Why Is Adopting Stablecoins Harder for Enterprises Than Expected?

In recent years, stablecoins have evolved beyond cryptocurrency trading tools into critical infrastructure for global payments and financial services. Many assume that simply holding stablecoins like USDC or USDT enables instant cross-border payments or fund transfers. However, for enterprises and financial institutions, the reality is far more complex.

When a bank, payment company, or fintech platform seeks to integrate stablecoin services, it must address identity verification, anti-money laundering checks, fund monitoring, liquidity management, and regulatory requirements across different jurisdictions—in addition to the blockchain technology itself. These processes often involve multiple vendors and complex technical integrations, driving up deployment costs. Checker aims to consolidate these fragmented functions into a single service, making it easier for businesses to plug into the stablecoin financial system.

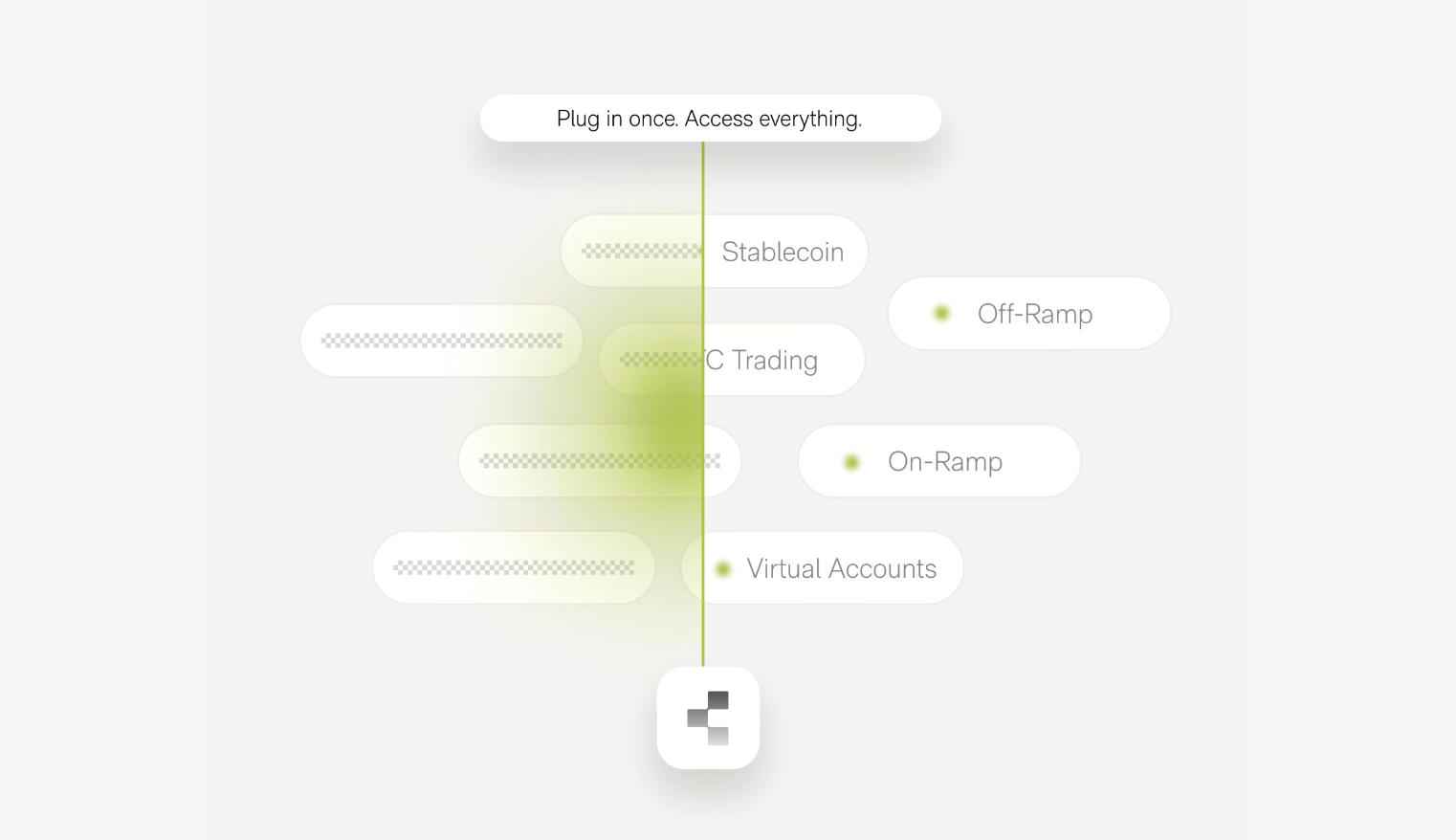

What Is Checker’s Core Architecture?

