The fundamental difference between Western Union's traditional remittance and USDPT stablecoin remittance comes down to the asset vehicle and the number of intermediaries. The traditional model moves fiat currency through banks and correspondent banks, while the USDPT model first transfers the token on the Solana blockchain, then taps into Western Union's global cash-out network via the Digital Asset Network. USDPT (Western Union Stablecoin) provides a full picture of the USDPT framework across three dimensions: issuance structure, Solana on-chain standards, and Digital Asset Network use cases.

Cross-border remittances have long depended on bank correspondent relationships, SWIFT messaging, and local clearing rules in each country. U.S. Dollar Payment Token (USDPT) is issued on Solana by Anchorage Digital Bank, N.A., and Western Union has integrated it into its Digital Asset Network, enabling on-chain dollar value to connect with existing agent locations and compliance systems. Both paths can ultimately reach the 200+ countries and regions Western Union serves, but the intermediaries and settlement mechanics differ significantly.

Understanding these path differences helps in evaluating the applicable scenarios, compliance touchpoints, and potential limitations of "fiat channel remittance" versus "on-chain token plus offline cash-out," rather than simply declaring one path superior.

What Is Western Union Traditional Remittance?

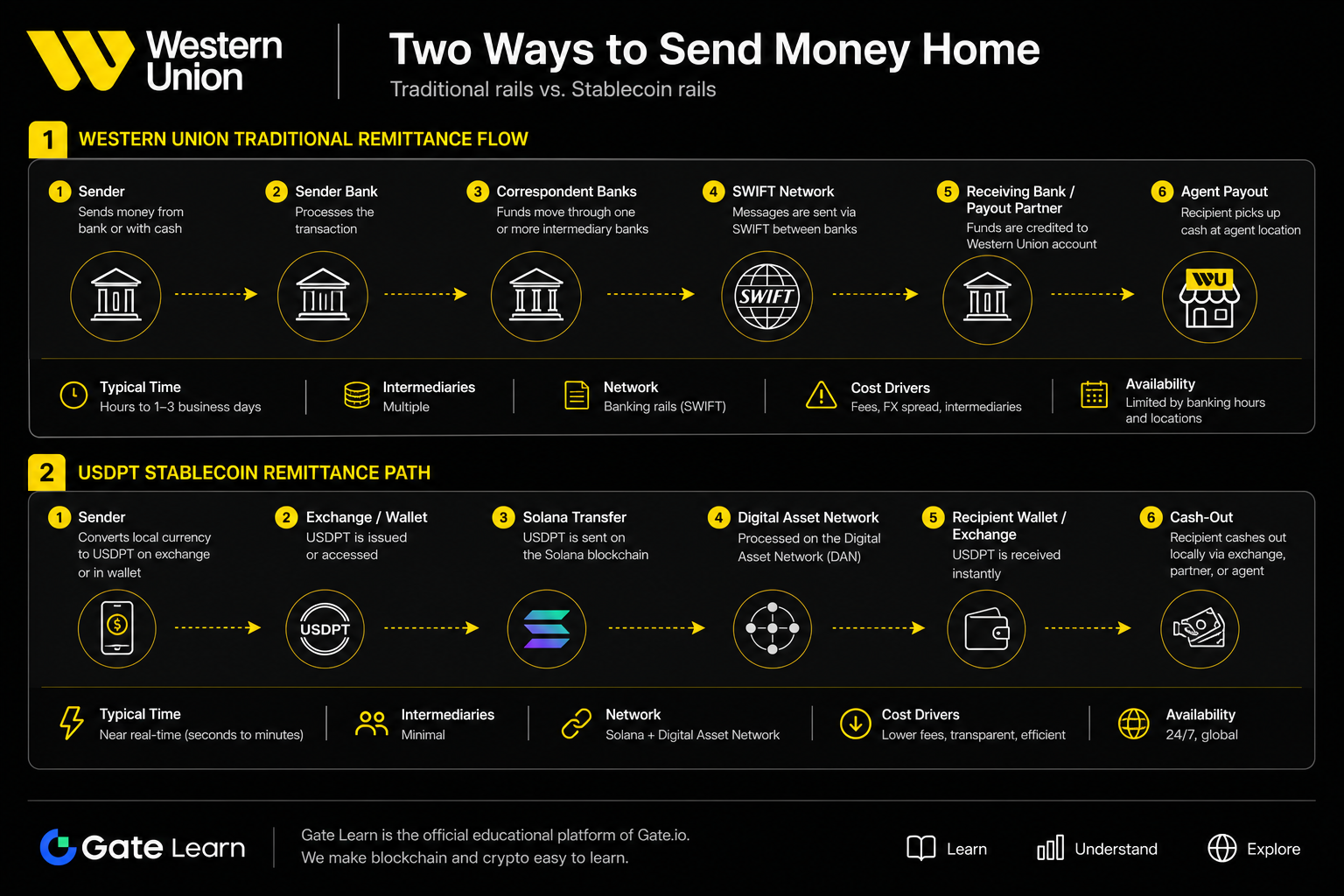

Western Union traditional remittance begins and ends with fiat currency. The sender typically submits instructions via the Western Union app, website, or an agent location. Western Union then processes the cross-border transfer through its own clearing system, correspondent banks, and local banking partners. When USD crosses borders, SWIFT messaging is commonly used for interbank communication. The sender operates entirely in fiat and never touches on-chain tokens. Each step is subject to bank business hours, holidays, and local regulatory rules, and the arrival time depends on the corridor and payout method.

What Is USDPT Stablecoin Remittance?

