The on-chain value of the U.S. Dollar Payment Token (USDPT) depends on the U.S. dollar reserve assets held by Anchorage Digital Bank. For every new USDPT put into circulation, the issuer must allocate an equivalent amount in U.S. dollar assets to the reserve account, creating a fully backed structure. USDPT (Western Union Stablecoin) describes the overall framework from three angles: issuance responsibilities, Solana on-chain standards, and the Western Union ecosystem.

The credit foundation of a payment stablecoin lies not in on-chain algorithms, but in off-chain asset custody and redemption commitments. USDPT is designed for cross-border payments and the Western Union Digital Asset Network. The composition of its reserves and the 1:1 peg mechanism directly determine whether holders can reliably redeem for U.S. dollars and cross-check against on-chain circulating supply.

To understand USDPT reserves, you need to look at asset types, the mint and redeem process, and the distinction between "issued under federal bank regulation" and "government-guaranteed."

What Assets Make Up the USDPT Reserve?

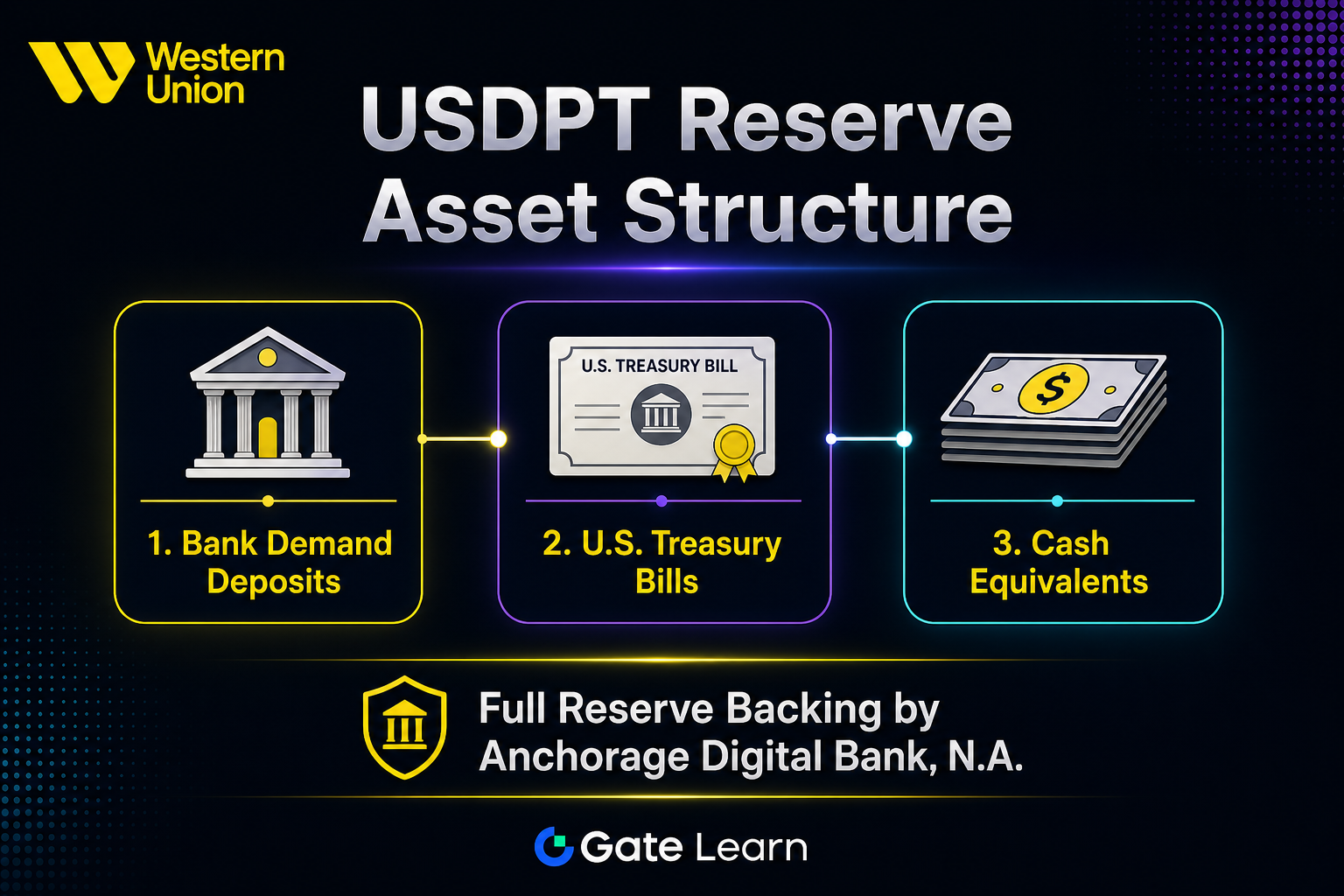

USDPT uses a fully backed reserve model. Anchorage Digital Bank holds an equal amount of U.S. dollar reserves for every USDPT in circulation. Publicly disclosed asset classes primarily include bank demand deposits, U.S. Treasury bills, and similar cash equivalents. All three are high-liquidity, dollar-denominated instruments with relatively manageable credit risk, making them a suitable base for a payment stablecoin.

Bank demand deposits facilitate redemptions and settlements. U.S. Treasury bills have short maturities, balancing safety with liquidity. Cash equivalents bridge the gap between deposits and Treasury bills to optimize liquidity structure.

| Asset Class |

Typical Characteristics |

Role in Reserves |

| Bank Demand Deposits |

High liquidity, available on demand |

Supports daily redemptions and settlements |

| U.S. Treasury Bills |

Short-term, backed by U.S. government credit |

Provides safety and predictable returns |

| Cash Equivalents |

Very short maturity, near-cash |

Adds liquidity and flexibility to asset structure |

The table above summarizes the three core asset types. Actual allocations may shift with redemption activity and interest rate conditions. The exact composition depends on periodic disclosures from Anchorage Digital Bank. Western Union handles distribution and redemption, but does not directly manage the reserves.

Figure 1. USDPT reserve asset structure: bank demand deposits, U.S. Treasury bills, and cash equivalents form the fully backed reserve base.

Figure 1. USDPT reserve asset structure: bank demand deposits, U.S. Treasury bills, and cash equivalents form the fully backed reserve base.

How Does the USDPT 1:1 Peg Work?

