoins. The core differences lie in issuer, blockchain strategy, and ecosystem integration. USDPT is issued by Anchorage Digital Bank on Solana, deeply tied to Western Union’s global cash-out network, focusing on cross-border payments and offline fiat conversion. USDC is natively issued by Circle’s regulated entities across multiple chains, prioritizing institutional compliance and CCTP cross-chain liquidity. USDT is widely circulated by Tether across multiple chains, emphasizing exchange and OTC settlement depth. None are FDIC-insured. Choose based on your on-chain needs, redemption path, and target scenario.

FAQ

Are USDPT, USDC, and USDT all pegged 1:1 to the U.S. dollar?

All three are designed as 1:1 USD-pegged stablecoins, backed by reserve assets. A peg is not a government guarantee; none are FDIC-insured, and redemption speed and liquidity may be affected under extreme conditions.

How do USDPT and USDC differ on Solana?

Both are SPL tokens on Solana, but they differ in issuer, contract address, and ecosystem positioning. USDPT is issued by Anchorage Digital Bank and integrated with Western Union’s Digital Asset Network, focusing on cross-border payments and agent cash-out. USDC is natively issued by Circle and has deeper liquidity in Solana DeFi protocols.

USDT has the largest supply. Is it always the best choice?

USDT is widely used on exchanges and OTC, but supply alone doesn’t determine suitability. For cross-border agent cash-out, institutional compliance, or native cross-chain in DeFi, USDC or USDPT may offer better paths.

Which of the three is guaranteed by the U.S. government?

None. USDPT is issued by an OCC-chartered bank, USDC by Circle’s regulated entities, and USDT by Tether Limited. A federal bank charter does not mean the token itself is insured.

What factors should I prioritize when comparing stablecoins?

Check issuer, deployment chain, reserve composition and disclosure frequency, redemption and cash-out paths, and ecosystem integration for your specific use case. Always verify the contract address before transacting to avoid fakes.

Can USDPT replace USDC or USDT in DeFi?

USDPT is built for payments and Western Union integration. Solana DeFi protocols generally support USDC and USDT more broadly. USDPT’s DeFi availability depends on protocol integration; its core design is for payment and cash-out scenarios.