The USDPT remittance path adds a Solana token transfer layer between the on-chain phase and the fiat phase. USDPT is issued on the Solana blockchain by Anchorage Digital Bank, N.A., following the SPL Token standard and maintaining a 1:1 peg to the U.S. dollar. Anchorage Digital Bank's issuance of USDPT defines the mint/burn permissions, reserve validation, and redemption release that form the credit foundation of the on-chain phase. Senders or recipients must first acquire USDPT through exchanges, partner platforms, or minting channels, and on-chain transfers can be executed continuously on the Solana network.

Western Union's Digital Asset Network bridges on-chain USDPT with offline cash-out capabilities. The USDPT mint-to-cashout flow at agent locations outlines a repeatable path from exchange acquisition, on-chain holding, to fiat delivery at Western Union agent locations. In planned scenarios, recipients can receive cross-border remittances in USDPT in selected markets, achieving 24/7 on-chain settlement. Users of partner exchanges can also cash out USDPT for local fiat at Western Union agent locations.

| Phase |

Key Participants |

Function |

| Acquiring USDPT |

Exchanges, Anchorage minting channels |

Fiat conversion or 1:1 minting of USDPT |

| On-chain Transfer |

Solana network, SPL contracts |

24/7 token transfer with on-chain records |

| Network Interface |

Digital Asset Network |

Compliance screening, platform and agent routing |

| Fiat Delivery |

Western Union agent locations, local partners |

Cash withdrawal or local fiat credit |

The table above illustrates the four-stage structure of the USDPT remittance path. Compared with the pure fiat path, the on-chain phase offers continuous settlement and programmable transfers. The fiat cash-out phase, however, remains subject to market permissions, agent availability, and local regulations. Users must distinguish among the risks of on-chain private key security, Solana network status, and offline cash-out channels.

Figure 1. Comparison of the two remittance paths: The Western Union traditional path relies primarily on fiat and bank clearing, while the USDPT path adds Solana on-chain transfer and Digital Asset Network integration.

Figure 1. Comparison of the two remittance paths: The Western Union traditional path relies primarily on fiat and bank clearing, while the USDPT path adds Solana on-chain transfer and Digital Asset Network integration.

At a Glance: Key Differences Between USDPT Remittance and Western Union Traditional Remittance