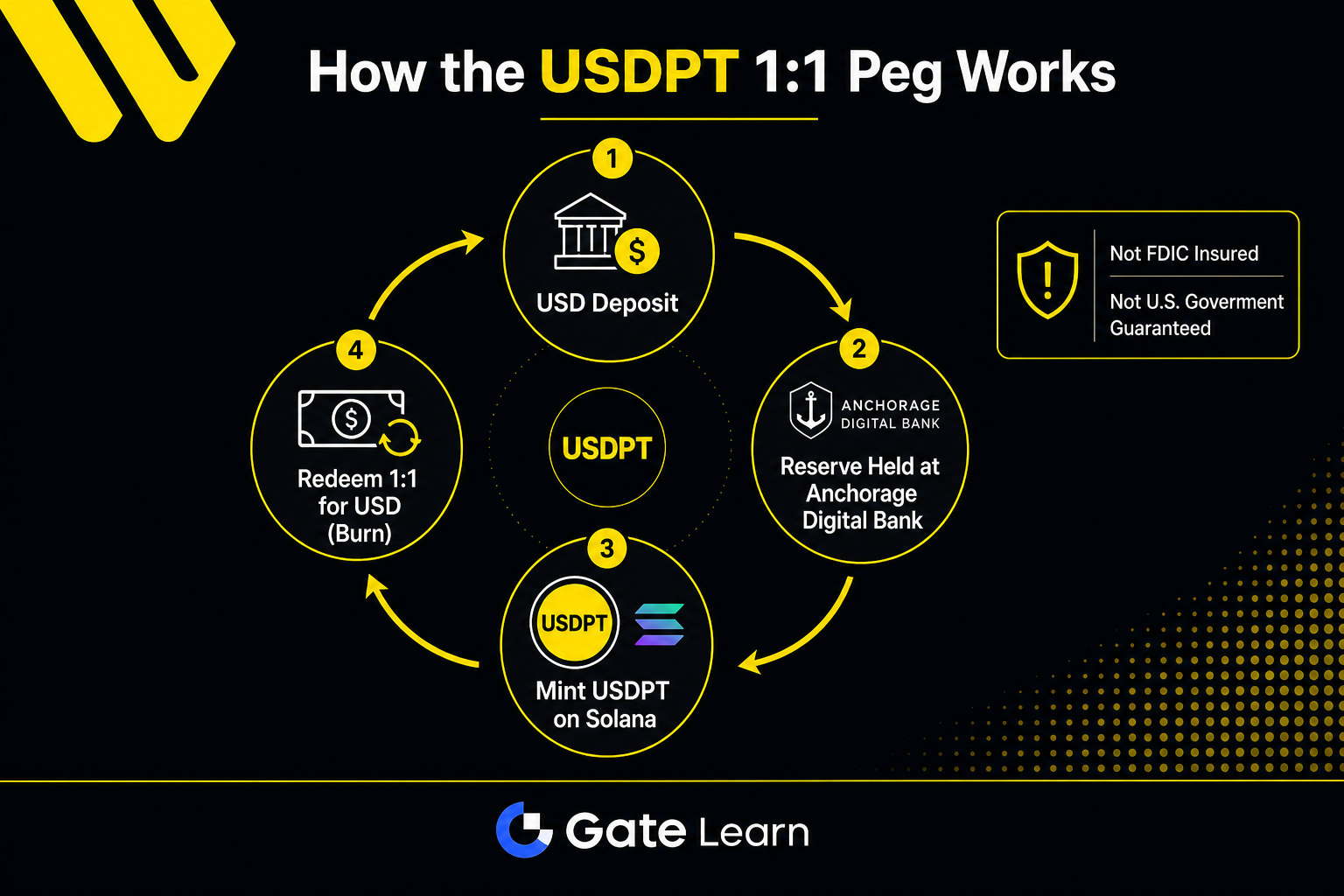

The USDPT 1:1 peg means that every on-chain USDPT token is backed by $1 in nominal reserve value. The peg is maintained through a two-way mint and redeem mechanism managed by the issuer. Anchorage Digital Bank issues USDPT handles USD deposit verification, on-chain minting, and redemption burn — the operational backbone of the peg.

The peg is issuer-managed, not algorithmically self-adjusting. Changes in on-chain USDPT supply move in lockstep with the USD assets in the reserve account. Once Western Union connects to the Digital Asset Network, on-chain transfers can happen 24/7, but the relationship between reserves and circulating supply remains under Anchorage Digital Bank's control.

| Step |

Trigger |

System Action |

Reserve Change |

| Mint |

USD deposit passes compliance checks |

On-chain USDPT issued |

Reserves increase by equivalent USD |

| On-chain Transfer |

User or institution initiates SPL transfer |

Token moves between addresses |

Total reserves unchanged |

| Redeem |

Holder submits redemption request |

On-chain USDPT burned |

Reserves decrease by equivalent USD |

The table shows the three core steps. On-chain transfers do not change total reserves — only minting and burning adjust them. The 1:1 refers to nominal value backing; short-term secondary market deviations may occur due to liquidity, but long-term stability depends on the redemption channel and reserve adequacy.

Figure 2. USDPT 1:1 peg flow: full path from USD deposit, reserve custody, minting on Solana, to 1:1 redemption burn.

Figure 2. USDPT 1:1 peg flow: full path from USD deposit, reserve custody, minting on Solana, to 1:1 redemption burn.

