Поки криптоіндустрія протягом останніх років досліджувала ліквідність активів у блокчейні, компанія Opendoor зараз намагається реалізувати подібний підхід у реальному секторі: використання штучного інтелекту для переосмислення ціноутворення, підбору та ефективності фінансування житла — одного з найменш ліквідних класів активів. Звіт про фінансові результати за перший квартал 2026 року, рідкісна інсайдерська купівля акцій генеральним директором і повністю AI-орієнтований транзакційний процес разом знаменують запуск "Opendoor 2.0". Це вже не просто історія про відновлення компанії з галузі proptech. Це глибокий експеримент із цифровізації ціноутворення реальних активів і перебудови ліквідності.

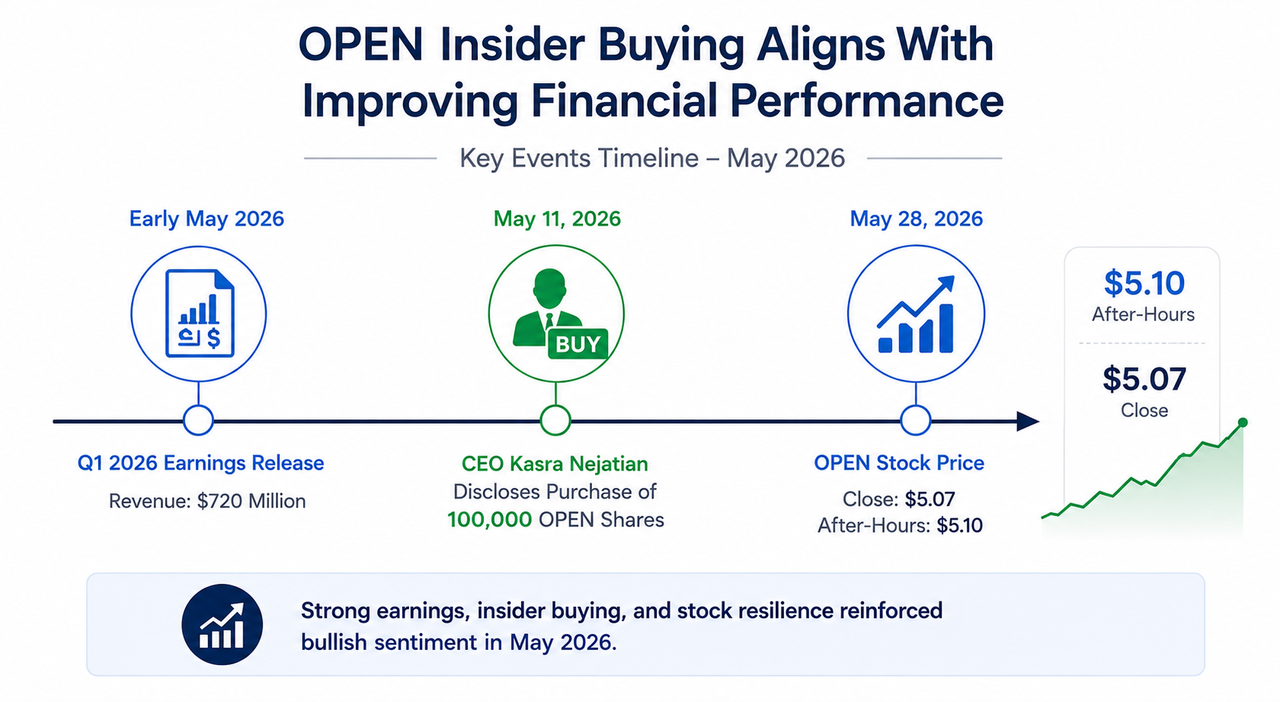

Динаміка ціни акцій OPEN і хронологія інсайдерської купівлі CEO

Ринок переоцінює не лише виручку — він переоцінює ефективність обороту активів, керовану AI

На початку травня Opendoor оприлюднила фінансові результати за перший квартал 2026 року: $720 мільйонів виручки, $72 мільйони валового прибутку, валова маржа відновилася до 10%. Чистий збиток скоротився до $173 мільйонів, обсяг грошових резервів становив близько $999 мільйонів, а коефіцієнт поточної ліквідності — 7,1. Це вказує на надзвичайно стійкий баланс. Незабаром після цього генеральний директор Касра Неджатьян придбав 100 000 акцій OPEN на відкритому ринку за власні кошти, чітко продемонструвавши впевненість керівництва. Станом на 28 травня ціна закриття OPEN складала $5,07, а після завершення торгів піднялася до $5,10.