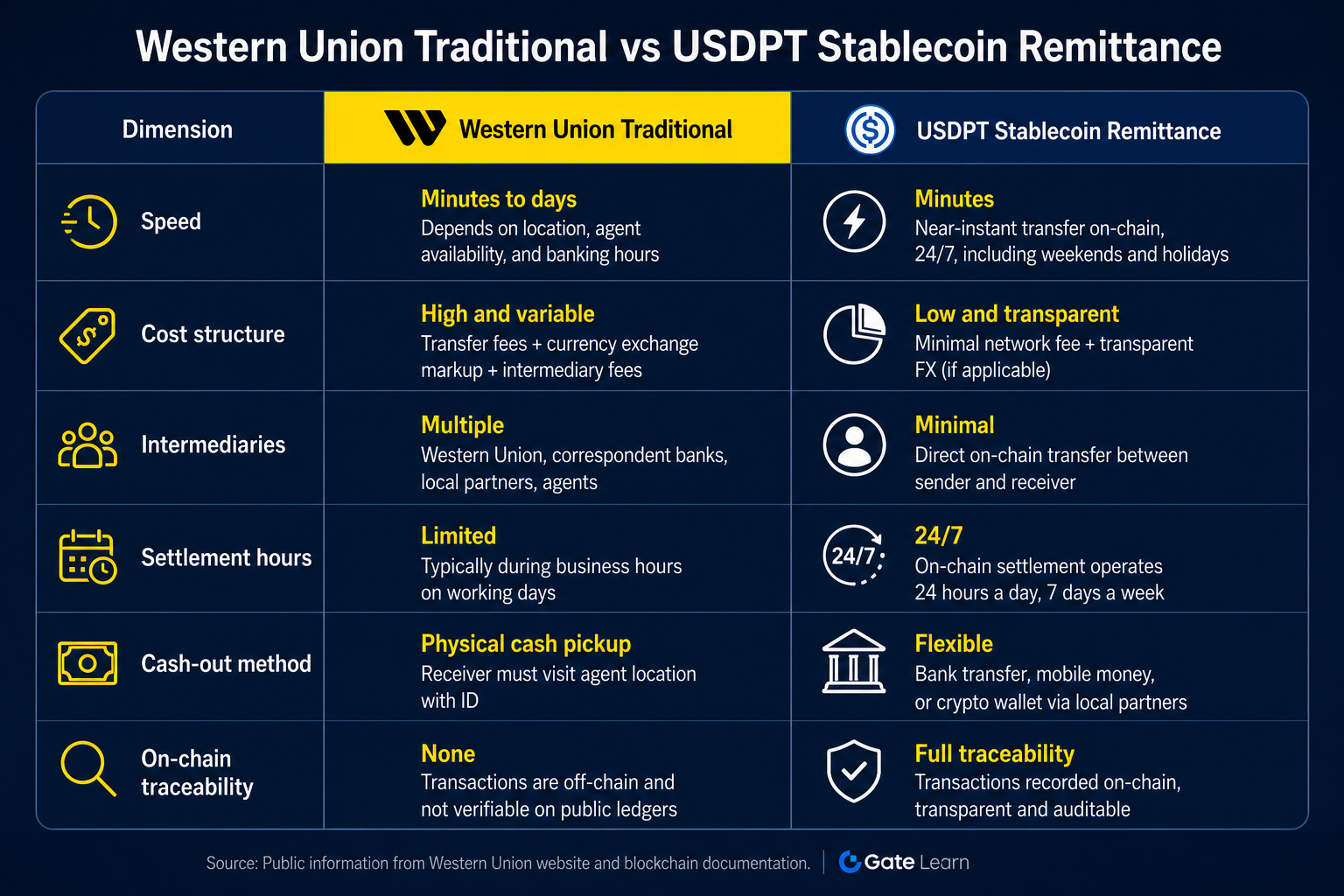

The two paths differ structurally in speed, fee composition, and the number of intermediaries. The comparison below is based on mechanism-level generalization; specific values vary by remittance corridor, amount, payout method, and market permissions and are not fee commitments.

| Comparison Dimension |

Western Union Traditional Remittance |

USDPT Stablecoin Remittance |

| Asset Form |

Fiat throughout |

On-chain USDPT + fiat cash-out |

| Settlement Time |

Affected by bank business hours and correspondent bank links |

On-chain phase: 24/7; fiat cash-out still subject to location and compliance procedures |

| Intermediaries |

Bank correspondents, SWIFT messaging, local clearing |

Solana on-chain transfer, Digital Asset Network, agent locations |

| Fee Structure |

Western Union fee + exchange rate margin + possible correspondent bank fees |

Exchange/minting fees + on-chain gas + Western Union cash-out fee |

| Traceability |

Bank and Western Union internal records |

Solana on-chain public records + Western Union compliance records |

| Technical Barrier |

Low; familiarity with fiat remittance is sufficient |

Requires knowledge of wallets, on-chain addresses, and token security |

| Coverage |

200+ countries and regions (traditional product) |

Planned coverage of 200+ countries/regions; specific USDPT features vary by market |

The table above compares the two paths across seven dimensions. The traditional remittance path involves more intermediary bank layers, and processing is tied to each country's bank calendar. The USDPT path can bypass some bank intermediaries in the on-chain stage, but users must bear the operational costs of acquiring tokens, managing private keys, and selecting compliant cash-out channels. USDPT vs USDC vs USDT distinguishes USDPT from other dollar stablecoins in terms of issuer, chain coverage, and offline cash-out paths, providing context for choosing an on-chain settlement tool.

Figure 2. Multi-dimensional comparison of speed, cost, and intermediaries: Each path has distinct characteristics in settlement continuity, traceability, and technical barriers.