Is USDPT Covered by FDIC Insurance? How Is It Different from Bank Deposits?

USDPT reserve assets are managed by Anchorage Digital Bank, but USDPT itself is not a bank deposit product. The Federal Deposit Insurance Corporation (FDIC) covers eligible bank deposit accounts up to the standard limit set by current FDIC rules. As an on-chain SPL token, USDPT is not covered by FDIC insurance.

USDPT is also not a digital dollar issued or guaranteed by the U.S. government. The U.S. Treasury and Federal Reserve provide no direct guarantee for its redemption. The credit that supports the 1:1 peg comes from Anchorage Digital Bank's reserve management and redemption obligations as an OCC-chartered federal trust bank.

| Comparison |

FDIC-Insured Bank Deposits |

USDPT |

| Product Form |

USD deposits in a bank account |

SPL token on the Solana blockchain |

| Insurance Coverage |

Eligible deposits are FDIC-protected |

Not covered by FDIC insurance |

| Government Guarantee |

Not directly guaranteed, but covered by deposit insurance |

Not guaranteed by the U.S. government |

| Value Backing |

Bank liabilities and regulatory capital |

USD reserve assets held by the issuer |

| Redemption Method |

Bank counter or electronic transfer |

Through Anchorage Digital Bank's redemption process |

The table highlights the key differences. "Issued under federal bank regulation" and "government-guaranteed" are separate concepts: OCC oversight requires capital adequacy and compliance reviews, but that does not mean token holders get FDIC insurance or a government backstop.