Джерело: Blaze Dimov (Medium)

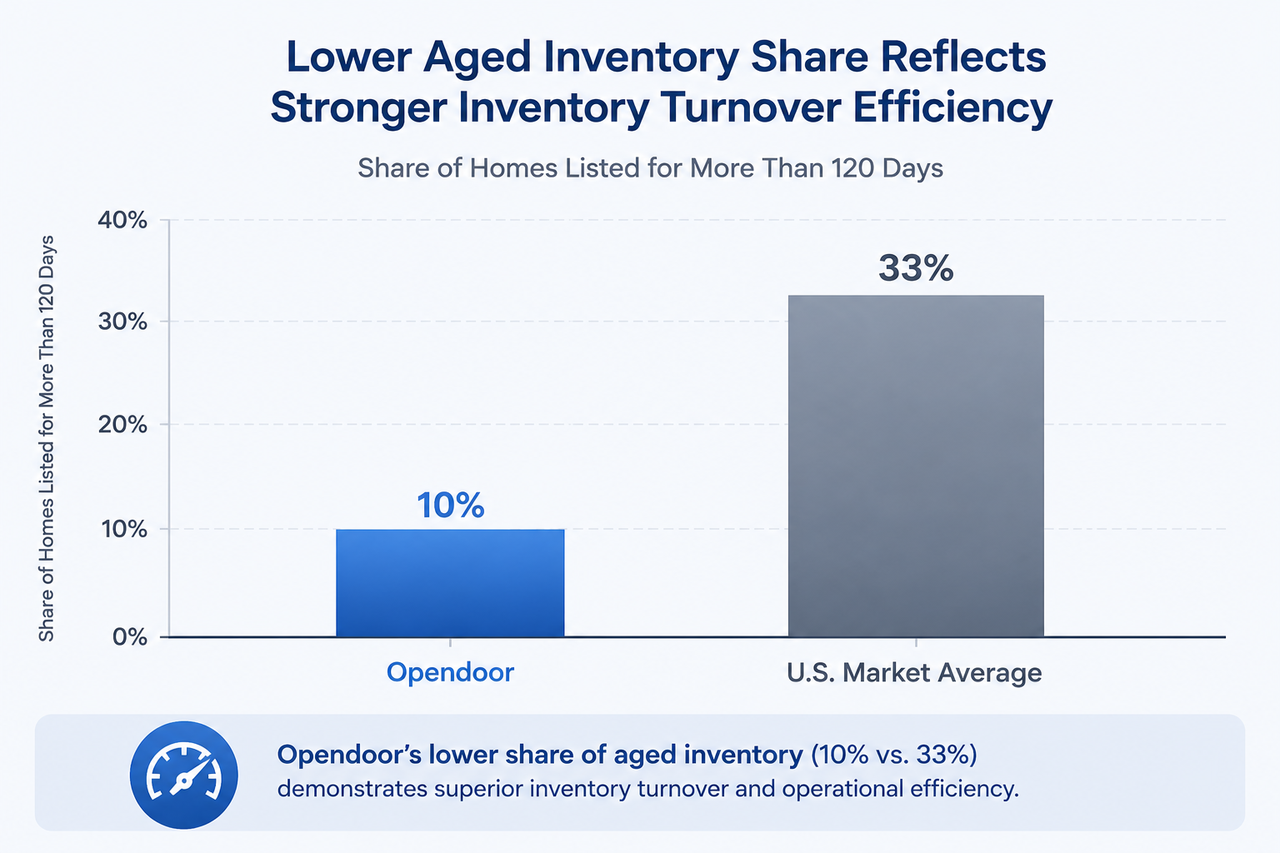

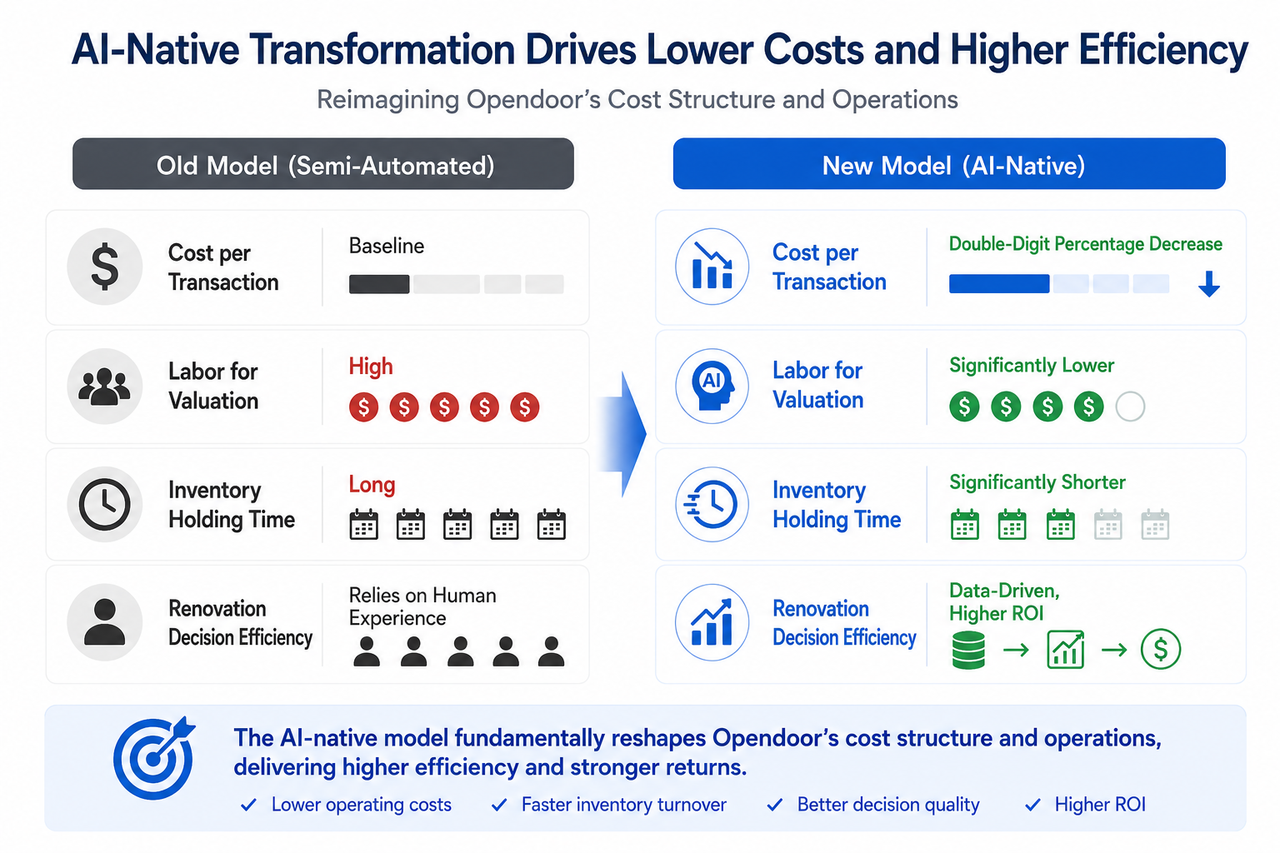

Однак справжнім каталізатором переоцінки з боку ринку стала не лише перевищена виручка. Ключова зміна — у якості запасів: лише 10% об’єктів нерухомості Opendoor перебували у продажу понад 120 днів, тоді як по ринку США цей показник становить 33%. Це означає суттєво коротші періоди утримання, значно менший ризик зниження цін і структурно підвищену ефективність капіталу. З фінансової точки зору це нагадує індикатор ризику для системи високочастотного маркетмейкінгу, а не звичайний звіт забудовника про запаси.

Порівняння якості запасів Opendoor із середнім показником по ринку

Від епохи нульових ставок до ліквідності, керованої AI: чому модель iBuying переглядають

Якщо поглянути на 2022–2024 роки, Opendoor майже стала символом краху бульбашки епохи низьких ставок. Модель iBuying базувалася на швидкому обороті та зростанні вартості активів. Коли Федеральна резервна система різко підвищила ставки, вартість запасів впала, збитки зросли, а акції подешевшали більш ніж на 90%. Тоді панівною стала думка, що це "помилка, породжена нульовими ставками".