(Source: Checker)

(Source: Checker)

From a positioning standpoint, Checker functions as a technical intermediary layer between traditional finance and blockchain. Rather than directly interfacing with multiple blockchains, liquidity providers, payment networks, and compliance service providers, enterprises handle all operations through Checker’s unified platform. This model mirrors the Banking-as-a-Service (BaaS) concept in traditional finance but extends its scope to stablecoins and on-chain asset management. By integrating underlying technology, payment capabilities, and compliance tools, Checker helps enterprises reduce development complexity, shorten time-to-market, and improve efficiency when expanding into new markets and payment scenarios.

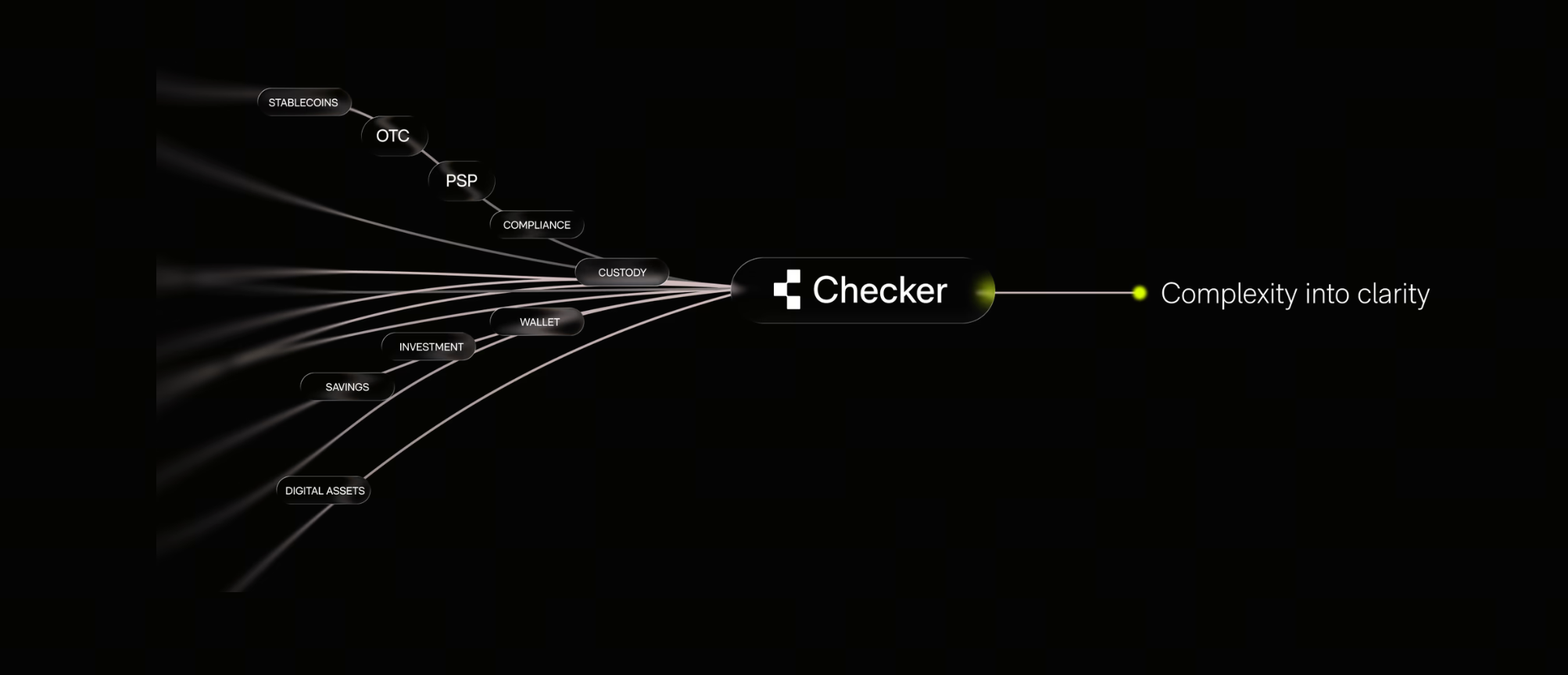

How Checker Helps Enterprises Integrate Stablecoin Services

(Source: Checker)

(Source: Checker)

Having understood Checker’s overall architecture, the next question is: How do enterprises actually integrate stablecoin services through this platform? For many, adopting stablecoins is not just about adding a payment method—it involves technical integration, identity verification, regulatory compliance, cross-border settlement, and fund management. Collaborating with separate vendors for each function often inflates development and maintenance costs.