How to Verify USDPT Reserves Against On-Chain Circulating Supply?

To assess USDPT reserve transparency, you can cross-check using on-chain data and off-chain disclosures. The total USDPT supply is publicly viewable on the Solana blockchain at the contract address HVWf8JmLoHs99Lw8Psf3fyqAtA4crWxCPkrmSdNjhNH3. Always verify the contract address and token symbol before any on-chain interaction to avoid counterfeit tokens.

Off-chain, check reserve reports and audit attestations published by Anchorage Digital Bank or Western Union. Ideally, disclosed total reserves should equal or exceed the on-chain circulating supply. USDPT Mint to Branch Cashout Flow explains how on-chain holdings and Digital Asset Network cashouts are systemically separated, which helps keep reserve verification distinct from understanding offline fiat delivery.

Risks and Limitations of USDPT Reserves

The USDPT reserve structure prioritizes safety and liquidity, but it still has built-in structural constraints and risk factors.

Structural Limitations: Reserves focus on safe, liquid assets, limiting yield potential. Disclosure frequency and detail level may still be evolving. The direct 1:1 redemption channel may primarily serve qualified institutions, so retail holders' ability to redeem depends on their access point. For cross-border scenarios, USDPT vs Western Union Traditional Remittance compares structural differences in settlement mechanisms between the on-chain token path and pure fiat paths.

Associated Risks: Mass simultaneous redemption requests could pressure liquidity. Interest rate changes affect reinvestment options. Solana network disruptions impact on-chain transfers but do not alter off-chain reserves. Evolving regulations across jurisdictions could limit availability. Counterfeit token risks require verifying the contract address every time. USDPT vs USDC vs USDT lays out structural differences in issuer, chain coverage, and cashout paths between USDPT, USDC, and USDT, helping you separate reserve mechanism risks from channel-specific risks.

Summary

USDPT reserves are fully backed by bank demand deposits, U.S. Treasury bills, and cash equivalents. The 1:1 peg is maintained through mint and redeem operations. USDPT is not FDIC-insured or U.S. government-guaranteed. Its value relies on the issuer's reserve management and federal banking oversight. To evaluate transparency, cross-check on-chain total supply against reserve reports.

FAQ

What assets make up the USDPT reserve?

The USDPT reserve primarily includes bank demand deposits, U.S. Treasury bills, and similar cash equivalents. Anchorage Digital Bank holds an equal amount of USD reserves for every USDPT in circulation. All three asset classes are dollar-denominated instruments with high liquidity and relatively low credit risk.

What does the USDPT 1:1 peg mean?

The 1:1 peg means each USDPT is backed by $1 in nominal reserve value. When minting, USD is deposited and an equivalent amount of tokens is issued on-chain. When redeeming, tokens are burned and USD is returned at a 1:1 rate. The peg is managed by the issuer, not algorithmically.

Is USDPT protected by FDIC deposit insurance?

No. USDPT is an on-chain SPL token, not a bank deposit product, and is not covered by FDIC insurance. Its value is backed by USD reserves held by Anchorage Digital Bank, not by deposit insurance.

Is USDPT a U.S. government-issued digital dollar?

No. USDPT is issued by Anchorage Digital Bank, with Western Union handling ecosystem distribution. It is not issued, endorsed, or guaranteed by the U.S. government. The U.S. Treasury and Federal Reserve do not provide any direct support for USDPT.

How can I verify if USDPT reserves match the circulating supply?

You can check the total USDPT supply on the Solana blockchain (contract address: HVWf8JmLoHs99Lw8Psf3fyqAtA4crWxCPkrmSdNjhNH3) and compare it with reserve reports from Anchorage Digital Bank or Western Union. Pay attention to total reserves, asset composition details, and how often the reports are updated.

What are the main limitations of the USDPT reserve structure?

Reserve assets prioritize safety and liquidity, which limits yield potential. Disclosure frequency and detail may still be developing. Direct 1:1 redemption channels may only be available to qualified institutions. Key risks to consider include extreme redemption waves, interest rate changes, regulatory shifts, and counterfeit tokens.