Справжній перелом настав у 2025 році. Opendoor вийшла з непрофільних ринків, суттєво скоротила операційні витрати та непомітно створила повністю AI-орієнтований транзакційний процес. На початку 2026 року ця система повністю замінила попередні напівавтоматизовані процедури, охопивши динамічне ціноутворення, автоматичну перевірку титулів і інтелектуальне формування пропозицій. Одночасно власні іпотечні продукти Opendoor досягли прориву в ціноутворенні — їхня вартість приблизно на 100 базисних пунктів нижча за ринкову.

Цей шлях нагадує трансформацію крипторинку після 2022 року: ринки перейшли від зростання, зумовленого ліквідністю, до прибутковості, заснованої на ефективності. Чи йдеться про блокчейн-протоколи, біржі або proptech-платформи, зараз капітал цінує реальний грошовий потік, контроль ризиків і автоматизацію, а не лише масштаб.

AI не просто перебудовує маркетинг — він переосмислює ціноутворення ризику активів

Ключ до розуміння Opendoor 2.0 полягає в тому, що штучний інтелект використовується не для "косметичного оновлення" старих процесів — він повністю перебудовує весь ланцюг транзакцій з нуля. Оцінка, рішення щодо ремонту, стратегії розміщення та періоди утримання — усе це керується алгоритмічними системами, що навчаються у реальному часі. Керівництво компанії повідомило під час earnings call, що операційні витрати на одну транзакцію знижуються двозначними темпами, і саме це є основним чинником досягнення позитивного скоригованого EBITDA.