Checker aims to consolidate these capabilities into a single platform, allowing enterprises to deploy stablecoin services through a unified process. Below, we break down the five main steps Checker uses to help businesses build a complete stablecoin financial infrastructure.

Step 1: Enterprises Access Stablecoin Services via API

The first step in Checker’s operational flow is API-based access. Traditionally, supporting multiple stablecoins and blockchains required separate integrations with each network. With Checker, enterprises connect a single API to manage various payment and asset services. This architecture frees development teams from diving into different blockchain fundamentals, letting them focus on product and business development. It also reduces integration costs when expanding into new markets or adding payment methods later.

Step 2: Complete KYC and Compliance Checks

For financial institutions, compliance is often the most critical aspect of stablecoin integration. Even with fast, low-cost blockchain transactions, failing to meet local regulatory requirements makes it difficult to operate formally. Therefore, Checker incorporates KYC (Know Your Customer), AML (Anti-Money Laundering), and source-of-funds checks into its platform.

When an enterprise opens an account or onboards a customer, the system handles necessary identity verification while monitoring for suspicious transaction activity. This design lets enterprises satisfy most financial regulatory demands without building a full compliance system from scratch.

Step 3: Build Payment and Settlement Capabilities

After completing technical integration and compliance procedures, enterprises can start using stablecoin payment services. Compared to traditional cross-border remittances, stablecoins offer a key advantage: 24/7 operation, unrestricted by banking hours. Through Checker’s payment architecture, enterprises can send, receive, and manage stablecoin fund flows, integrating data into their existing financial systems. This real-time settlement capability is highly attractive for cross-border e-commerce, international supply chains, and global fintech companies.

Step 4: Liquidity Management and Fund Allocation

Payments are just one part of the stablecoin infrastructure. As enterprises scale, fund management often becomes more critical than payment functionality itself. For example, a multinational may need to manage USD stablecoins, EUR stablecoins, and payment demands across different regions simultaneously. Insufficient liquidity can disrupt operations.

Checker integrates liquidity sources and fund allocation tools to help enterprises deploy capital more efficiently across markets. This focus is increasingly shared by other stablecoin infrastructure providers.

Step 5: Offer Financial Products and Value-Added Services

Beyond payments and settlements, the stablecoin market is spawning demand for additional financial services: yield products, foreign exchange, asset allocation, and corporate treasury management tools. Checker therefore extends beyond payment capabilities to build a more complete financial services ecosystem.

In the future, enterprises may use a single system to manage payments, investments, liquidity, and financing needs, further improving capital efficiency. This evolution is driving stablecoin infrastructure toward comprehensive financial platforms.

Why the Single API Model Is Winning Market Favor

From an industry perspective, the stablecoin market is entering an infrastructure competition phase. Early on, the focus was on which stablecoin attracted the most users. Now, as the market matures, enterprises care more about how to use stablecoins effectively. Platforms that simplify integration, lower technical barriers, and enable rapid service deployment are gaining traction. The single API model essentially abstracts complex blockchain financial processes, letting enterprises access the stablecoin market as easily as using cloud services.

How Might Stablecoin Infrastructure Evolve?

In the coming years, competition in the stablecoin market will likely shift from issuance scale to overall service capability. Enterprises need not just stablecoins, but a complete financial operating system—covering payments, clearing, liquidity management, compliance tools, and risk controls. As more financial institutions enter the space, the importance of infrastructure platforms will continue to grow. Checker’s direction represents the ongoing integration of traditional financial services with blockchain technology.

Summary

Checker’s core value lies not simply in offering stablecoin payment functions, but in establishing a standardized connection framework between enterprises and blockchain finance. Through APIs, compliance tools, liquidity management, and payment services, businesses can access the stablecoin market faster and more securely without building complex underlying systems themselves. As global financial markets increasingly accept stablecoins as payment and settlement instruments, infrastructure platforms like Checker may become a key driver of widespread stablecoin adoption.