Figure 2. Multi-dimensional comparison of speed, cost, and intermediaries: Each path has distinct characteristics in settlement continuity, traceability, and technical barriers.

For Cross-Border Remittances, Should You Choose USDPT or Western Union Traditional Path?

The choice depends on the user's technical capability, the recipient's preferences, arrival time requirements, and available market features—not on a one-dimensional ranking of which path is better.

Traditional remittance is more common when the recipient has no crypto wallet, needs only fiat arrival, or when the market has not yet enabled USDPT functionality. The USDPT path is more suitable when the sender or recipient already holds on-chain tokens, needs 24/7 on-chain arrival, or plans to cash out at a Western Union location via the Digital Asset Network. For crypto platform users conducting cross-border settlements that require verifiable on-chain records, the USDPT path is mechanically better aligned. For small, everyday family remittances, traditional products have a lower operational barrier. Scenario judgment must consider actual availability in the region: not all Western Union agent locations support USDPT cash-out.

What Common Compliance Requirements Do USDPT and Traditional Remittance Share?

Regardless of the chosen path, Western Union's core requirements for KYC, AML, and sanctions compliance remain consistent. As the issuer of USDPT, Anchorage Digital Bank, N.A., is subject to OCC federal banking supervision during minting and redemption. The Digital Asset Network applies Western Union's global risk control rules when on-chain tokens enter the cash-out system. USDPT is not protected by FDIC deposit insurance, and compliance does not mean zero risk.

What Are the Limitations of This Comparison?

An objective comparison requires awareness of four limitations: fees and arrival times vary by corridor, and uniform quotes are difficult to obtain through public channels; USDPT features are not rolled out simultaneously in all 200+ countries and regions, so comparing a mature traditional product with a planned feature may create mismatches; the USDPT path requires wallet and private key management skills, and operational errors can lead to irreversible on-chain losses; stablecoin and foreign exchange regulations are still evolving across countries, and policy changes may affect availability in specific markets.

Summary

Western Union traditional remittance centers on fiat currency, completing cross-border clearing through bank correspondents and SWIFT channels, then delivering funds to global agent locations. USDPT stablecoin remittance transfers dollar-pegged tokens on the Solana blockchain, accesses Western Union's cash-out network via the Digital Asset Network, and offers 24/7 continuous settlement and publicly traceable on-chain records. Both paths share a KYC/AML compliance framework, but differ in intermediaries, technical barriers, and fee structures. The choice of path should be based on a comprehensive assessment of the recipient's capabilities, available market features, and time sensitivity, not on a one-dimensional ranking.

FAQ

What is the biggest difference between USDPT remittance and Western Union traditional remittance?

The biggest difference lies in the asset vehicle and intermediaries. Traditional remittance uses fiat currency throughout, clearing through bank correspondents and SWIFT channels. USDPT remittance first transfers dollar-pegged tokens on the Solana blockchain, then connects to the Western Union global cash-out network via the Digital Asset Network.

Is USDPT remittance always faster than traditional remittance?

Not necessarily. The on-chain transfer of USDPT can be executed 24/7, but the fiat cash-out phase is still subject to Western Union's compliance processes, agent operating hours, and local rules. Traditional remittance in some mature corridors has already been highly optimized for arrival time. Actual speed varies by corridor and amount.

Do I need a crypto wallet to use USDPT remittance?

If the recipient receives the remittance in USDPT form, a Solana-compatible wallet and correct address are typically required. If the recipient only holds tokens on a partner exchange and cashes out through a Western Union location, the operation may resemble a centralized platform account, but it still involves on-chain token management steps.

Are the compliance requirements the same for both paths?

The core compliance framework is identical—both must complete KYC and AML checks. The USDPT path additionally involves banking supervision requirements for the issuance phase by Anchorage Digital Bank, as well as verification of on-chain addresses and token authenticity. Local regulations on stablecoins may vary by country.

Do all Western Union locations support USDPT cash-out?

No. USDPT cash-out capability is being rolled out gradually in selected markets through the Digital Asset Network and does not cover all agent locations in the 200+ countries and regions where Western Union operates. Specific availability should be verified based on actual features in the local market.

What fees should be considered when comparing the two paths?

For the traditional path, consider Western Union fees, exchange rate margins, and possible correspondent bank fees. For the USDPT path, include exchange or minting fees, Solana on-chain gas, Digital Asset Network cash-out fees, and possible platform buy-sell spreads. A total path cost should be calculated before making a comparison.