З точки зору фінтеху, ця система фактично є високочастотним рушієм ціноутворення ризику для ринку нерухомості. Ключова перевага — вже не в обсязі запасів, а у швидкості ціноутворення, коротшому періоді експозиції та зниженні транзакційного тертя. Це мова, яку добре розуміють користувачі крипторинку: маркетмейкінг, рушії ризику, алгоритмічні фінанси.

Потенційна зміна логіки оцінки

У міру того як ефективність ціноутворення на основі AI та переваги фінансових продуктів стають більш очевидними, ринок поступово перекваліфіковує OPEN із "компанії з нерухомості" на "AI-фінтех-платформу". Якірні точки оцінки для кожного з цих підходів принципово різняться:

| Тип оцінки | Основна логіка | Ключові метрики |

|---|---|---|

| Традиційна нерухомість | Чиста вартість активів, балансова вартість | PB, ризик уцінки запасів |

| AI-платформа | Мережеві ефекти технологій, data flywheel | Обсяг транзакцій, швидкість ітерацій алгоритму |

| Фінтех | Довічна цінність клієнта, чистий процентний дохід | Обсяг іпотечного портфеля, коефіцієнт конверсії |

Останнє відновлення ціни акцій OPEN значною мірою відображає обережну переоцінку ринком цієї зміни логіки. Якщо скоригований EBITDA стане позитивним за підсумками року, цей процес може прискоритися.

Дискусія "бики-проти-ведмедів": AI-оповідь проти структурних обмежень

Джерело: Benzinga (Linkedin)

Нинішнє протистояння "биків" і "ведмедів" щодо OPEN є класичним. Оптимісти наголошують на інсайдерській купівлі CEO, прямому впливі іпотечних ставок на 100 базисних пунктів нижчих за ринок на залучення клієнтів і щомісячні платежі, а також на можливості переоцінки компанії у міру наближення до прибутковості. Песимісти зосереджуються на структурно слабких продажах житла в умовах високих ставок, невипробуваних ризиках іпотечних портфелів із низькими ставками протягом повного кредитного циклу та на суттєвій різниці між чистим прибутком за GAAP і скоригованими показниками.

Існує також глибший ризик, пов’язаний із самим AI-наративом. Ринок може переоцінювати короткострокові вигоди від "AI, що все перевинаходить". Якщо маржа прибутку не зросте у наступних кварталах, AI-лейбл може, навпаки, стати причиною стискання оцінки.

Висновки для RWA, AI-агентів і ринків активів у блокчейні

Джерело: Antier

Вийшовши за межі аналізу однієї акції, Opendoor 2.0 має ширші наслідки для криптоіндустрії та фінтех-інфраструктури.

По-перше, нерухомість — один із найменш ліквідних основних класів активів. Використання Opendoor штучного інтелекту для ціноутворення та автоматизованого підбору фактично трансформує ліквідність реальних активів. Це співзвучно основній логіці сектору RWA, який прагне вирішити проблему ліквідності після токенізації активів.

По-друге, якщо AI-агенти почнуть брати участь у транзакціях із реальними активами, такі системи, як Opendoor 2.0 — із повністю алгоритмічним ціноутворенням і виконанням — можуть стати першими інтерфейсами транзакцій, орієнтованими на агентів, у реальному секторі.

По-третє, у міру того як дані про транзакції з житлом, моделі ціноутворення та автоматизація досягатимуть достатньої стандартизації, відкриється потенціал для перенесення цих процесів у блокчейн, токенізації нерухомості та створення систем забезпечення на основі блокчейну. Хоча це поки що досить спекулятивно, напрямок уже окреслений.

Opendoor 2.0: порівняння структури витрат до та після впровадження AI-процесів

Висновок

Інсайдерська купівля CEO, система на основі штучного інтелекту, яка з нуля перебудувала транзакційний ланцюг, і іпотечні ставки на 100 базисних пунктів нижчі за ринок — ці чинники роблять історію Opendoor у 2026 році унікальною. Але справжня міжгалузева значущість полягає не лише у відновленні однієї компанії. Це спроба перевести малоліквідні активи на алгоритмічне ціноутворення та ефективний обіг. Якщо минуле десятиліття інтернет радикально змінив обіг інформації, то наступне десятиліття фінансових систем на базі AI може трансформувати ліквідність реальних активів. Opendoor 2.0 — один із найцікавіших ранніх експериментів у цьому напрямку. Кожен факт і структурна зміна заслуговують на аналіз у цьому ширшому контексті.